The ECB will pivot in 2024, but probably not as early or swiftly as markets predict.

The Federal Reserve isn’t the only central bank that stands accused of reacting slowly to disinflation. The European Central Bank (ECB) came under criticism last week when eurozone inflation fell 50 basis points to a 28-month low of 2.4% for the twelve months ending in November. While the Federal Open Market Committee outcome on Wednesday will be a highlight of next week’s news, the ECB decision the following day will also be closely watched.

Following three consecutive months of below-consensus inflation readings in the eurozone, markets are pricing in almost six quarter-point rate cuts by the ECB in 2024. Odds of a cut in March are over 70%. This implies that the ECB will not only be the first among major central banks to pivot next year, but will also deliver the most aggressive easing cycle.

The recent deceleration in inflation does not come as a surprise. Shocks related to global supply chains and the war in Ukraine have eased, and global energy prices have been on the decline. In addition, the eurozone economy has been slowing noticeably, highlighted by recession in Germany.

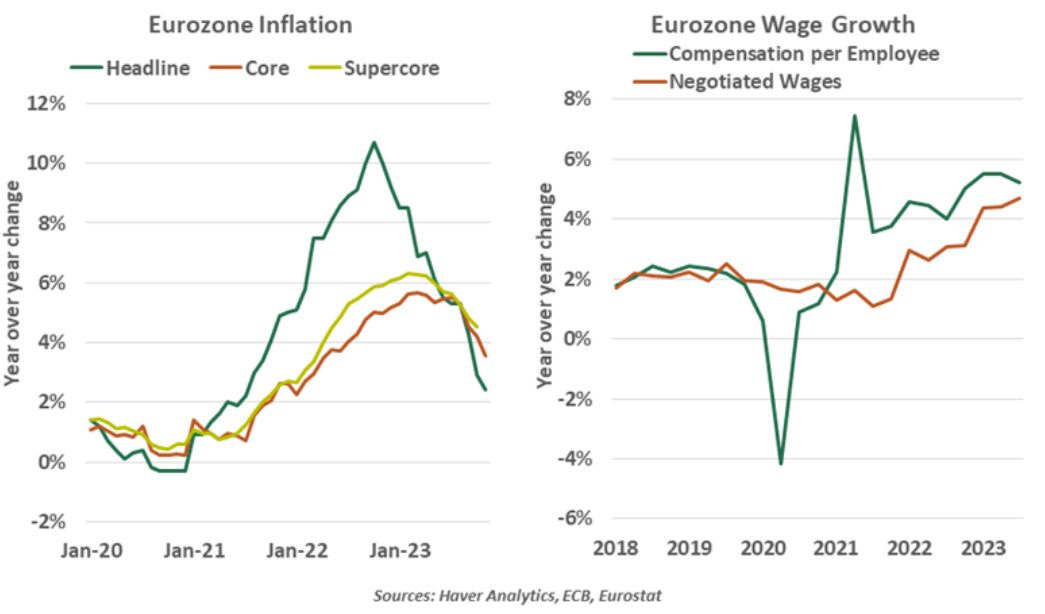

The disinflation has been broad-based across major components. The supercore measure, which is based on those items which are sensitive to slack or output gaps, has dropped from a peak of 6.3% year over year at the start of 2023 to 4.5% in October. One-off factors can affect price indexes, but extreme price movements are becoming less common.

In addition to these encouraging developments in inflation and its alternative measures, signs of moderation in eurozone wage growth are emerging. The latest pay data are signaling a likely undershoot of ECB expectations for a 4.3% average increase in 2024, consistent with signs that the labor market is starting to loosen. But Europe’s labor markets are still tight, with the unemployment rate at a record low of 6.5%. While wage pressures have likely peaked, gains are still too strong to support a return to the 2% inflation target.

Both survey- and market-based inflation expectations remain elevated. According to the ECB’s latest consumer expectations survey, inflation is expected to average 4.0% over the next 12 months and 2.5% over the next three years. Both readings are above the ECB’s 2% target.

Comments from ECB officials have ramped up early pivot wagers. Doves have cited the need to cut soon “to avoid unnecessary damage to economic activity and risks to financial stability.” But German central bank chief Joachim Nagel pushed back, stating that it was “far too early to even think about a possible reduction in key interest rates.” The debate within the ECB governing council next week should be especially active.

Most economists (ourselves included) are still cautious and expect only a gradual easing cycle from the ECB commencing around the middle of 2024.

A decision to remain on hold next week will likely be a no brainer for the ECB, but the communication challenge for the group will be to keep all possibilities open without coming across as too dovish or disconnected from reality. And the messaging will have to be phrased in a manner that resonates across 20 countries.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

Market trends are shifting – is your investment strategy keeping pace? Join industry experts as they delve into the equity and bond markets, offering insights into the 2024 outlook. Register for our Market Outlook Symposium, on December 14th at 11 am ET. Click here.

© Northern Trust

Read more commentaries by Northern Trust