Sovereign debt levels soared during the pandemic, and countries at the eurozone’s periphery may look high risk. But appearances can be deceptive.

Although the 2008 euro-area sovereign debt crisis seems well behind us, investors remain wary of a recurrence and nervous of high debt levels.

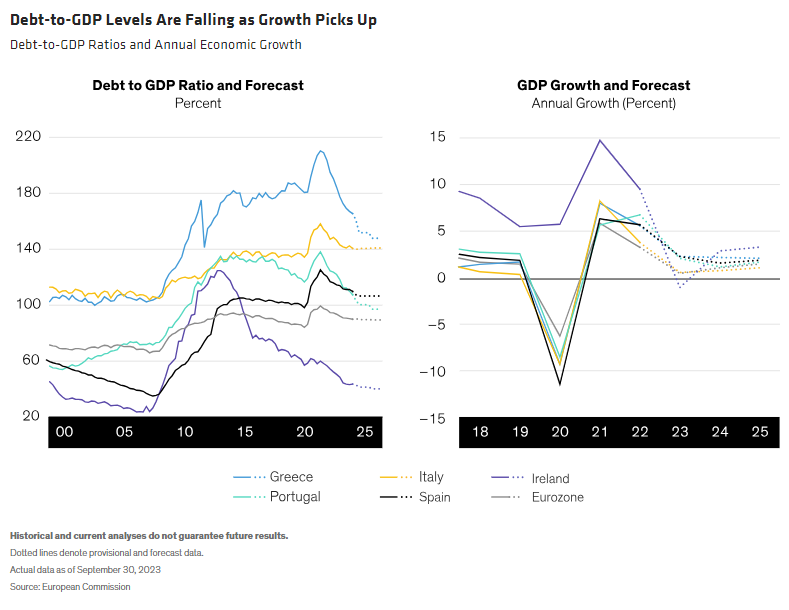

During the pandemic, shrinking economies and more interventionist fiscal policies increased debt-to-GDP ratios across Europe, leaving peripheral euro-area countries more vulnerable to economic shocks. While debt ratios have now stabilized, the European Commission forecasts they won’t fall much in the next two years and will mostly remain well above the limit required by the European Union’s (EU’s) Stability and Growth Pact (SGP). That sounds like a scary scenario—but it doesn’t tell the whole story.

Economies Are Healing After the Pandemic

Overall, the EU’s peripheral nations—Greece, Ireland, Italy, Portugal and Spain—have already reduced their debt-to-GDP ratios significantly since the pandemic and continue to make gradual progress (Display). Italy is the exception: its debt-to-GDP ratio is forecast to remain high (140%) until at least 2025, and its growth prospects are the lowest of the peripheral countries.

Despite their high debt ratios, peripheral European countries’ growth trends look relatively favorable. Lately, these nations have outperformed their northern European neighbors, such as Germany and the Netherlands, because their economies tilt more towards services and depend less on energy and global trade.

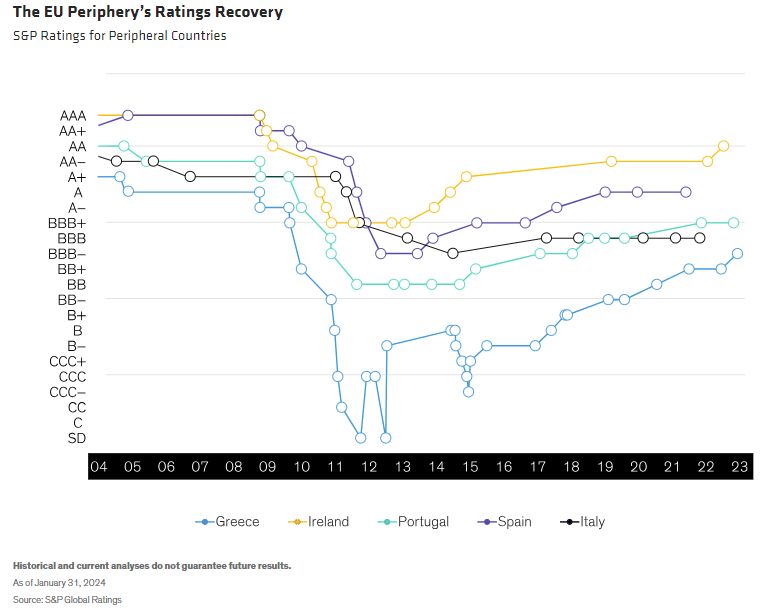

Ratings upgrades acknowledge the more positive trends (Display). Greece was recently rerated to investment grade by leading agencies, following on from Portugal, which is approaching A status. Ireland is approaching AA status, while Spain remains a strong A. Italy at BBB has yet to make post-pandemic ratings progress.

New Structures Address Systemic Risks

Since the 2008 crisis, European and global institutions have created and improved an array of structures to better manage systemic risk. In the eurozone, sovereign-bond-buying programs—including the European Central Bank’s (ECB’s) asset purchase programme (APP, 2014) and pandemic emergency purchase programme (PEPP, 2020)—have helped reduce sovereign spreads during periods of heightened investor concern. Subsequently, the introduction of the Transmission Protection Instrument (TPI, 2022) has reduced market stress and lowered spreads. Once activated, the TPI would enable the ECB to make targeted purchases to support the bonds of individual member states.

In response to the pandemic emergency, the European Commission assumed borrowing powers to provide both loans and grants to specific euro-area countries through the Recovery and Resilience Facility (2021). This represented the first move towards a common debt structure across the EU to help address the needs of individual member states and reduce their funding costs.

Currently, the European Commission is revising its approach to sovereign-debt control. While the original SGP rules prescribed a rigid ceiling on deficits and debt ratios (which were not to exceed 3% and 60% of GDP respectively), the recently agreed revisions to the SGP will allow a more flexible country-specific approach to managing debt levels down. We expect this new approach will both encourage fiscal discipline and help contain market stress should a country fail to meet its targets in any given year—without severely impacting that country’s economic growth.

Stronger Banks Mean Lower Stress

A sounder banking system has also helped reinforce financial stability. While last year’s US regional banking crisis and the failure of Credit Suisse reminded us of the ever-present risks to the banking sector, banks’ balance sheets are much stronger than before the global financial crisis. Higher liquidity ratios and a stronger overall regulatory framework have helped prevent regional crises escalating to global level.

In Europe, the banking supervision reforms initiated in 2014 have helped to improve monitoring and increase the soundness of the banking sector. Although systemic stress increased in 2022, this episode was relatively short-lived, partly because of reduced risks of contagion from the financial sector to the real economy.

Bond Pricing Reflects the New Reality

With the benefit of these additional safeguards, the initial stages of ECB policy tightening have proceeded as planned: the APP quantitative tightening (QT) that began in March 2023 is going smoothly, while the announcement of the roll-off and discontinuation of the PEPP hasn’t disturbed sovereign spreads.

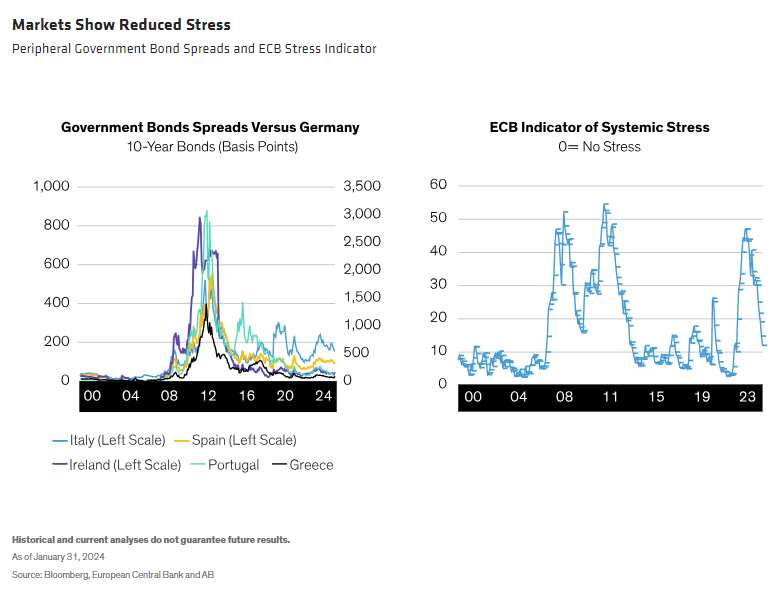

Peripheral government bond spreads remain at or near their lowest since the 2008 crisis, reflecting both stable domestic economic conditions and lower sensitivity to changing market sentiment (Display). Here again, Italy stands out. While BTP-Bund spreads are lower than during the sovereign-debt crisis, they remain volatile in response to Italy’s structural challenges. Even so, we expect those spreads will continue to fluctuate around current levels as QT proceeds undisturbed.

“The Periphery” Is Becoming History

We see a more constructive period ahead for EU sovereign debt. More supportive structural and regulatory conditions should help discourage excessive borrowing and prevent systemic shocks. We also expect the ECB to start cutting rates this summer, which would feed through to lower funding costs over time for euro-area sovereign borrowers.

In light of these changes, we believe investors should focus not on systemic worries but on the merits of individual euro-area issuers. While the EU’s peripheral economies may have been more uniform in 2008, today we can see wide divergences that make it less appropriate to view them as a bloc; in fact, the stronger members are increasingly being classified as “semi-core.”

Italy remains the standout—in our view, for idiosyncratic rather than systemic reasons. We see Italian politics as the main driver of the country’s economic fortunes and believe investors should pay close attention to the Italian political scene. Today, a setback for Italy might cause a ripple in euro sovereign spreads. But we think it would be unlikely to cause a tempest.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© AllianceBernstein

Read more commentaries by AllianceBernstein