In 1958, few took notice when the low-budget movie The Blob hit the screens. Starring Steve McQueen in his first leading role, this film about an unstoppable blob became a cult classic. Fifteen years later, the finance industry began creating another blob of sorts. In 1973, the first bond indexes were introduced to track the performance of investment grade fixed income. Like the movie villain, these indexes grew considerably and have proved unstoppable. Bond indexes provide valuable information to market participants, but they were not designed to be ideal investments. In fact, modern portfolios based on such indexes may be victims of what is sometimes called the “Blob Effect.”

How the Blob Effect Engulfed the Bond World

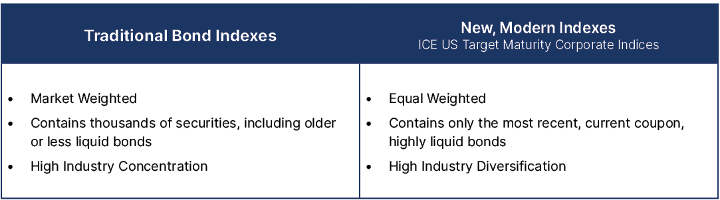

Bond data is inherently more difficult than stocks; they do not trade on centralized exchanges, bond math is more complex than simple price data, and bonds outnumber stocks by a margin of 4.5x. So despite the long history of bonds, bond indexes were not developed until well after their stock counterparts, and were patterned after their market capitalization weighted cousins. Bond indexes weight companies by their relative amount of debt outstanding: the greater the debt, the greater the index share. Rewarding the most valuable companies is useful in equity indexes, but rewarding the biggest debt issuers in bond indexes should cause concern among investors seeking exposure to less indebted companies.

By incorporating all eligible bonds from each issuer, traditional fixed income indexes contain thousands of securities, including older or less liquid securities. In our opinion, these indexes are so large that investing in them directly is at best inefficient and at worst simply unachievable. Many of the bonds in the marketplace today were issued by corporations for myriad reasons some time ago — for example, to “lock in” lower coupons or to finance an immediate business need. The result is an index influenced by somewhat random factors useful to issuers and traders, but not necessarily to investors.

As ETFs have sprung up around bond indexes, companies representing a larger portion of these indexes find more demand for their “index eligible” debt — so they issue more and more. Over time, a potential horror show for investors has emerged: the serial issuer. These companies issue debt frequently, and often in large quantities, encouraged and rewarded by the index as it guarantees demand for their bonds.

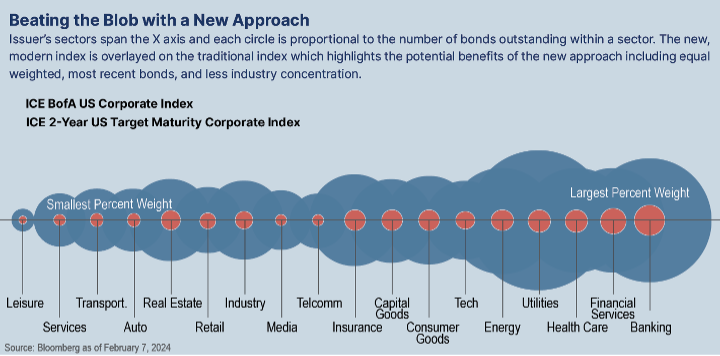

Serial issuers dominate the top holdings of the bond indexes, forming most of the thick end of the “blob” in Chart 1 below. As Chart 1 illustrates, a disproportionate share of the US Corporate Index is occupied by serial issuers, primarily banks and financial services, which together represent 28% of the index by weight. In addition, the index includes an unmanageably large number of individual bonds issued by these companies since it includes nearly all outstanding bonds from every issuer.

Defeating the Blob: A New, Modern Index Designed for Investors by Investors

Seeking to remedy this Blob Effect, F/m Investments teamed with ICE, a leading bond index provider, to create a new series of bond indexes that allow investors to control their interest rate exposure and avoid the Blob.

The new ICE US Target Maturity Corporate Indexes, by design, will not allow serial issuers to dominate, preventing Blob formation. Critically, the new indexes are built to be investible, with far fewer individual bonds and a preference for the most liquid bonds from each issuer.

These novel indexes are evenly weighted by issuer, choosing the most recent and liquid bonds issued. The resulting concentration on current coupon bonds can translate into higher distributable income and better liquidity.

Conclusion

Attacking the Blob Effect with thoughtful index construction aims to dramatically improve upon the decades-old method by meaningfully reducing industry concentration risk, better representing the current corporate bond market, and most importantly, introducing for the first time an investible index. After decades of dominating the world of bonds, the Blob may have finally met its match.

Disclosures

The information contained in this post is general in nature and for informational purposes only. It should not be considered as investment advice or as a recommendation of any particular strategy or investment product. This post is not a solicitation or an offer to buy or sell any specific security. We cannot guarantee the accuracy of information from third parties.

BPS – Basis points, otherwise known as bps are a unit of measure used in finance to describe the percentage change in the value or rate of a financial instrument

Coupon – A coupon payment refers to the annual interest paid on a bond. Coupons are expressed as a percentage of the face value and are paid from the issue date until maturity.

ICE BofA US Corporate Index tracks the performance of US dollar denominated investment grade rated corporate debt publicly issued in the US domestic market. To qualify for inclusion in the index, securities must have an investment grade rating (based on an average of Moody's, S&P, and Fitch) and an investment grade rated country of risk (based on an average of Moody's, S&P, and Fitch foreign currency long term sovereign debt ratings).

ICE 2-Year US Target Maturity Corporate Index is a subset of the ICE BofA US Corporate Index comprised of selected securities with a remaining term maturity of roughly two years. In order to qualify for selection, securities must be TRACE eligible with at least $300 million face amount outstanding and have at least 1.5 years but less than 2.5 years remaining years to maturity. Of the qualifying securities, one is selected per issuer based on the priority of (1) rank, (2) amount outstanding and (3) time since issue. For the rank, senior bonds are selected first, followed by senior secured and finally all subordinated debt.

Investors should consider the investment objectives, risks, charges and expenses carefully before investing. For a prospectus or summary prospectus with this and other information about the Fund, please call 1-800-617-0004. Read the prospectus or summary prospectus carefully before investing.

As with all ETFs, Shares may be bought and sold in the secondary market at market prices. Interest rate risk is the risk of losses attributable to changes in interest rates. In general, if prevailing interest rates rise, the values of debt instruments tend to fall, and if interest rates fall, the values of debt instruments tend to rise.

Investments involve risk. Principal loss is possible.

Distributed by Quasar Distributors, LLC

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.