When consumers fall behind, the credit card bill goes unpaid.

In our best teaching moments, we have helped our audiences overcome meganumerophobia, the fear of large numbers. Figures in the billions and trillions can sound scary and may lead to ominous inferences and conclusions. We encountered this last year, as the total balance on U.S. consumer credit cards reached one trillion dollars. Some thought that this was a sign that consumers were in trouble.

We did not rush to worst-case conclusions. Inflation drove up nominal card balances, and the credit card sum combines card holders who pay in full and those who revolve a balance. More broadly, debt can be used for any number of purposes, and we should not assume more debt is always a bad outcome. We look at delinquencies to judge whether households are overextended. And last week, the signal of debt performance became worrying.

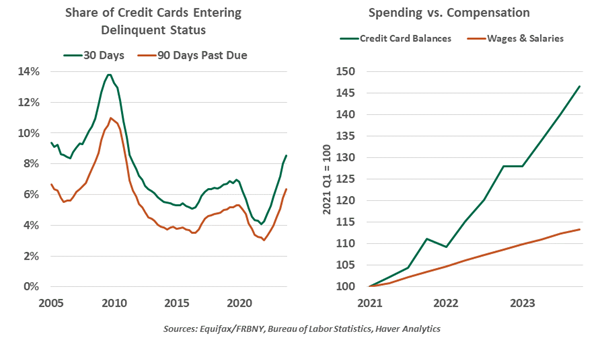

The share of credit card balances entering severe delinquency (90 days past due) has risen from a record low of 3.0% in early 2022 to a 12-year high of 6.4% at the end of 2023.

Total revolving card balances fell as stimulus payments were issued in 2020. Balances now stand 46% above their first quarter 2021 lows. Such a rapid rise in balances, far in excess of the rise in wages, suggests more delinquencies are still in the pipeline.

PAST-DUE DEBTS SHOW SOME HOUSEHOLDS ARE FALLING BEHIND.

Eventually, lenders will cease to attempt to collect bad debts and charge them off. The credit bureau TransUnion reports a record high of 4.6 million credit cards (over 1% of active accounts) were charged off in the fourth quarter. However, the dollar amount of charge-offs remains below the levels seen in the Global Financial Crisis.

While the credit outlook offers reason for concern, the overall consumer view is not yet worrying. The strong job market and rising wages have kept total household debt service ratios well contained under 10%. But a favorable aggregate story will obscure some households that are overstretched and are making difficult decisions about payment prioritization.

We do not suffer meganumerophobia. Large numbers are an occupational hazard. But rising delinquencies do give us a chill.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© Northern Trust

More Active Management Topics >