Inflation: Too Hot?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsRelatively hot inflation reports might be blips, but they reinforce why the Fed's rate-cutting cycle might be more gradual, which could be a better backdrop for stocks.

A pair of hotter-than-expected inflation reports last week unsettled markets and further adjusted the expected start point to Federal Reserve rate cuts. Here, we take a look under the hood, specifically of the Consumer Price index (CPI) and its components, and whether we think it's indicative of the old adage about the "last mile" being toughest in terms of bringing inflation down.

Blip?

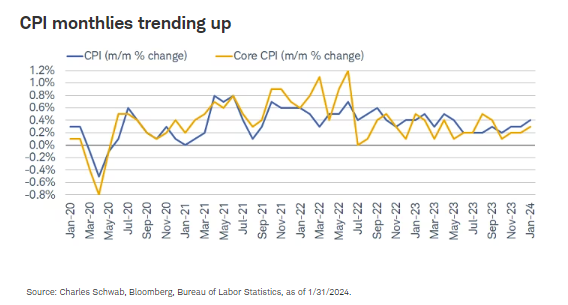

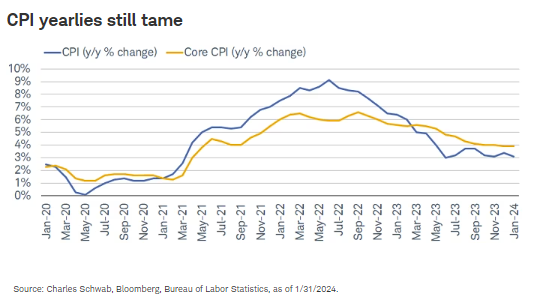

As shown in the first chart below, the headline CPI rose 0.3% month/month in January, with the core (ex-food/energy) up 0.4% month/month. Those monthly increases translated to 3.1% and 3.9% in terms of year/year for headline and core CPI, respectively.

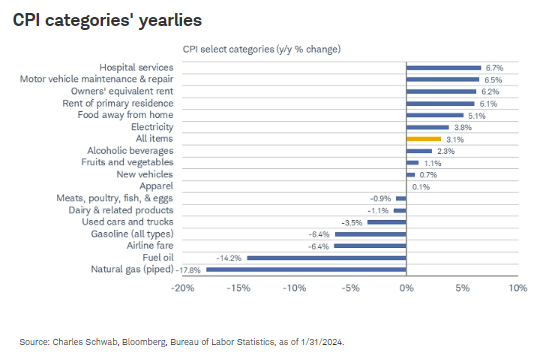

The services side of inflation continues to dominate the "hot" segments; with an ongoing (and sticky) increase in the CPI's shelter components—owners' equivalent rent (OER) and rent of primary residence (RPR) … more on that subject below. As shown below, particularly in year/year terms, those components' inflation rates remain uncomfortably high—alongside hospital services and motor vehicle maintenance/repair.

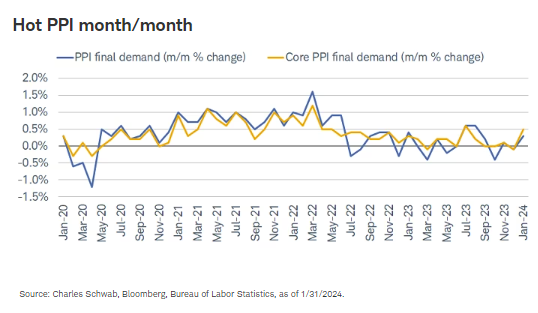

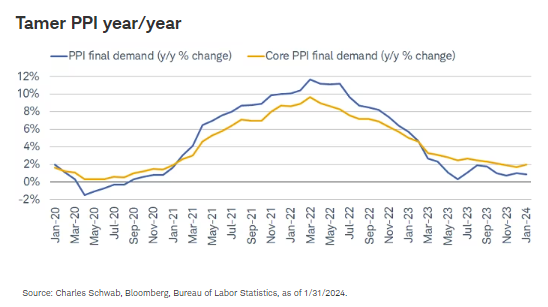

Unfortunately, for those in the "blip" camp were likely not pleased with the later release last week of the Producer Price Index (PPI). The month/month increases for both headline and core PPI were a bit troubling (first chart below); however, the year/year trends remained downward (second chart below).

What say you, Fed?

As it relates to prospective Federal Reserve policy, an important reminder is that the Fed's preferred inflation metric is the personal consumption expenditures (PCE) price index (January's reading will be released on February 29). The PCE preference dates back to the Alan Greenspan days, during which the 1996 Boskin Commission found that the CPI had been overstating inflation. It was later, in 2012, that the Fed adopted the 2% "formal" PCE inflation target.

The Fed's preference is also in part due to the PCE accounting for changes in how people shop when inflation jumps (e.g., consumers shifting away from expensive national brands to less expensive store brands). In addition, the CPI only tracks out-of-pocket consumer medical expenditures, while the PCE also tracks expenditures made on behalf of consumers, including employer contributions. Also significant is the weight of shelter in each index; with more on that below.

Because inflation has historically come in waves—and courtesy of the lessons (hopefully) learned throughout the 1970s—the Fed has pushed back on what was a high probability of a March start to rate cuts as recently as early last month. What could be particularly troubling to the Fed is the significant jump in the share of CPI categories with inflation rates running hotter over the past three months relative to the past 12 months.

Elevator up, escalator down?

There is an old adage about the Fed and how it approaches a full rate cycle—typically taking the "escalator up" (slower, more methodical shifts higher) and the "elevator down" (faster shifts lower, especially when combatting recessions). We think this cycle may continue to be the mirror image of that historical tendency—with the Fed clearly having taken the elevator up during its aggressive tightening cycle.

Any month now

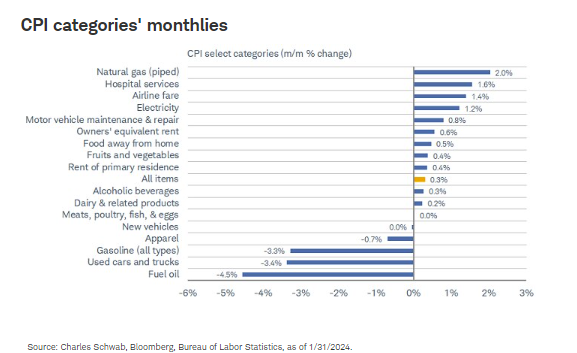

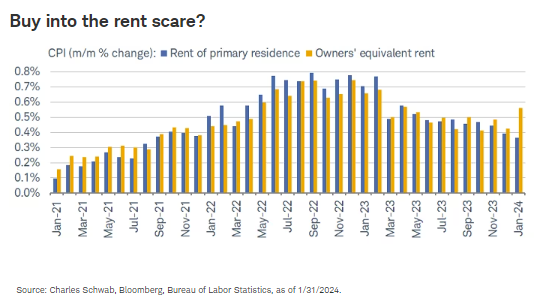

As noted, one of the biggest sources of consternation over January's CPI report was the unexpected jump in shelter costs. The shelter component increased by 0.6% month-over-month, the largest gain since February 2023. Interestingly, however, among the shelter category's components, the strong gains weren't widespread. As shown in the chart below, the RPR and OER subcomponents both increased but at markedly different rates. The former moved up by less than 0.4% while the latter moved up by nearly 0.6%. That might not seem like a large difference, but it marked the widest spread between both monthly growth rates since 1993.

There isn't yet a clear explanation as to why the gap widened so much in January, but it does open up a broader discussion about the shelter components in inflation metrics—especially CPI, given shelter's significant weight in the index. That statistic alone is the reason many investors and some central bankers often exclude it when looking at inflation. At the same time, however, shelter is still in core measures of inflation (be it CPI or the Fed's preferred gauge, PCE), so we as investors shouldn't ignore it completely.

In the CPI's shelter category, the two components with the largest weights are RPR and OER. The former's weight in CPI is just less than 8% while the latter's is much larger at 25%. That discrepancy means OER tends to receive more attention; if not for its weight, then surely because of how it's calculated. OER is an imputed metric; each month, the Bureau of Labor Statistics (BLS) asks homeowners how much they think they can earn if they were to rent out their home in a competitive market, then uses that to calculate the growth in "rents."

With home prices having reaccelerated, it's not difficult to see why OER has taken longer to slow down, which has gone against the consensus' call for shelter costs to fall quickly and accelerate the disinflation process. We often hear from reports, analyses, and conversations that it will happen "any month now." As long as home price growth stays elevated, though, we actually see scope for a slower and choppier path lower for OER.

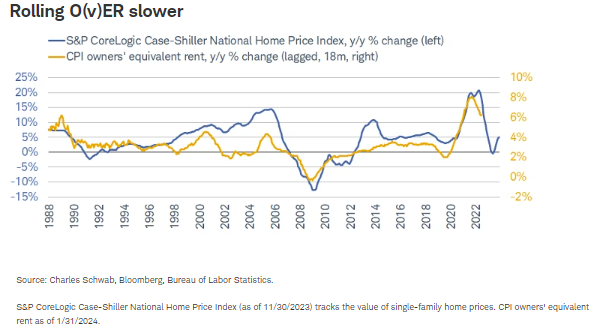

Looking at the chart below, there is a lagged relationship between actual home price growth and OER. Yet, the rub is twofold: it's not perfect, and if we're comparing the current cycle to prior spikes in OER (especially the late 1980s), home price growth at the current pace would be consistent with a much slower pace in OER growth. That hasn't happened yet.

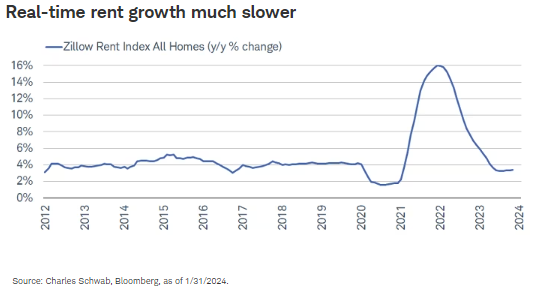

Many in the shelter disinflation camp have and will continue to point to "real-time" market metrics that suggest rent growth has already come down at a much faster pace. Indeed, that is true, evidenced by the full pandemic roundtrip in metrics like Zillow's Rent Index, as shown in the chart below.

However, that misses the point we're trying to emphasize via the prior chart. If OER is based on homeowners' perceptions of how much they can earn from renting their home—which is derived from how valuable their homes are—then a swift decline in OER seems less likely, given existing home prices are back to all-time highs (per S&P CoreLogic Case-Shiller data). This doesn't mean we expect to see OER growth permanently stuck in a higher range. We're simply pointing out the risk of shelter costs easing at a slower pace, which would complicate the disinflation path for core inflation. That also inherently gets to the point of homeowner affordability still looking quite poor—more so for new buyers, given mortgage rates remain elevated and home prices continue to move higher.

Know your CPIs and PCEs

Speaking of core inflation and discrepancies, it's also worth pointing out that there remains a large gap between the shelter components' weights in CPI and PCE. As mentioned, shelter is 36% of CPI. Conversely, housing's weight in PCE is just 18%. As noted, we'll get the January update for PCE at the end of this month, but based on the difference in weights alone, it's not out of line to expect a smaller bump relative to CPI (all else equal).

That supports the argument that the Fed might not be as nervous over the January CPI stat. That said, however, a good chunk of the public watches CPI and uses it as the preferred inflation gauge, so it's tough to believe that the Fed will shun the index altogether.

If anything, the main takeaway here is that the disinflation process continues to be choppy. The underlying data are all telling different stories, with the goods sector's disinflation and/or deflation, and the services sector's stickier inflation. Overall, though, the aggregate indexes are not yet convincing the Fed that its 2% target can be reached (and then sustained) just yet; evidenced by what FOMC members have said lately. Investors might argue otherwise, so that prompts us to remind readers of the following: there is often a big difference between what Fed watchers think the Fed should do and what the Fed will actually do.

Stock market, what say you?

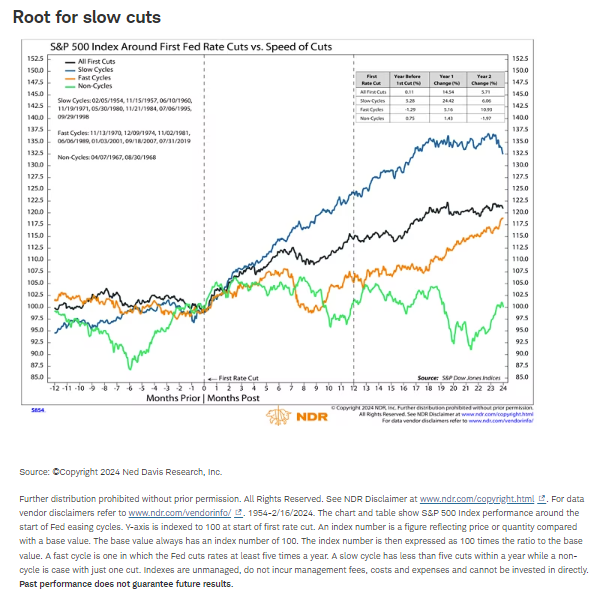

Equities' reaction to the CPI report was swift and brutal; but its recovery was equally swift. The market continues to price in both a later start to Fed rate cuts and fewer cuts this year; but that's not necessarily a bad thing from a market perspective. As shown below, historically (since the mid-1950s), stocks have performed better on average when the Fed was moving slowly (four or fewer cuts in a year) vs. more quickly (five or more cuts in a year).

Assuming inflation and the economy do not heat up so much such that rate cuts get priced out altogether this year, a milder pace of rate cuts and a later start may actually be a better backdrop for stocks this year.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All