Ten years ago, income investing was next to impossible.

Money markets paid nothing. The dividend yield for the S&P 500 Index was 2%, and the 10-Year Treasury yield was stuck between 2%-3%. Retirees who had spent a lifetime accumulating a nest egg of a few million dollars with the expectation of living on the income would say to their financial advisors, “Just give me 5%, that’s what I need to live on.”

But any honest advisor had to explain that the only way to 5% was by sacrificing liquidity, using leverage, or reaching for yield in lower-quality fixed income. For many, accepting the increased risk of a higher allocation to equities was the answer to earning 5% returns, but it came with more restless nights when volatility inevitably struck stocks.

Fortunately, the era of no income is over, and I am hopeful it will stay that way. Today, money markets yield over 5% and the 10-Year Treasury yield is 4.3% after peaking near 5% in October.

Each Monday our fixed-income team reviews the landscape of the fixed-income markets, and we see 5%+ yields across the credit spectrum. Government-backed mortgages yield 5.5%, Investment Grade Corporate bonds yield close to 6%, High Yield corporate bonds and Emerging Market bonds yield over 8%, and floating-rate bank loans yield over 9%.

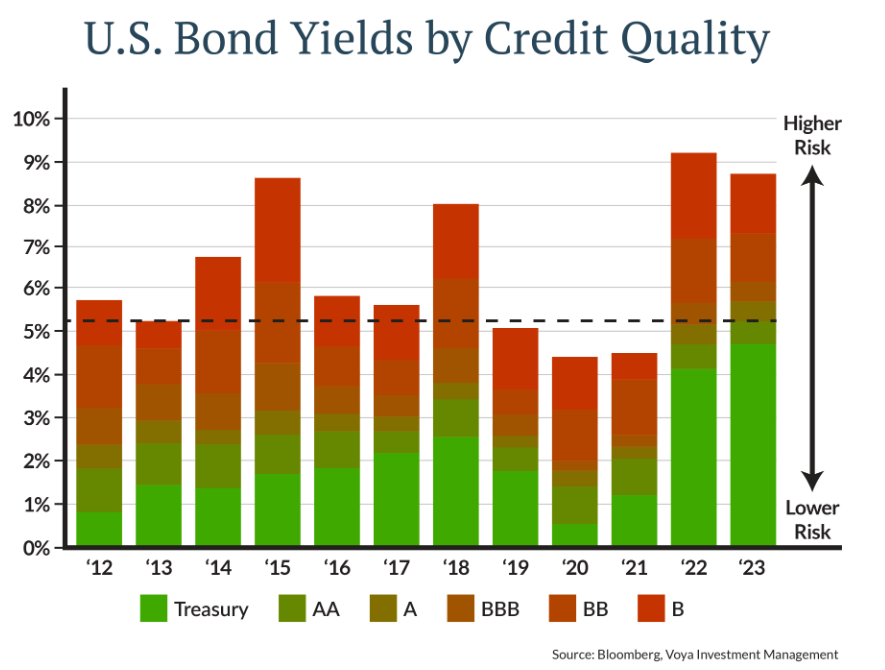

Voya Investment Management looked back at bond yields going back to 2012 and found that A-rated corporate bonds (think names like JPMorgan, IBM, Intel and Disney) today yield as much or more than junk bonds a decade ago [Figure 1]. No longer is it necessary to reach for yield to generate a solid stream of income from bonds.

Don’t Overlook Municipal Bonds

So far I have focused on the income opportunity in taxable bonds. But investors in high tax brackets should take a hard look at tax-exempt municipal bonds issued by state and local governments to fund things like the construction of highways, sewer systems and schools.

I first began trading municipal bonds in 2010. Back then, I would spend hours looking for muni odd lots (very small sizes of a much larger large bond issue) in the attempt to earn a few basis points (a basis point is 1/100 of 1%) in excess of the yield available on larger lots. I added value for my clients through painstaking research but still ended up buying bonds with yields that were usually below the rate of inflation.

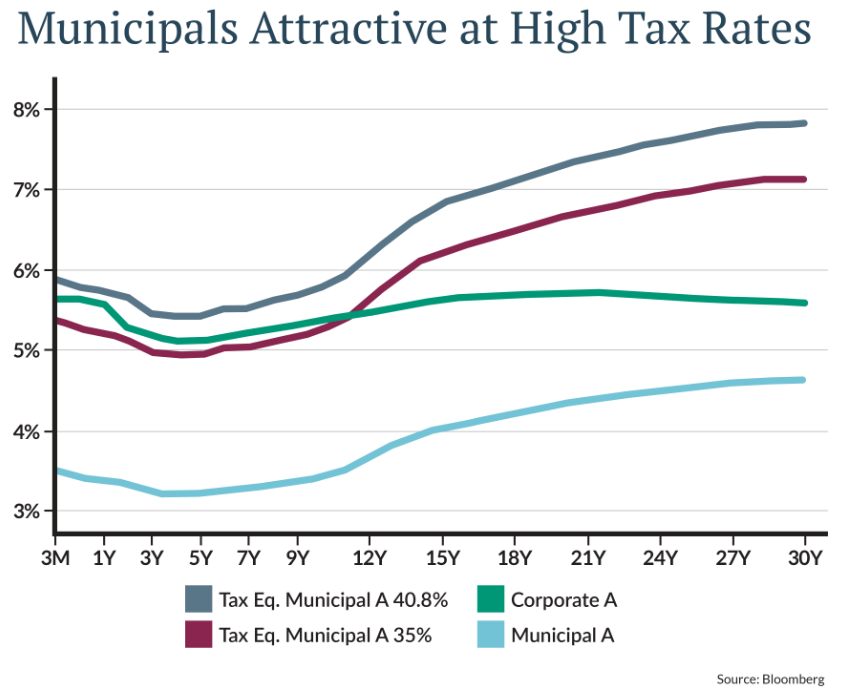

Today, we are consistently buying high-quality tax-exempt municipal bonds at nominal yields of 3%-5%. That translates into taxable equivalent yields of 5% to 8% for investors in the highest tax brackets [Figure 2].

The municipal yield curve is upward sloping, unlike the Treasury yield curve, making longer-term municipals look especially attractive. Taxable equivalent yields are between 6%-8%, well above similarly rated corporate bond yields, for investors willing to take on more interest-rate risk. High earners should consult with their advisor about whether it makes sense to extend the average maturities of bond portfolios.

Bonds vs. Stocks

Investors who made the choice years ago to maintain a higher allocation to equites to earn 5% have achieved their goals if they managed to stay steadfast during the harrowing drawdowns along the way. But such investors may wish to reconsider their overweight to equities considering the current opportunity in fixed income.

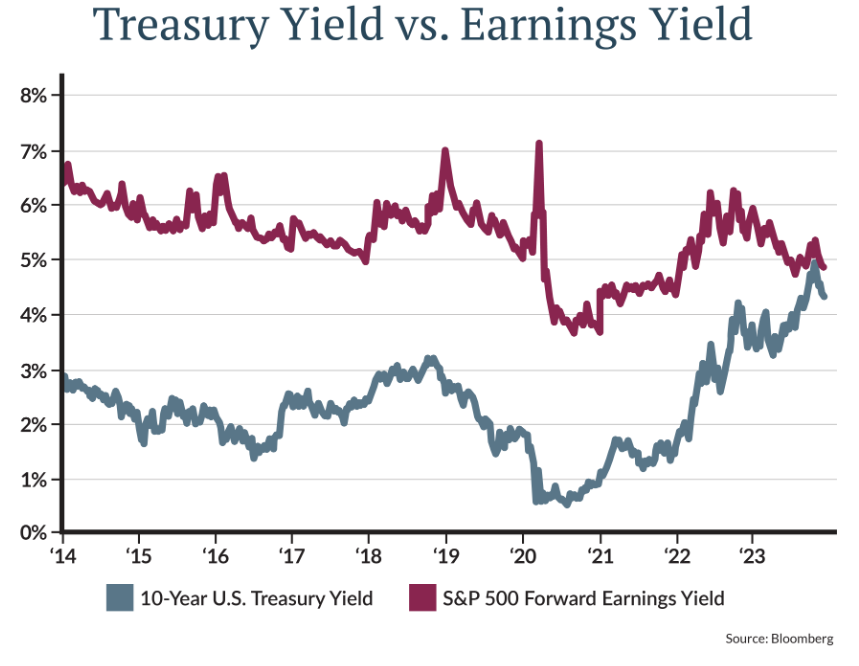

The S&P 500 Index dividend yield today is about 1.5%, even lower than it was a decade ago. Higher-than-average equity valuations are also reflected in the earnings yield (the inverse of the P/E ratio), which shows the percentage of a company's earnings per share. The forward earnings yield for the S&P 500 is about 4.9% today compared to the post-financial crisis average of 6%. Treasuries are more compelling relative to stocks than they have been in many years [Figure 3].

If we were to compare BBB corporate bond yields to the S&P 500 earnings yield, the chart above would be even more favorable to bonds, showing a yield advantage of about 0.75% in favor of corporate bonds. That is a reversal of the trend over the last quarter century when the S&P earnings yield typically exceeded BBB bond yields.

Is 5% Enough?

Today, advisors can look their income-oriented clients straight in the eye and talk about a number of ways to reach 5%. Clients need not reach for yield in lower quality areas of fixed income or assume the added volatility of overweighting equities. High-quality corporate and municipal bonds can do the heavy lifting in income-oriented portfolios for the first time in 15 years.

A better question to ask these days is whether 5% is enough. And that question should be answered through the creation of a comprehensive financial plan with your JFG advisor. Income generation is just one piece of the puzzle, but one that is a lot more important and enticing than is has been in some time.

This information is for educational and illustrative purposes only and should not be used or construed as financial advice, an offer to sell, a solicitation, an offer to buy or a recommendation for any security. Opinions expressed herein are as of the date of this report and do not necessarily represent the views of Johnson Financial Group and/or its affiliates. Johnson Financial Group and/or its affiliates may issue reports or have opinions that are inconsistent with this report. Johnson Financial Group and/or its affiliates do not warrant the accuracy or completeness of information contained herein. Such information is subject to change without notice and is not intended to influence your investment decisions. Johnson Financial Group and/or its affiliates do not provide legal or tax advice to clients. You should review your particular circumstances with your independent legal and tax advisors. Whether any planned tax result is realized by you depends on the specific facts of your own situation at the time your taxes are prepared. Past performance is no guarantee of future results. All performance data, while deemed obtained from reliable sources, are not guaranteed for accuracy. Not for use as a primary basis of investment decisions. Not to be construed to meet the needs of any particular investor. Asset allocation and diversification do not assure or guarantee better performance and cannot eliminate the risk of investment losses. Certain investments, like real estate, equity investments and fixed income securities, carry a certain degree of risk and may not be suitable for all investors. An investor could lose all or a substantial amount of his or her investment. Johnson Financial Group is the parent company of Johnson Bank and Johnson Wealth Inc. NOT FDIC INSURED * NO BANK GUARANTEE * MAY LOSE VALUE

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Johnson Financial Group

Read more commentaries by Johnson Financial Group