Secure lifetime income is a top wish-list item for defined contribution plan participants, and it has benefits for plan sponsors too. But there are very different ways to deliver it.

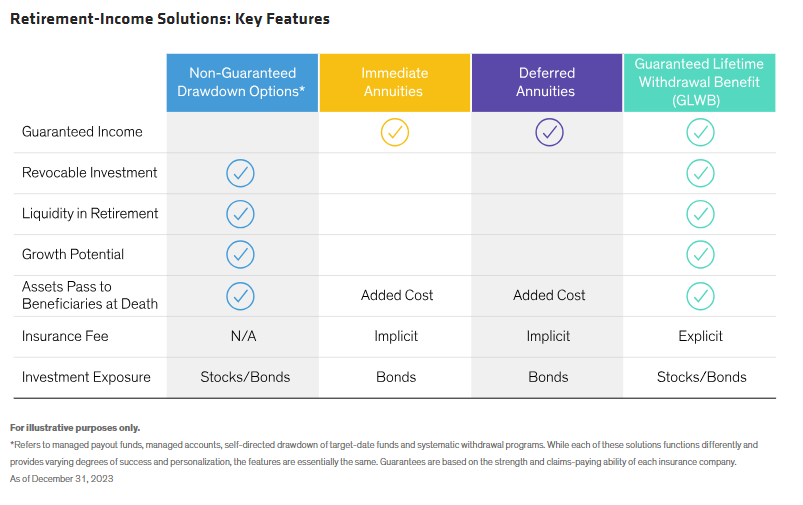

The first step in choosing a retirement-income solution is understanding the differences—which can be substantial—across the broad array of options. Let’s look at four categories of typical solutions, with a high-level view of how they work, as well as their costs and risks, summarized in the Display below.

1) Self-Insurance: The Non-Guaranteed Approach

One way to pursue retirement income is what many participants do today: they invest in a diversified solution, such as a target-date strategy, and forgo insurance—often managing withdrawals on their own. Participants keep full ownership of and liquidity in their retirement savings, have growth potential based on their asset allocations, and can pass remaining account balances to their beneficiaries at death.

The drawback of self-insurance is uncertain income, and participants tend to overestimate or underestimate their sustainable withdrawal rates. As a result, they may have to reduce the percentage of assets they withdraw, lowering their amount of income and their living standard as a result. Or they can continue withdrawing the same amount of income and risk running out of assets. Participants who don’t want these risks are more likely to favor income insurance—a feature of the next three solutions.

2) Single Premium Immediate Fixed Annuity (SPIA)

A SPIA, also referred to as an income annuity, is among the most well-known annuities. At retirement, participants surrender their assets to an insurance company (a decision that can’t be revoked). In exchange, they receive guaranteed fixed payments that start right away and continue for life. SPIAs have no explicit annual insurance premium or fees, because participants no longer own any assets.

Outcomes for participants depend heavily on their age of death; half will die before the median life expectancy, failing to reap the full income benefit. Adding death-benefit riders can reduce the loss from dying early, but at the cost of a lower income rate. Participants living longer receive bond-like returns for decades: they no longer risk outliving their assets, but they sacrifice the liquidity and growth potential of target-date funds.

3) Deferred Fixed Annuity

A deferred fixed annuity, such as a qualified longevity annuity contract (QLAC), requires participants to surrender their assets up front, like the SPIA. But with a QLAC, income payments start many years later. A person surrendering their assets at age 65 might receive payments starting at age 80. In exchange for waiting, payment rates are higher than those of a SPIA. Participants must manage their own assets and avoid running out of money until guaranteed income payments start.

As with a SPIA, participants with QLACs forgo the liquidity and growth potential of the assets they surrender to the insurer. The deferred payments make outcomes more sensitive than a SPIA to the age of death. For example, a person who dies before payments start may get nothing. Adding death benefits can address this, but they reduce the income rate. QLACs also face more inflation risk: fixed payments are bought many years before they start, so rising prices will reduce their purchasing power. A QLAC’s income level is more sensitive than a SPIA’s to prevailing interest rates at the time of purchase, so participants face more market-timing risk and potential buyer’s remorse.

Fixed annuities like the SPIA and QLAC face significant risks and impose implicit costs that are neither transparent nor clearly visible at purchase. This sets up a potential unwelcome surprise for those who don’t fully understand them.

4) Guaranteed Lifetime Withdrawal Benefit (GLWB)

A GLWB is a lifetime income insurance contract on a participant’s investment portfolio. Participants keep ownership of all their assets and retain growth potential, because assets covered by the GLWB are typically invested in a well-diversified mix of stocks, bonds and inflation-sensitive assets.

Guaranteed income is initially withdrawn from the participant’s insured portfolio. If that portfolio runs out of funds, an insurer (or insurers) steps in to pay guaranteed income for the rest of the participant’s life. The GLWB also includes “step up” provisions that may boost income if the insured portfolio grows with rising markets. If there’s a balance left when the participant dies, it’s transferred to beneficiaries.

A GLWB contract charges an annual insurance premium—typically a percentage of the insured portfolio balance. Insurance can be bought before or at retirement, and participants can cancel some or all of it at any time with no restrictions, so they benefit from liquidity and flexibility.

The specific features, costs and risks of these representative retirement-income solutions vary quite a bit, and some risks and costs aren’t obvious on the surface. Understanding the distinctions is a vital step for plan sponsors to take in assessing which one is best suited to meet the individual needs of each plan participant.

“Target date” in a fund’s name refers to the approximate year when a plan participant expects to retire and begin withdrawing from his or her account. Target-date funds gradually adjust their asset allocation, lowering risk as a participant nears retirement. Investments in target-date funds are not guaranteed against loss of principal at any time, and account values can be more or less than the original amount invested—including at the time of the fund’s target date. Also, investing in target-date funds does not guarantee sufficient income in retirement.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein