A secure lifetime income solution can seamlessly continue the “do it for me” structure that has helped DC plan participants save in their working years.

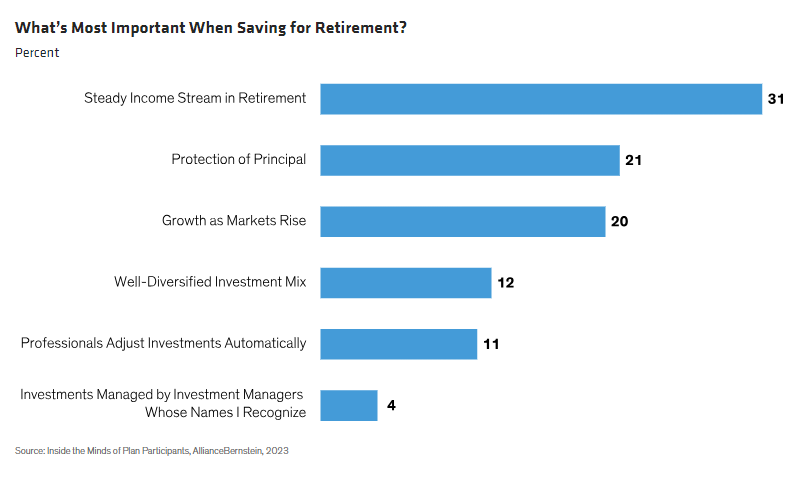

Demand for defined contribution (DC) solutions delivering secure lifetime income through insurance guarantees is growing. Defined benefit (DB) plans, with their built-in income, have been dwindling for decades, even as retirement income tops participants’ wish lists (Display). Many need help getting it, because they're not clear on how much they can withdraw from their savings in retirement.

In our latest participant survey, we asked: “Imagine for a moment that you retired at age 65 and had $500,000 in your retirement account. What percentage of that $500,000 could you probably spend each year during retirement without running out of money for the rest of your life?”

Nearly half (45%) of respondents said they could withdraw 7% or more; nearly one-third said 10% or more. Those excessive rates could cause participants to run out of money early in retirement—even in good markets. Even if participants withdraw prudently, poor market outcomes can still cause those with an average life expectancy to deplete their accounts.

Some participants try to go it alone without income insurance; they “self-insure.” But if they overestimate how much they can take out, they might outlive their savings. And if they withdraw too conservatively to avoid running out of money, they could fail to take full advantage of their savings.

Bear in mind that retirement expenses are generally fixed—or even rising. The lack of a predictable year-to-year income creates a lot of uncertainty—and may require tough decisions in bad years.

Automation: A Boon for Retirement Savings

Incorporating insurance may help participants translate their savings into lifetime income more efficiently while significantly reducing the risk that they outlive their money. For example, showing participants how much income they’re building can encourage them to save more and stay invested during their working years.

We think building on automation’s success is the key to better income outcomes.

Two-thirds of plan sponsors have reported “direct and attributable” benefits from auto features—including higher participation, faster asset growth and better participant behavior. With automation and qualified default investment alternatives (QDIAs), participants don’t have to be investment experts to save effectively. Essentially, they can do nothing and still enjoy the potential for better outcomes. That’s a very DB-like benefit.

However, most participants can’t simply “do nothing” and arrange lifetime income for their retirement phase. Very few have the know-how to do this successfully; if they’ve never made an investment decision, they’re not likely to become overnight experts in designing sustainable income.

Plan Sponsors’ Incentive for Lifetime Income Solutions

The next logical step in improving retirement outcomes, as we see it, is to automate income benefits through a default path.

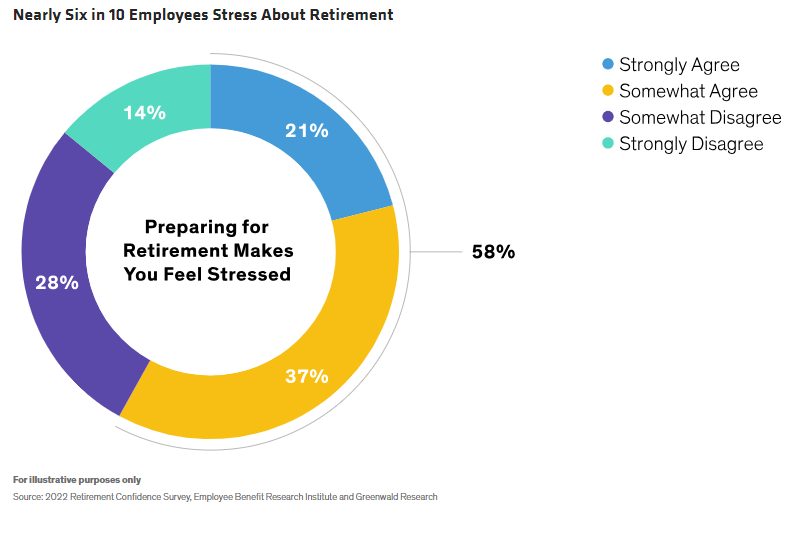

Plan sponsors have incentive to act, because employees worried about retirement readiness can take a toll on organizations—and many workers are worried (Display). This problem can close avenues for newer workers to advance, because those near retirement aren’t confident enough to retire. That roadblock could lead frustrated up-and-coming talent to seek greener pastures.

Lost earnings and productivity can hurt, too. One study put the annual cost for every year delay in one worker’s retirement at roughly $50,000, given the cost difference between retiring and entry-level workers. The higher the worker’s skill level, the higher the cost. Financially stressed employees are also more likely to seek new jobs, be less productive and log poor attendance records.

The Lifetime Income QDIA: a “Do It for Me” Income Solution

A guaranteed lifetime income QDIA can alleviate employees’ stress, making them more confident that they can retire when they really want to. It can also give organizations a stronger value proposition in the talent wars. Plan sponsors may have been hesitant to select an income/annuity provider, but the SECURE Act has gone a long distance toward paving the way.

Incorporating lifetime income in a QDIA also keeps participants’ assets in plans, which could give plans more muscle when negotiating with providers for better value. Participants also benefit from an institutionally managed solution, with its expert analysis and oversight. If that QDIA can be personalized to individuals’ needs, it can overcome a common objection that solutions are “one size fits all.”

Embedding a secure lifetime income solution with an insurance option in a QDIA will likely reach more participants than simply adding a stand-alone menu option. It’s also easier now to add a secure-income component to an existing target-date solution, giving participants a missing feature without disrupting anything else that’s working. Ultimately, a lifetime-income QDIA would enable a seamless continuation of the automatic, “do-it-for-me” structure that has helped participants so much in their working years.

For DC plan sponsors interested in pursuing such a solution, the next step is to determine which type is the best fit for their plan’s participants.

“Target date” in a fund’s name refers to the approximate year when a plan participant expects to retire and begin withdrawing from his or her account. Target-date funds gradually adjust their asset allocation, lowering risk as a participant nears retirement. Investments in target-date funds are not guaranteed against loss of principal at any time, and account values can be more or less than the original amount invested—including at the time of the fund’s target date. Also, investing in target-date funds does not guarantee sufficient income in retirement.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© AllianceBernstein

Read more commentaries by AllianceBernstein