Investors who stay too long in cash may find they’ve missed out.

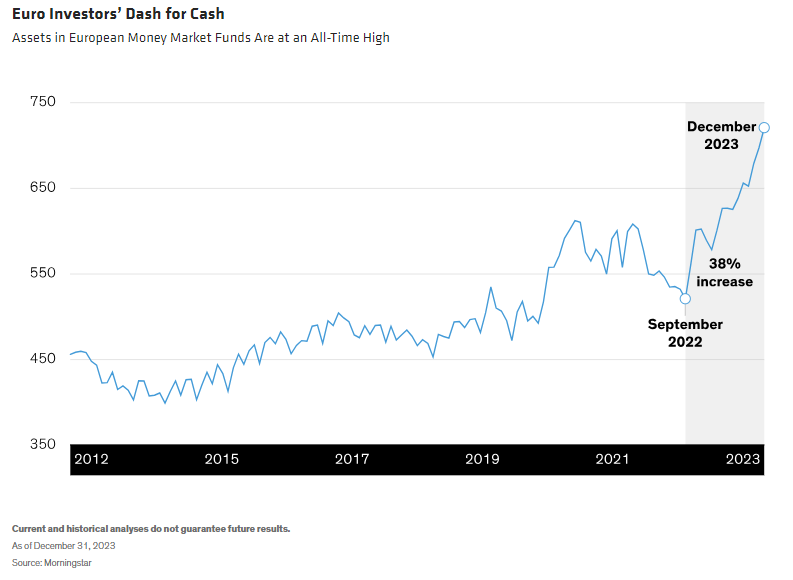

A challenging economic backdrop combined with historically high cash yields has driven many investors to favor low-risk, liquid assets such as money market funds (Display).

Now we believe the balance of risks for euro investors is changing. If you’re among the many investors sitting on the sidelines, now’s the time to get in on the action. Here’s why.

With euro-area inflation easing, rate cuts will likely drive bond prices higher and cash yields lower. Investors bold enough to lock into fixed-income investments now will continue to earn current high income levels and may enjoy capital gains too.

Our analysis—based on a longer US data history—shows that assets tend to flow out of money market funds when the central bank starts to ease monetary policy. On that basis, we believe that euro money-market flows will likely soon reverse as assets are redirected to bond markets. Considering the very large sums involved, the impact on bond prices could be substantial.

Timing Is Critical: Don’t Miss Out

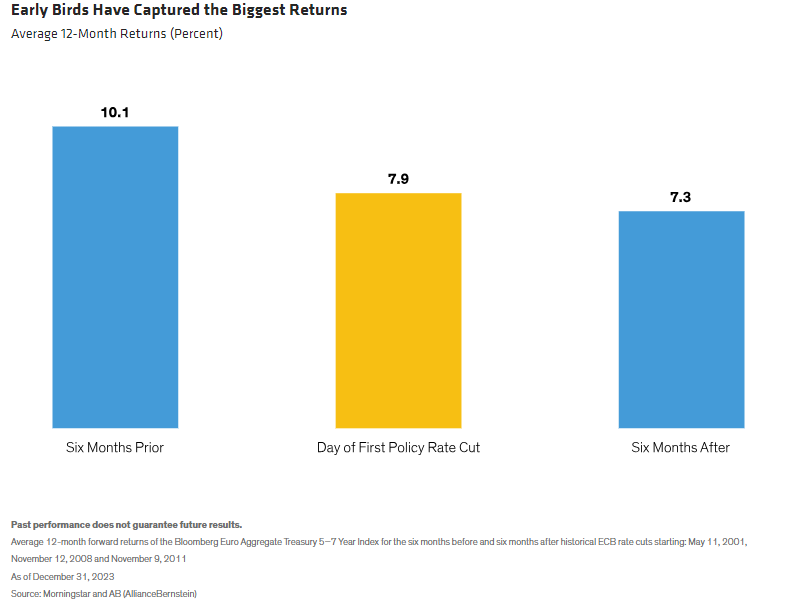

The European Central Bank (ECB) is getting closer to cutting interest rates and has signaled that rate cuts may start in the summer; the market consensus indicates cuts may come as early as April. Timing is important because, historically, bond prices have started to rise ahead of a first rate cut. The investors who made the biggest gains were those who moved early (Display). Investors who stayed on the sidelines, waiting in cash deposits or money market funds until rates changed, missed out on the early gains.

We believe that investors should aim to get ahead of the ECB’s first rate-cut decision. That means making the switch now.

Cash Yields Look Set to Dwindle

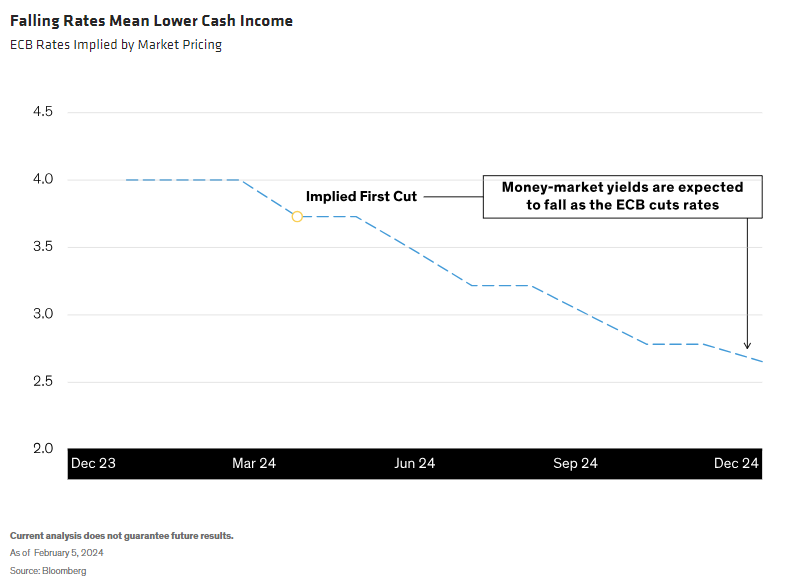

Meanwhile, investors who stay sitting in money market funds will likely see their yields decline progressively, resulting in a lower annualized return than they may have expected, given starting cash yields. While the exact path of cash deposit rates is hard to predict, the likely trajectory is clear—down (Display).

Although money market funds may currently offer attractive starting yields, their underlying investments are short-term, and with each cut in rates the maturity proceeds of those securities must be reinvested at lower yields. By switching to longer-term fixed-income investments, investors can delay that reinvestment risk in line with their choice of bond maturities.

Yields May Surprise, but Asymmetry Favors Bondholders

In a troubled world, it’s important to consider the downside. Geopolitics remain worrisome, and global conflicts could trigger an inflation shock to change the rates outlook. Services inflation and related private sector wage rises have been sticky and could continue to trouble policymakers, putting upward pressure on rates. Even so, we believe the potential downside risks to bond prices are well compensated by current high bond yields.

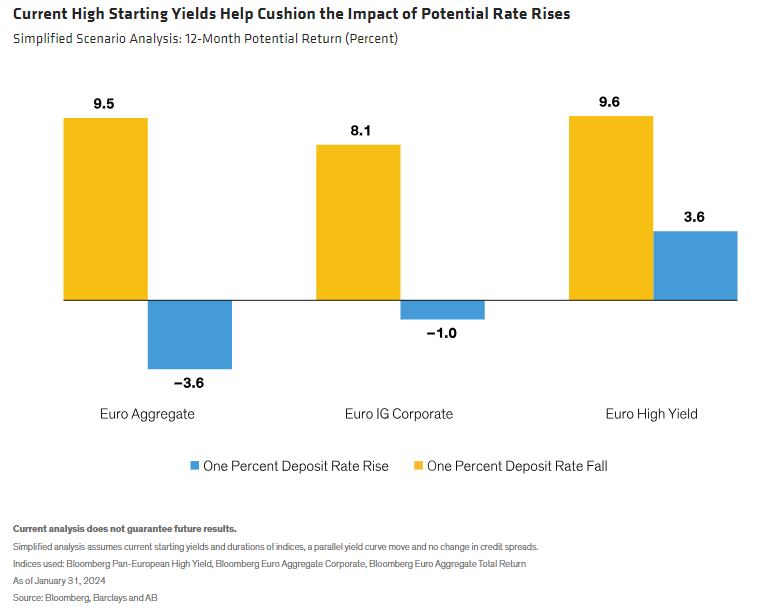

In our analysis, today’s yields provide a big enough cushion to mostly offset the impact of a possible 1% rate rise, while providing high single-digit gains in the event of a likely 1% rate cut (Display). Although risks remain, this asymmetry of outcomes favors bondholders.

Time Is of the Essence

Euro fixed income currently offers yields that are very high relative to recent history and have scope to fall to much lower levels and generate attractive gains. Meanwhile, struggling euro-area economies cannot tolerate current high interest rates indefinitely. Ultimately, the question is not whether to move out of cash, but when.

Investors can expect continued volatility as yields trend lower over the next few months. However, given a likely surge in demand for bonds and expected erosion of cash yields, investors who act now can position themselves for strong potential returns. That’s why, while cash has ruled in the past, there’s no time like the present to switch to fixed income.

The author would like to thank Vishali Thakker, Fixed Income Product Manager, for her invaluable contribution to this research.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our YouTube channel.

© AllianceBernstein

Read more commentaries by AllianceBernstein