Walking through our house before we purchased it, the home inspector noticed that the hot water heater was showing its age. I asked how we would know if it was failing, and he shrugged. He said we’d know when one of us found ourselves taking an unexpectedly cold shower.

All was well, until it wasn’t. The heater failed quietly and without warning, leaving me shivering for want of heat. At that moment, more than most moments, I appreciated the essential nature of heat and the energy that produces it. We take the availability of energy for granted, and disruptions can be a major shock.

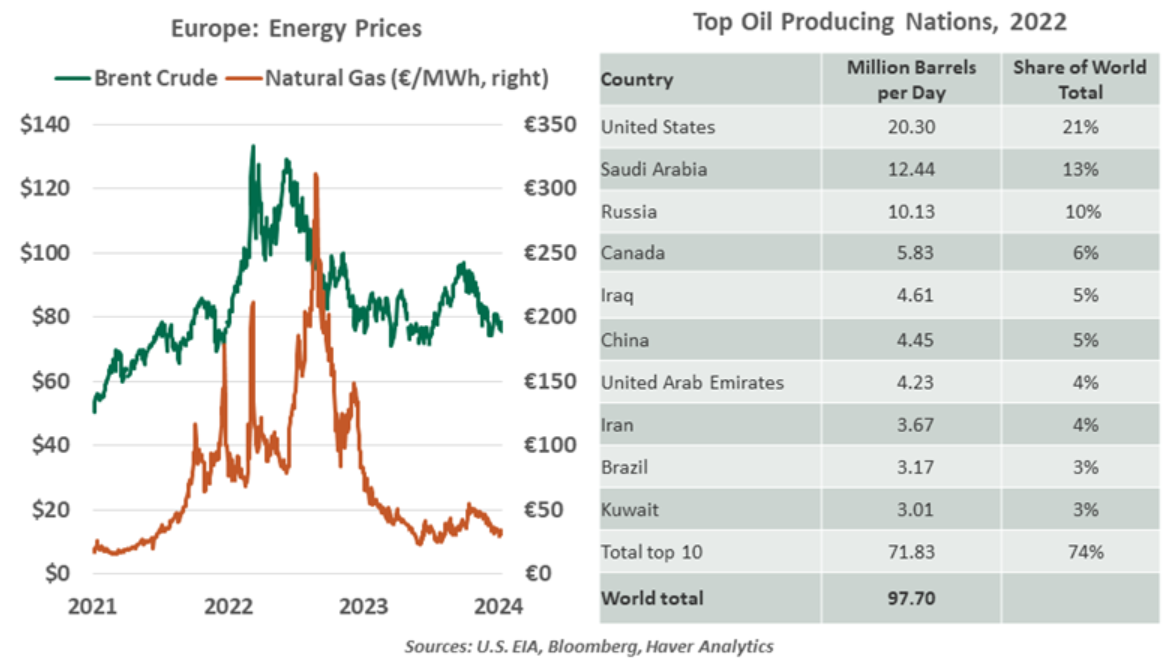

The energy market has had significant ups and downs over the past four years, across regions and products. Pandemic stops and starts distorted consumption patterns. Russia’s invasion of Ukraine, and the ensuing sanctions on Russian energy exports, caused rapid spikes to energy prices and contributed to high global inflation. Energy production and trade flows settled into a more normal state over the course of last year, but there remain many reasons to fear of a new round of volatility.

Throughout 2023, the Organization of Petroleum Exporting Countries and their allied producers (OPEC+) incrementally reduced their output targets by a total of five million barrels per day, hoping to keep oil prices elevated. These announcements did move markets, but the impact was temporary. Global demand was muted, especially amid China’s manufacturing slump. Non-OPEC nations, notably the United States, are producing more oil, blunting the cartel’s control of prices. Frustrated, some OPEC+ members have quietly increased their exports.

The Israel-Hamas conflict has sparked fears of disrupted energy transit or stricter sanctions on producing nations. Thus far, prices and production have been stable.

The surprising growth of oil extraction in the U.S. has done the most to keep markets calm. Prior to the pandemic, the rise of hydraulic fracturing (or fracking) made the U.S. a major growth market for oil production. However, the higher cost of fracking limited its profitability, and when demand plunged during the pandemic, many producers became insolvent. The environmental hazards of fracking and policy shift toward green energy set a base expectation that fracking’s heyday was in the past.

However, this form of production has rebounded, making the U.S. the highest-volume producer of both oil and liquified natural gas (LNG) in the world. While the quantity of drilling rigs has declined, operators have found ways to make existing wells more productive. And more projects are scheduled to come online in Texas and Louisiana this year to expand LNG capacity.

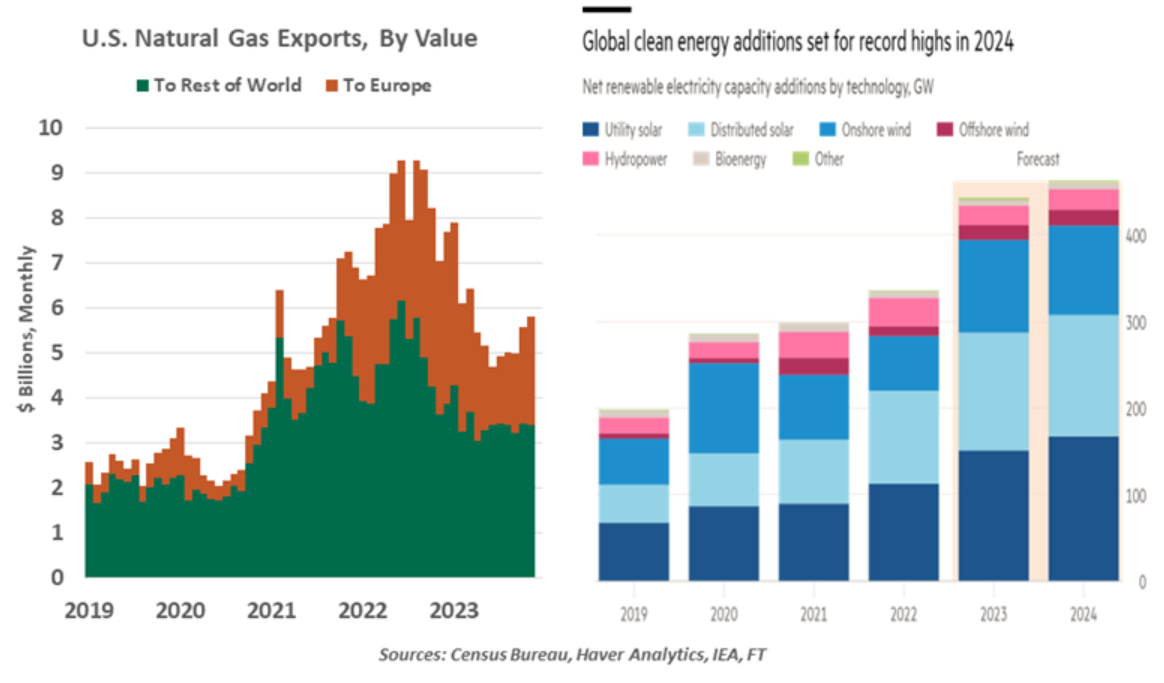

The higher level of U.S. output has pushed up the nation’s energy exports, helping to keep global prices contained. This has been a particular benefit to Europe, the continent facing the most salient risks to energy supply. The dissolution of trade with Russia revealed the structural dependency that many European nations had upon Russian energy. Natural gas was the point of greatest concern, as the termination of pipeline flows sparked fears of energy rationing. Gas prices surged, forcing Europeans to find other sources of gas.

Europe narrowly avoided a winter recession last year, supported by stockpiling, conservation efforts and the luck of mild weather. European nations have invested in their capacity to receive and store oil and gas imports. The resilience seen in the wake of Ukraine has bolstered hopes that energy markets can withstand any disruption stemming from the latest conflict in the Middle East.

The U.S. has resumed its place as a major energy producer.

Steadily low prices have also given the U.S. an opportunity to replenish the Strategic Petroleum Reserve (SPR). To combat inflation, nearly half the stock of the SPR was drawn down from July 2021 through December 2022. While still depleted, recent weeks show a very small increase in the stock. While price arbitrage was never an intended use of the SPR, as long as oil prices stay low, the U.S. may have succeeded in selling high and buying low.

The current focus on petroleum-based energy sources may feel out of tune with the buzz around clean energy. The transition toward renewables will be a long-running project, and the need for oil will not subside anytime soon. But make no mistake, the transition is underway. Both public policy and private investments are supporting the growth of renewables. Geopolitical conflict and a year of record-breaking heat have only added to the case for transitioning away from fossil fuels.

The move to alternative sources of energy will not be a panacea. Sources like wind, solar and tidal energy each have their limitations and tradeoffs—but so do hydrocarbons. A wider array of energy will reduce the role of unreliable actors and hedge the exposure to volatile supplies and prices.

The growth of alternative energy sources should reduce vulnerability to oil and gas shocks.

The years ahead are poised to be an inflection point in the green transition. Governments have made major commitments to support sustainable energy, from the $369 billion of clean energy programs in the U.S. Inflation Reduction Act to the European Commission’s €300 billion REPowerEU program. Projects of that scale take years to plan and implement. Global clean energy investments in 2024 are forecast to reach a record high of 460 gigawatts of output, led by solar energy infrastructure.

A plumber replaced our hot water heater without much fuss. But the cold shower made me regret not taking action before the tank failed. The shocks of the past two years have awakened many nations to the need to be prepared for thermal deficits. Unlike the mistake I made, they are heeding the warnings.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.