It’s hard to chart a course through equity markets in times of uncertainty. Here are our thoughts on some of the big questions on investors’ minds today.

Global equity markets posted healthy gains in 2023, but investors enter the new year with many concerns. As macroeconomic uncertainty lingers after a year of extreme market concentration, equity allocations should be prepared for a range of scenarios.

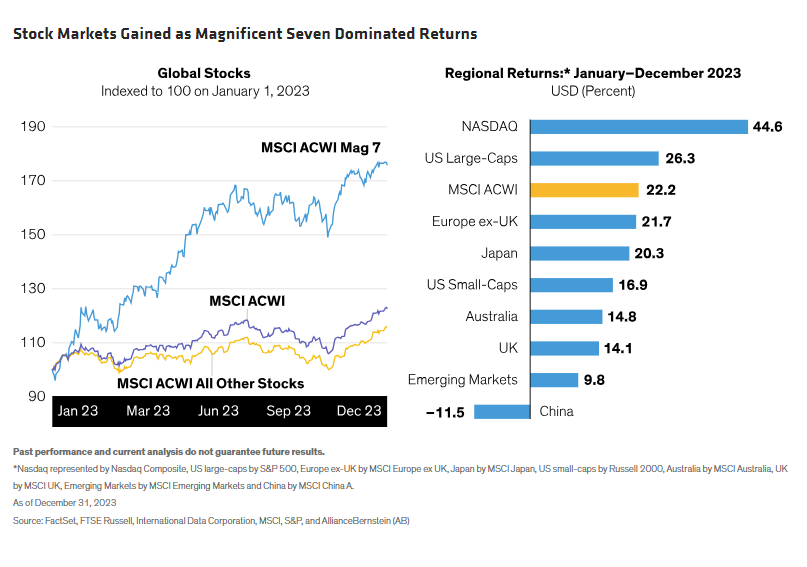

The last two years were practically a mirror image for equity markets. In 2023, the MSCI ACWI Index of global stocks rose by 22.2% in US dollar-terms, after falling by 18.4% in 2022. Yet the market trajectory was anything but smooth. First-half gains were marred by volatility from US banking failures. Then, after peaking in early August, the MSCI ACWI Index fell through October before recovering through year-end (Display). We believe that market fluctuations in the second half of the year reflect investors’ lack of conviction in the path of macroeconomic growth.

Japanese stocks performed well, as the economy and companies benefited from the long-awaited impact of Abenomics reforms, as well as a reversal of two deflationary decades and a weaker yen. Emerging markets underperformed, with Chinese stocks suffering a particularly tough year. US market gains were dominated by the so-called Magnificent Seven (Mag 7)—a group of giant companies perceived to be big winners of the artificial intelligence (AI) revolution. These stocks accounted for 58% of the S&P 500’s returns in 2023.

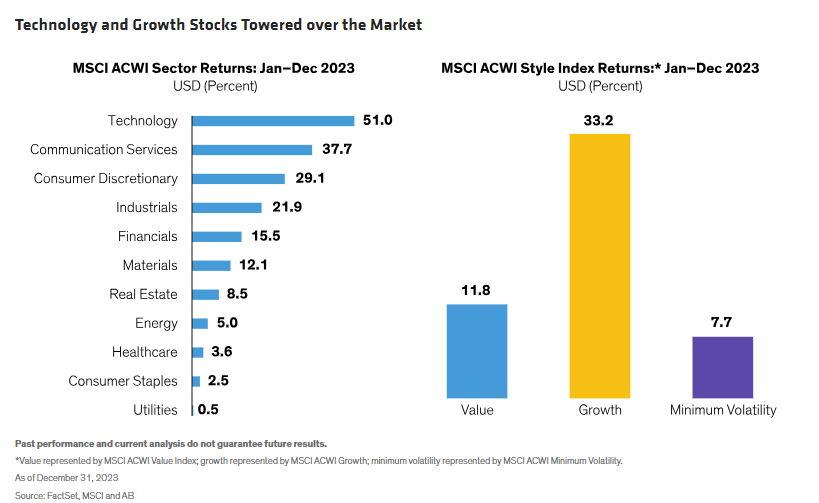

Heavily concentrated returns reflected lopsided style performance. Growth stocks surged by 33.2, eclipsing value and minimum-volatility stocks (Display). The technology and consumer-discretionary sectors—home to the Magnificent Seven—towered over the market, along with communications. Utilities, consumer staples and healthcare were the biggest laggards.

We believe that the magnitude of AI-driven equity returns is indicative of a growing thirst for earnings growth amid a shaky economic outlook. How this tension resolves could determine the course of equity markets and individual company performance during 2024. It’s also the source of key questions investors are asking, including:

1. What is the potential range of macroeconomic scenarios in 2024?

Inflation pressures have eased around the world during 2023, removing a burden on global macroeconomic growth. Global unemployment rates are low by historical standards. Yet central banks are still cautious: policy rates and bond yields remain high globally and are likely to stay elevated well into 2024 before retreating.

AB’s economists expect a soft landing for the global economy this year. Slower growth should keep inflation in check, which in turn should allow central banks to start cutting rates as the year progresses. But every region faces unique growth, inflation, monetary and fiscal policy circumstances that could lead to wide variations from this forecast. There are also significant downside risks to this forecast, especially given geopolitical hazards from war in the Middle East and Ukraine to US/China tensions and US elections.

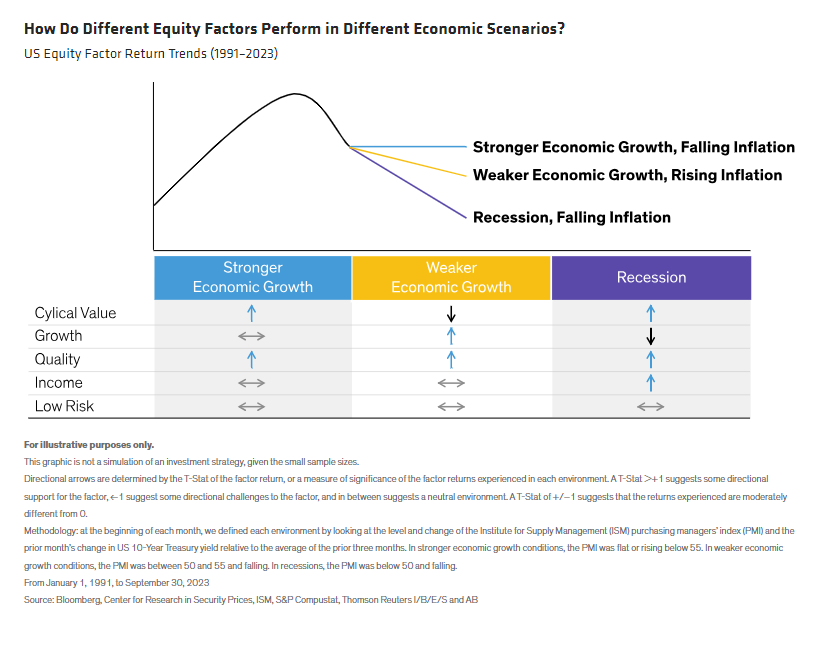

Different equity strategies are sensitive to the potential outcomes in different ways. Our research of US equity factor returns in varying economic scenarios from 1991 to 2023 is instructive (Display). In scenarios with stronger economic growth and falling inflation, cyclical value stocks have generally performed well, while growth stocks have lagged. When economic growth was weaker and inflation was rising, growth factors performed well. But in a hard landing—i.e., recession—past performance suggests that strategies featuring strong profitability or higher levels of dividend yield provide the best cushion.

Quality factors performed well in all three environments. In a world of higher inflation and interest rates, we believe that stocks with quality features will continue to deliver by virtue of their focus on balance-sheet strength and profitability, which underpin financial resilience.

2. Will high inflation and interest rates be big hurdles to equity returns?

In an inflationary world, equities must generate high nominal returns to deliver positive real returns, above the inflation rate. That’s a high hurdle for equity portfolios at a time when economic growth is under pressure.

The good news is that inflation is settling down. AB economists project global inflation of 3.5% in 2024, with a rate of 2.5% in the US and 2.2% in Europe. Though that’s higher than what we’ve been used to in recent decades, it’s much lower than the extreme post-pandemic spike in 2022, when global inflation exceeded 7%.

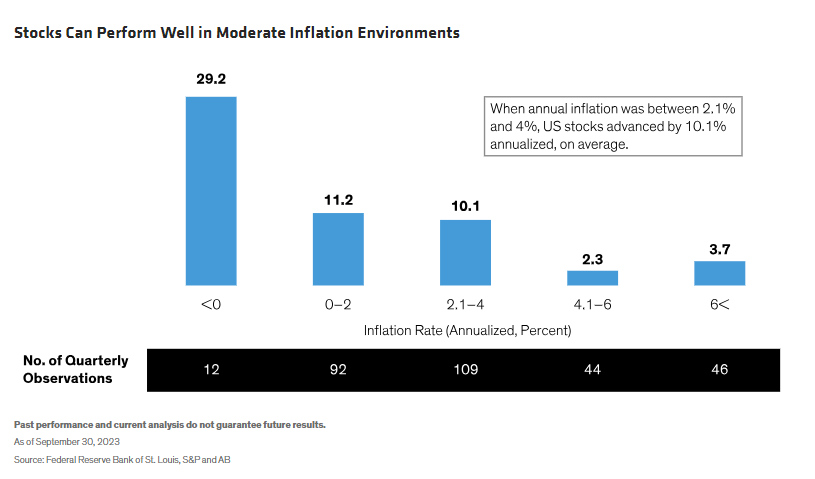

For equities to deliver positive real returns, the level of inflation matters. We looked at inflationary periods from 1948 to today and found that US equities did well in moderate inflation environments (Display). When the inflation rate was between 2.1% and 4.0%, the S&P 500 delivered an annualized return of 10.1 on average, handily beating the rate of rising prices.

Here’s another way to look at it. During periods of higher inflation and higher interest rates, bond yields tend to be higher. That leads to a decline in the equity risk premium (ERP), the excess return that investors expect to earn over a risk-free rate. However, between 1983 and 2008, when the ERP was at a similar level to today, the S&P 500 delivered solid annualized returns of 10.2%.

3. Why shouldn’t investors simply load up on the Magnificent Seven?

Although macro risks weighed on the market this year, generative AI galvanized investors around a technology paradigm shift, with the potential to unlock productivity gains and profitability. This prompted a powerful surge of the Magnificent Seven stocks—Alphabet Inc. (Google), Amazon.com, Apple, Meta Platforms, Microsoft, NVIDIA and Tesla. By year-end, they made up 28% of the S&P 500’s market cap.

Of course, the US mega-caps include some great businesses. We believe that equity portfolios should include or exclude individual names at appropriate weights based on their investing philosophies. However, their trading patterns have become tightly correlated, so investors who load up on all seven stocks could get burned if sentiment toward the entire cohort sours.

The AI revolution that has supercharged their returns will also lead to greater competition between the mega-caps, which could affect profitability. And we believe that it’s too soon to know who the big winners of the AI revolution will be, as the technology is just beginning to find commercial applications. At previous technology turning points, companies that invested heavily in the infrastructure were not necessarily the ones that monetized and profited most.

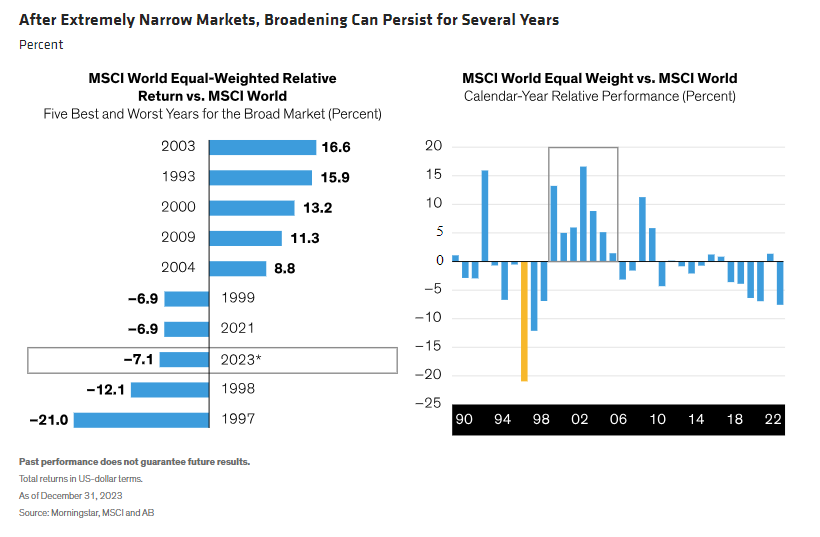

During 2023, the equal-weighted MSCI World underperformed its corresponding cap-weighted index by 7.1% (Display). History suggests that after extremely narrow returns, when a broadening of the market materializes, it can persist for several years. Nobody can predict when that might begin. But after more than 70% of S&P 500 constituents trailed the market in 2023—with shares of many companies underperforming their own earnings growth—we think the dominance of the Mag 7 is unlikely to persist.

Market concentration creates a dilemma for active investors. Portfolios that didn’t hold the entire Mag 7 group generally underperformed the market. In a concentrated market, simply choosing not to hold a mega-cap stock creates a large underweight and adds significant benchmark risk. This is a strategic issue that portfolio managers must address.

How to Position Amid the Uncertainties

At the start of 2024, investors are confronted with a long list of risks. Earnings forecasts are trending down, while equity valuations are somewhat elevated in some parts of the market—particularly in the US. It’s hard to develop conviction in a likely macroeconomic outcome. Market concentration cannot be ignored. And the potential impact of geopolitical risk is hard to predict.

In such a fluid environment, we think investors should focus on long-term investment outcomes by creating balanced allocations of different equity strategies, which can unlock diverse opportunities that can’t necessarily be captured in a single portfolio. Portfolios that capture secular growth themes, via companies with high-quality business models, can do well in a tougher economic environment. Investing in growth companies that have solid three-to-five-year earnings forecasts can also be rewarding, as we believe that the market may be overlooking long-term potential because of a lack of short-term visibility.

Value stocks deserve attention. Many investors have been underweight value, which has been out of favor for several years. Yet value stocks have historically done well in softer- and harder-landing environments, making them important for a balanced allocation today.

If volatility strikes again, strategies based on quality stocks with more stable trading patterns can help cushion the downside. Lower-volatility strategies add defensive attributes to an allocation that can help investors stay the course in tougher markets.

Finding the right balance will differ based on individual investor risk appetites. But in our view, the key to navigating equity markets in 2024 is to be wary of developing false conviction in a single macro or market outcome. Equity portfolios of all types must identify companies with the right attributes to traverse a wide range of scenarios—and investors should review their allocations to ensure they create the right strategic recipe for capricious market conditions.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© AllianceBernstein

Read more commentaries by AllianceBernstein