Equities have an important role to play in a diversified allocation today, to help hedge against inflation and to navigate a lower-growth environment.

Higher bond yields are presenting tough questions for equity investors. While the risk/reward trade-off for equities might be less favorable than in the past, historical return patterns suggest that US stocks can still do well in this environment.

Making investment decisions about any asset is a function of risk versus reward. For investors in stocks, the equity risk premium (ERP) is a common way to measure the risk/reward trade-off. Simply put, the ERP is the excess return that investors expect to earn over a risk-free rate. It measures the compensation that investors expect for investments in stocks, which are generally seen as riskier assets than bonds or cash. A higher ERP signals that investors can expect a relatively greater reward from stocks than they would in a lower-ERP environment, and vice versa.

Is Today’s Lower ERP a Bad Signal for Stocks?

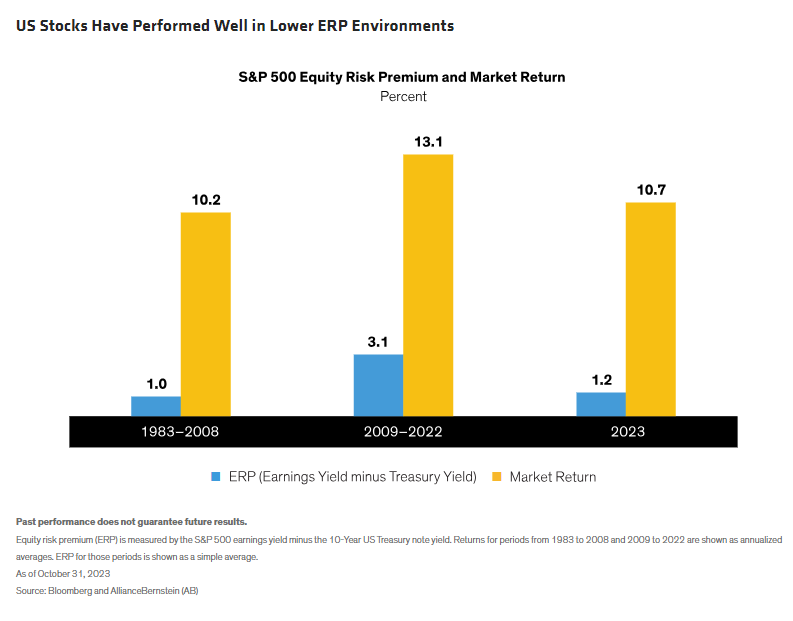

This year, the ERP for US stocks has declined. Our ERP metric shows the earnings yield of the S&P 500 minus the yield of the 10-Year US Treasury note, a proxy for the risk-free rate. That spread declined to 1.2 percentage points at the end of October, from an average of 3.1 percentage points between 2009 and 2022 (Display). The ERP has narrowed because rising interest rates lifted the Treasury yield from near-zero levels to 4.9% at the end of October.

To equity investors, that sounds worrying. After all, the ERP is likely to be lower in the coming years, as bond yields won’t be suppressed by low inflation, ultralow interest rates and the Federal Reserve’s quantitative easing programs that prevailed from the global financial crisis through the COVID-19 pandemic. From 2009 to 2022, when the ERP was much higher, US stocks returned 13.1% annualized on average. So does that mean the lower ERP is a warning sign for equity investors?

Not necessarily. We’ve experienced periods of lower ERPs in the past, and stocks have done relatively well. For example, from 1983 through 2008, the ERP was also low at 1.0%. Yet during that period, the S&P 500 returned an annualized average of 10.2%. Future conditions may well be different than in the past, and the lower ERP does set the bar higher for equities. Still, history suggests that stocks can still deliver solid returns in higher-bond-yield environments.

Equities Can Help Portfolios Cope with Inflation

Yes, we understand that bond yields of close to 5% these days are an attractive proposition for investors and offer a sense of safety in an unstable world. Yet we believe stocks and bonds both have important roles to play in a diversified investment portfolio today.

In particular, we think stocks offer a good hedge against inflation. Our research suggests that in periods of moderate annual inflation of between 2% and 4% between 1948 and the third quarter of 2023, the S&P 500 returned 2.5% per quarter. That’s a solid real return, which helps protect the purchasing power of portfolios if inflation stays relatively high, as we expect.

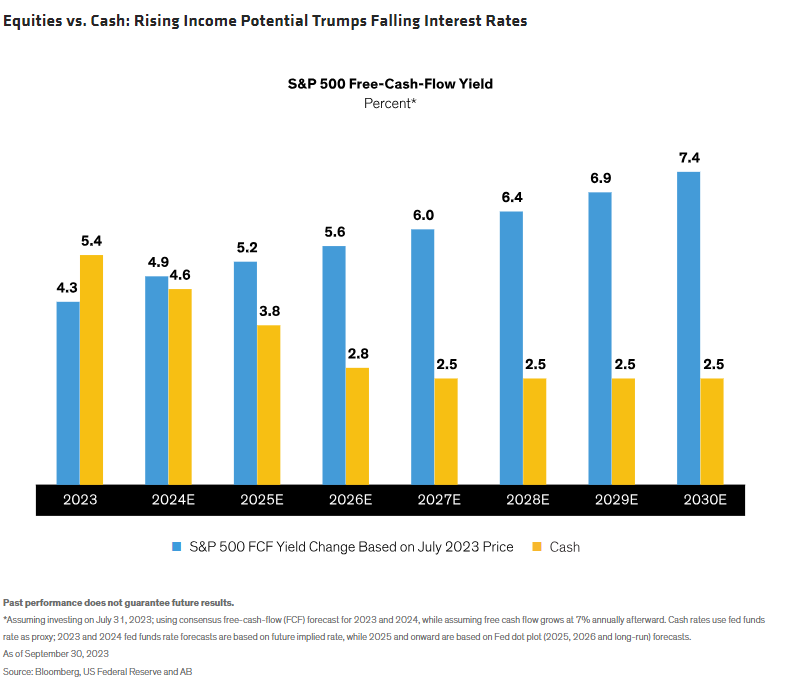

Equities can also offer a rising stream of income via increasing dividends. We measure equity income by using the free-cash-flow (FCF) yield, which calculates the excess cash that a business generates after deducting all operating costs. Our research suggests that the FCF yield of US stocks should rise over time, above the Fed’s long-term inflation target of 2%.

This contrasts markedly with a popular investment strategy these days—cash. Interest rates on cash are very attractive now, but they may not be for long if the Fed cuts rates, as many investors expect (Display). If yields do decline, investors who stay too long in cash would miss out on the potential for increasing dividends and the prospect of share-price appreciation along the way.

Selectivity Is Crucial When the Hurdles Are Higher

Bonds and stocks can and should coexist in a diversified investment allocation. In fact, if rates continue to fall over time, the ERP would rise, providing another impetus for equity returns.

For now, equity investors must be particularly selective to navigate a low-ERP environment. It’s especially important to identify quality companies with strong balance sheets that benefit from sources of consistent growth potential and cash-flow generation, and with share prices that trade at reasonable valuations. When carefully curated in an active equity portfolio, companies like these can help provide equity investors with both resilience and the ability to deliver return potential in a world of higher macroeconomic and market hurdles.

Grant Banko, Equities Product Manager, contributed to this analysis.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© AllianceBernstein

Read more commentaries by AllianceBernstein