U.S. Outlook: One Thing Leads to Another

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsEconomic pain is likely in 2024, but that doesn’t mean stocks will struggle all year, especially if there is a continuation of the rolling recessions that have hit the economy.

"Don't fight the Fed" is a decades-old mantra. "Higher for longer" is a newer reference to Federal Reserve policy amid what has been the most aggressive monetary policy tightening cycle in more than 40 years. As we approach 2024, there has been no diminution in the recession vs. soft landing debates thanks to a cycle filled with cross-currents in terms of economic data and inflation. A key characteristic of 2023—one we feel will persist into 2024—is the inverse relationship between Treasury bond yields and stock prices.

The only full-blown correction (defined as a drop of at least 10%) in U.S. stocks so far in 2023 from late July to late October directly corresponded to the spike in the 10-year Treasury yield from below 4% to 5%. The ensuing recovery since then has some roots in the decline in yields; with the 10-year yield moving back down to below 4.5%, as of Friday's close. Looking at next year, we believe the best backdrop for the U.S. equity market would not necessarily be another significant plunge in yields—particularly if triggered by a significant weakening in economic growth—but instead less volatility/more stability in yields.

Rolling along

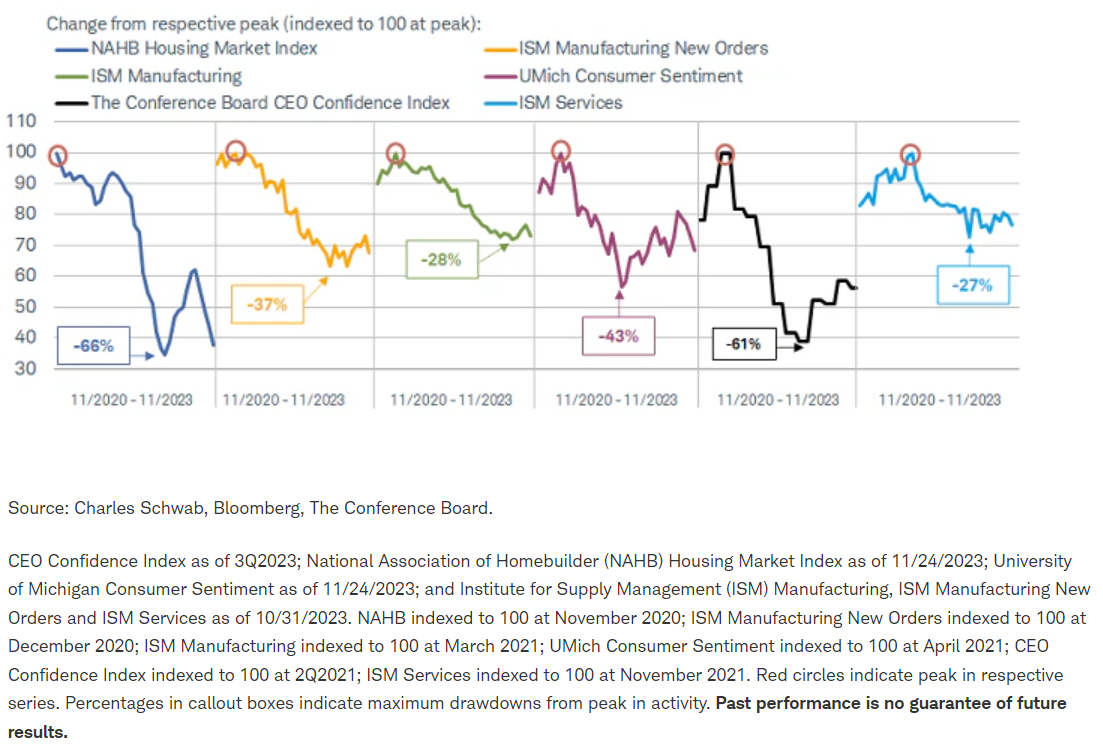

Amid the recession vs. soft landing debate, we continue to take a more nuanced approach given the unique nature of the pandemic cycle. We have used the term "rolling recessions" for some time given that several key segments of the U.S. economy, including housing, manufacturing, and many consumer-oriented segments of the economy have experienced recession-level weakness, as shown below.

A tale of rolling recessions

During the compression phase for the aforementioned segments of the economy, there was the offsetting strength in services—later to recover out of the lockdown phase of the pandemic. As services is a larger employer in the United States, that helps explain the resilience in the labor market. As you can see on the right in the graphic above, however, services have not been unscathed, with deterioration unfolding alongside more than a few cracks having formed in the labor market.

Looking ahead to 2024, we view the best-case scenario as a continued roll-through, with possible recession-level weakness in services being offset by stability and/or recovery in segments which have already taken their hits. However, we think recession risk in a traditional sense, via a formal declaration by the National Bureau of Economic Research (NBER)—the official recession arbiters since the late-1970s—is still a distinct possibility.

Long and variable lags

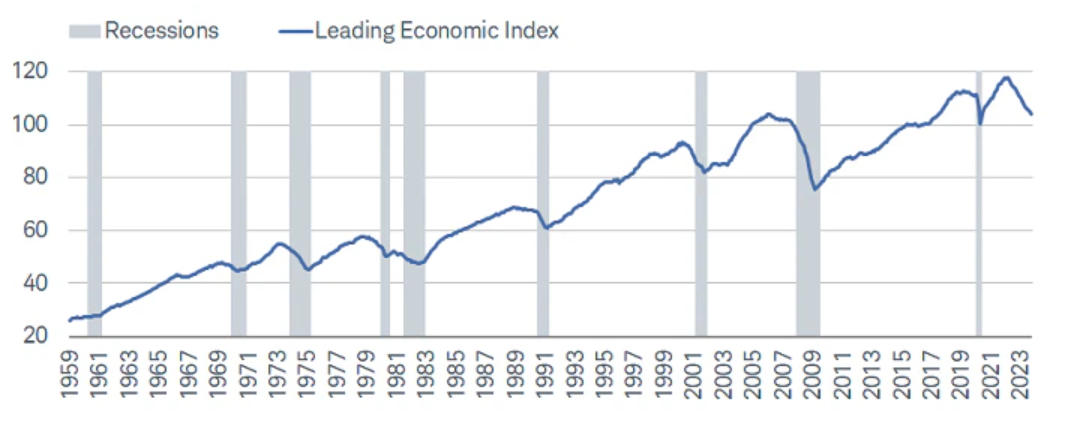

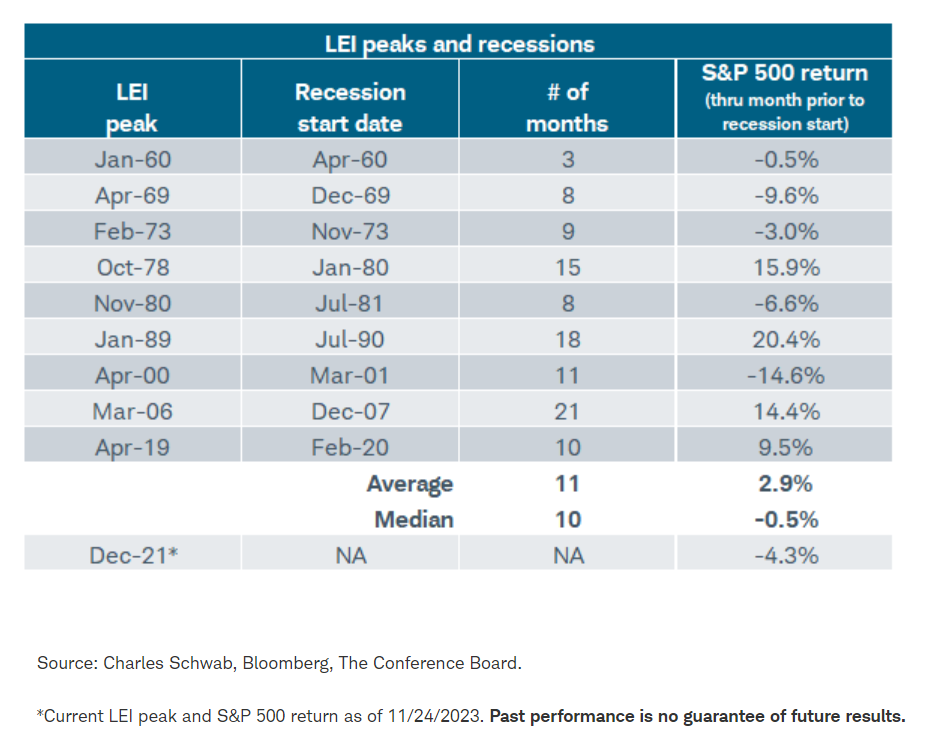

In his book, A Program for Monetary Stability, famed economist and Nobel laureate Milton Friedman wrote that "monetary changes have their effect only after a considerable lag and over a long period" and that the lag is "rather variable." Heading into 2024, the U.S. economy has not passed the expiration date associated with those variable lags, specifically as it relates to the timing of the decline in leading economic indicators and the inversion of the yield curve.

As shown below, the Leading Economic Index (LEI) from The Conference Board has been in a steady decline for 19 consecutive months and as of the end of October 2023, was down nearly 8% year-over-year. Per the recession bars in the chart, such steep declines have typically only occurred during recessions. As shown in the accompanying table below, the distance between LEI peaks and recession starts has averaged 11 months; but importantly, the range is quite wide: only three months of separation in 1960 and 21 months of separation in 2006-2007. Where you can also see a wide range is in the S&P 500® performance column above. This is a great example of the appropriate admonition about averages: analysis of an average leads to average analysis.

Leading indicators' plunge

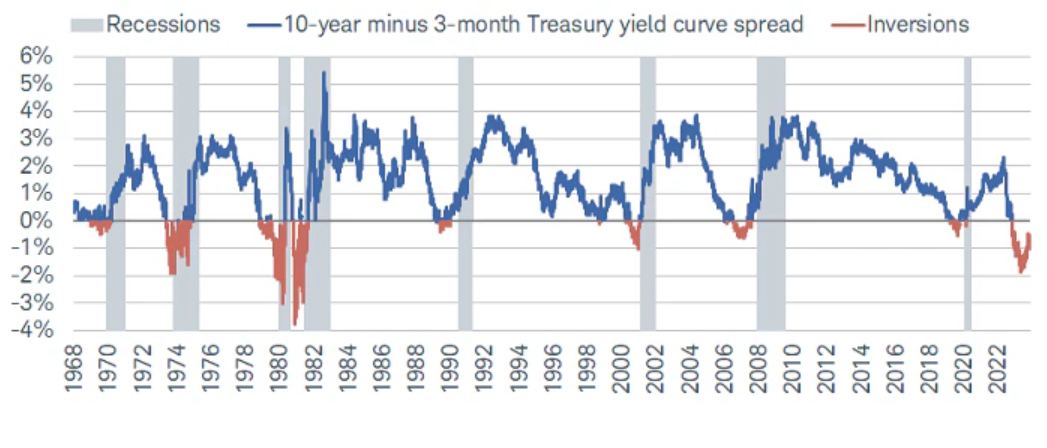

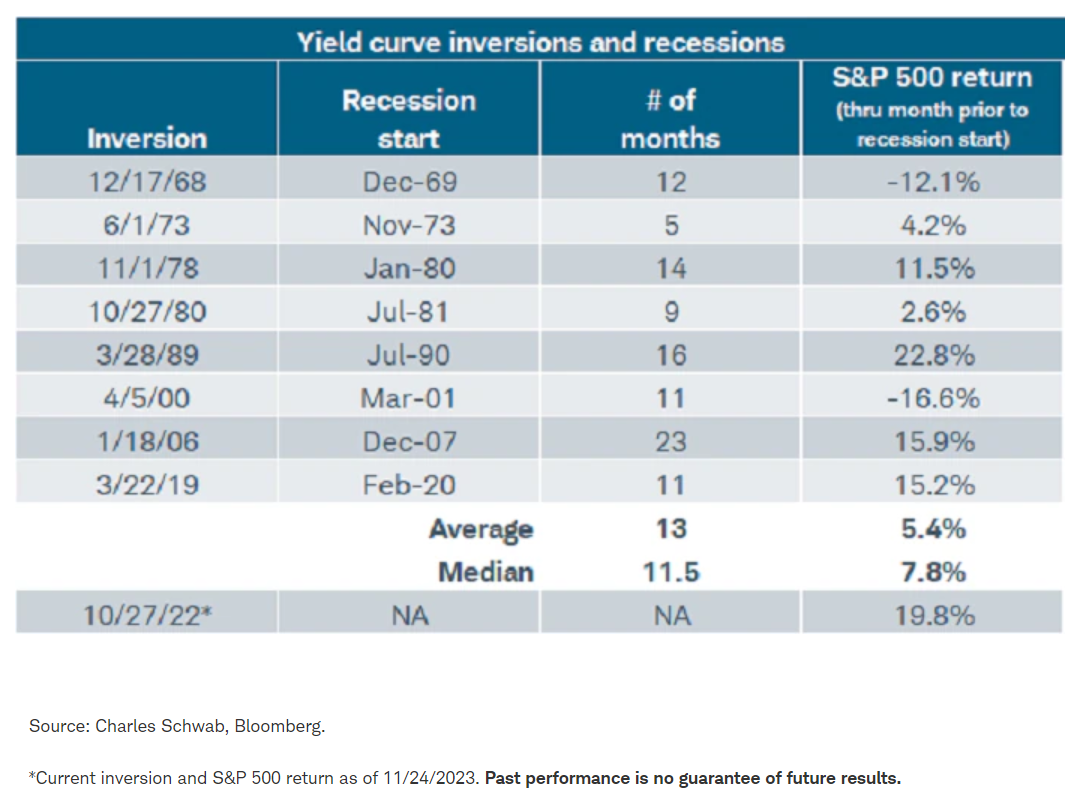

Though not quite the 19-month span of the LEI's decline, the U.S. yield curve has been inverted for more than a year. As shown in the chart below, with the exception of an extremely brief/mild inversion in 1998, inversions over the past six decades have had a perfect track record of signaling recessions to come. Like with the LEI, however, there is both a small sample size and wide range associated with yield curve inversions in terms of time span and equity market returns. As shown in the accompanying table, a recession came as quickly as five months post-inversion in 1973, while it was nearly two years following the inversion in early 2006 before the global financial crisis recession began. Also, like with the LEI, the S&P 500's return between inversions and recession starts had a very wide range historically. To repeat: analysis of an average leads to average analysis.

We've recently received a number of questions about whether the recent steepening of the yield curve means recession risk is waning. The reality is that steepenings are signals of easier monetary conditions ahead—typically in response to recession. To use a weather analogy, inversions tend to be the recession "watch" while steepenings tend to be the recession "warning."

Yield curve says recession

Consumer exhaustion?

With consumer spending accounting for about 70% of U.S. gross domestic product (GDP), it is key to whether a formal recession can be avoided. In a more esoteric sense, recessions reflect contagion and the denting of animal spirits, typically necessitating a catalyst—often in either the labor market or financial system. As such, in 2024, we will be looking for signs in leading labor market indicators like unemployment claims and/or in the credit markets.

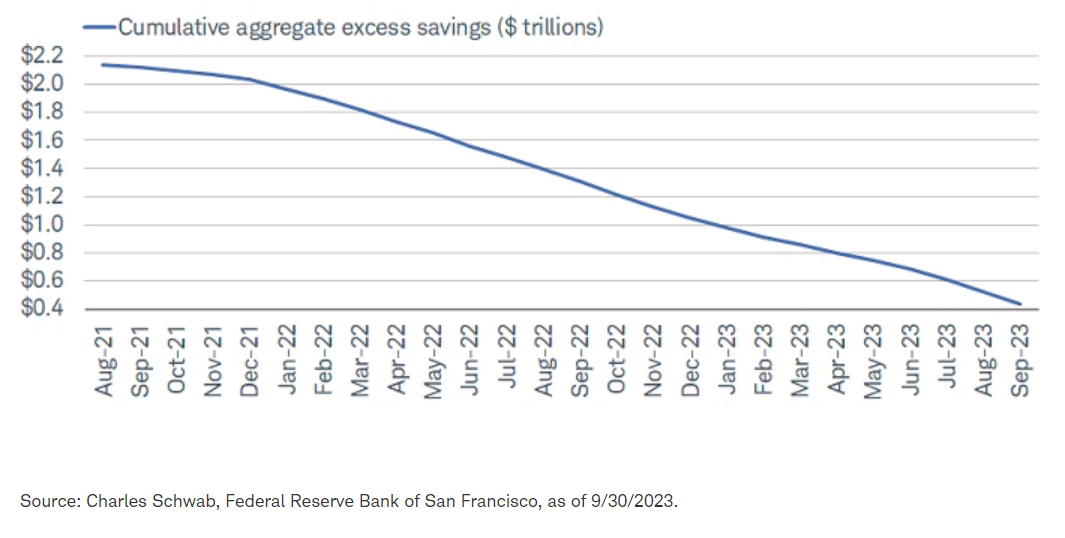

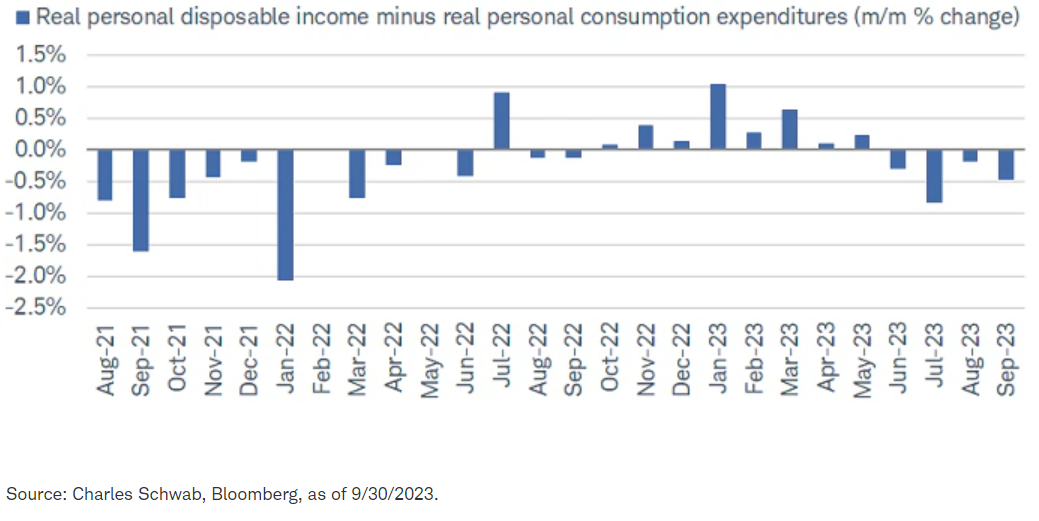

In this unique cycle, the strength in consumer spending had its roots in massive monetary and fiscal stimulus, which contributed to elevated "excess savings." But more recent resilience of consumer spending amid the decline in savings and a more challenging macro backdrop has largely been driven by confidence in the labor market.

As shown in the first chart below, there has been a complete rolling-over in excess savings. At the same time, per the second chart below, the spread between real disposable personal income and personal consumption expenditures has been negative (meaning spending is exceeding income) since last June.

Savings down/consumption up

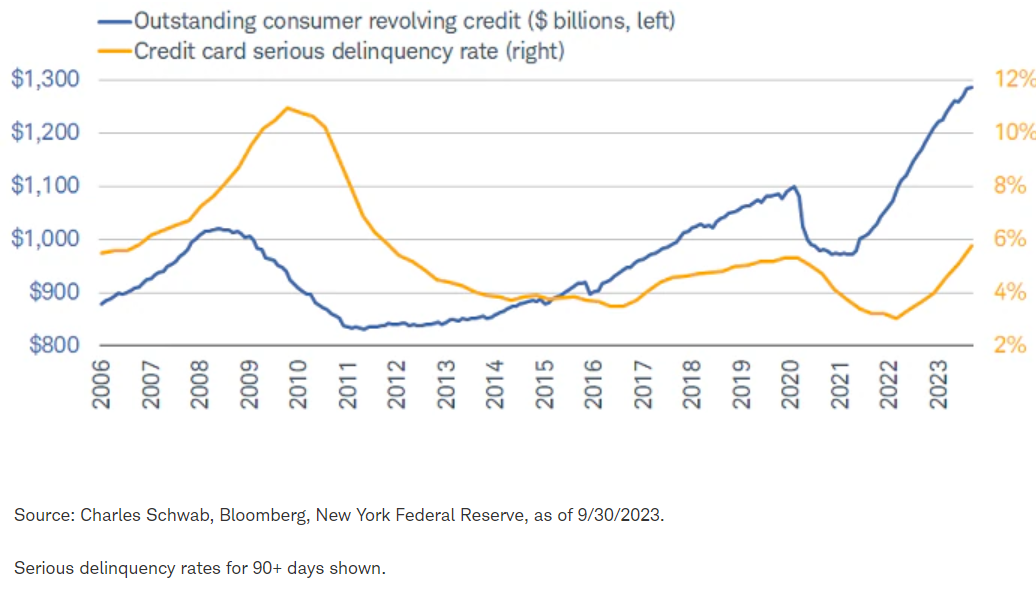

Non-mortgage interest payments by consumers are up more than 50% year-over-year, surpassing $1 trillion (annual rate) in the third quarter of 2023, per Bureau of Economic Analysis data. As shown below, the burgeoning "living beyond means" character of the consumer can most easily be seen when looking at consumers' revolving credit, shown in the blue line; and the associated increase in serious credit card delinquencies, shown in the yellow line. Those delinquencies are particularly acute among younger borrowers. For now, healthy wage growth has kept the ratio of credit card debt to compensation historically low; but further weakening of wage growth will cause the ratio to climb.

Charge it!

Delinquencies are rising elsewhere, too, including among auto loans. This is prompting banks to increase loan loss reserves, which will likely continue to weaken lending, consumer spending, and overall economic growth; at least until the Fed can take its foot off the economic brake.

Higher for longer?

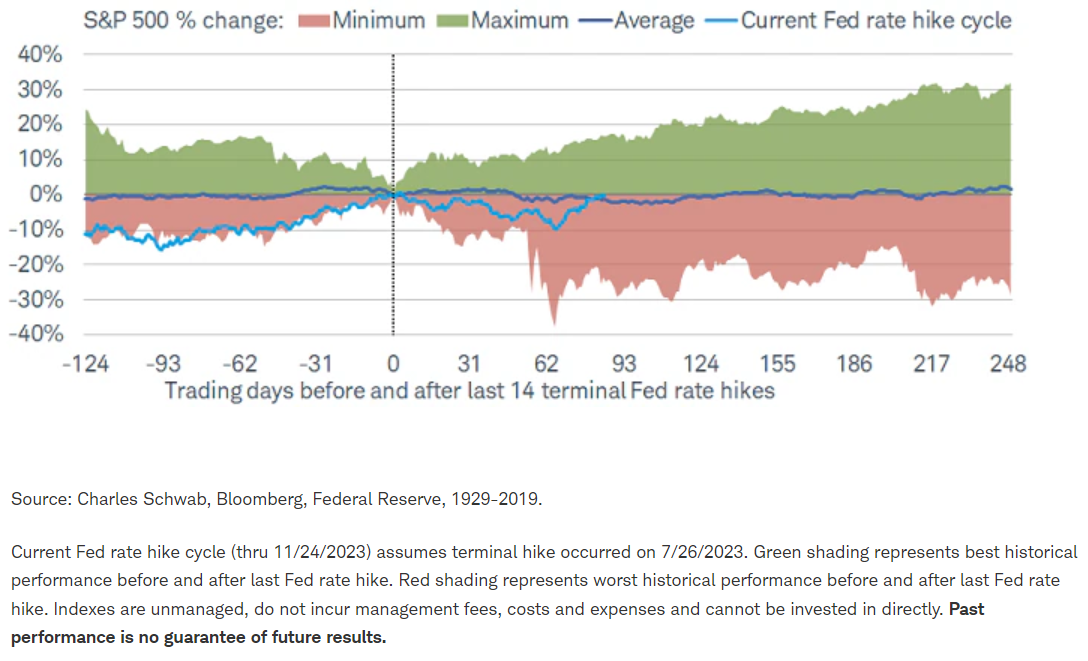

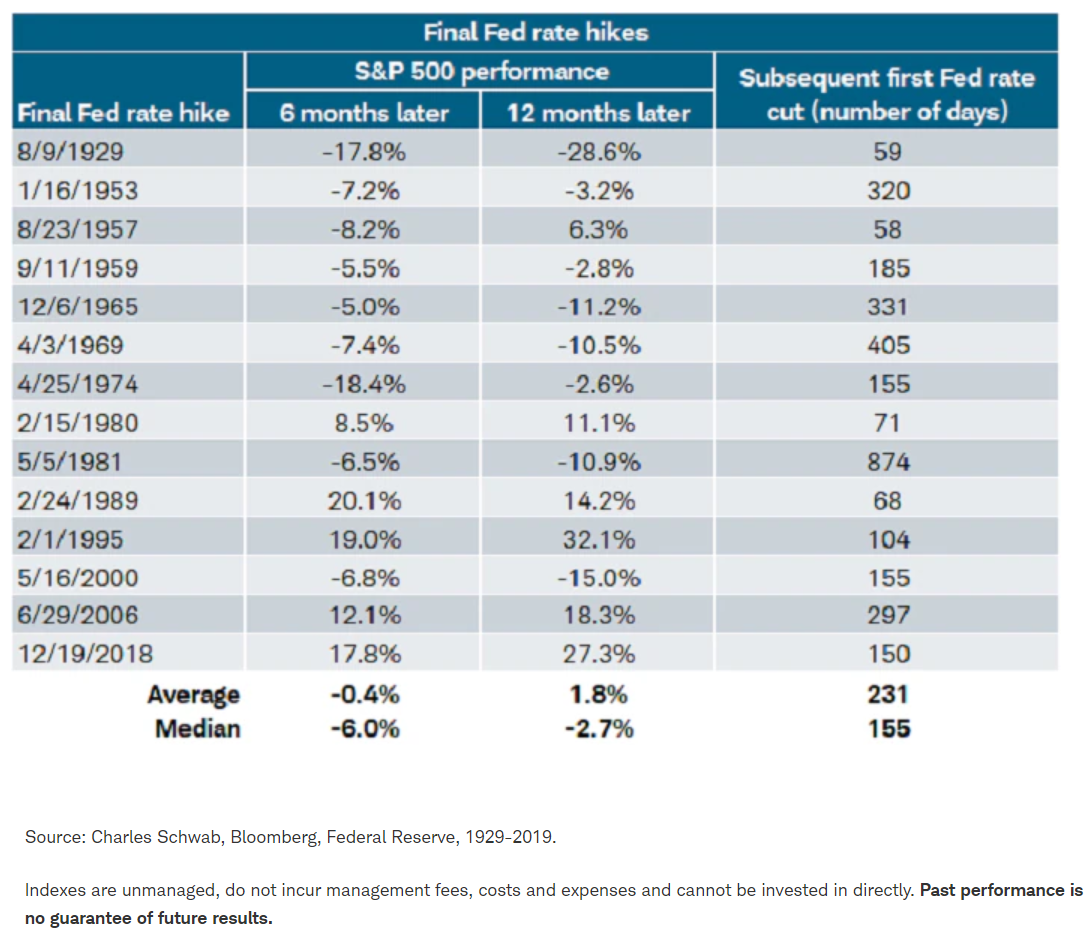

We believe inflation will continue to trend down heading into 2024—albeit not in a straight line. We also believe the July 2023 rate hike was the final hike in this tightening cycle. So, what might that mean for the economy and the stock market in 2024? It's easy to construct a chart showing the average performance of the stock market around final rate hikes throughout history. That's precisely what is shown with the dark blue line in the chart below.

Final rate hike: mixed picture

Importantly, however, the average belies the extreme range associated with historical outcomes. Yes, on average, the S&P 500 has been down slightly over the six months following the final rate hike, and up close to 2% over the 12 months following the final rate hike. But the ranges were -18% to +20% and -29% to +32%, respectively. Based on the small sample size and extremely wide ranges, it's disingenuous to cite averages or medians; when in fact, not a single occurrence in either the six-month or 12-month column resembles the average or median. To repeat: analysis of an average leads to average analysis.

As shown in the light blue line in the chart above, since the July Fed rate hike, the S&P 500 has tracked in the weaker part of the historic range; though with the latest rally, it's sitting closer to the average. It highlights that there are always myriad influences on market behavior—not just Fed policy.

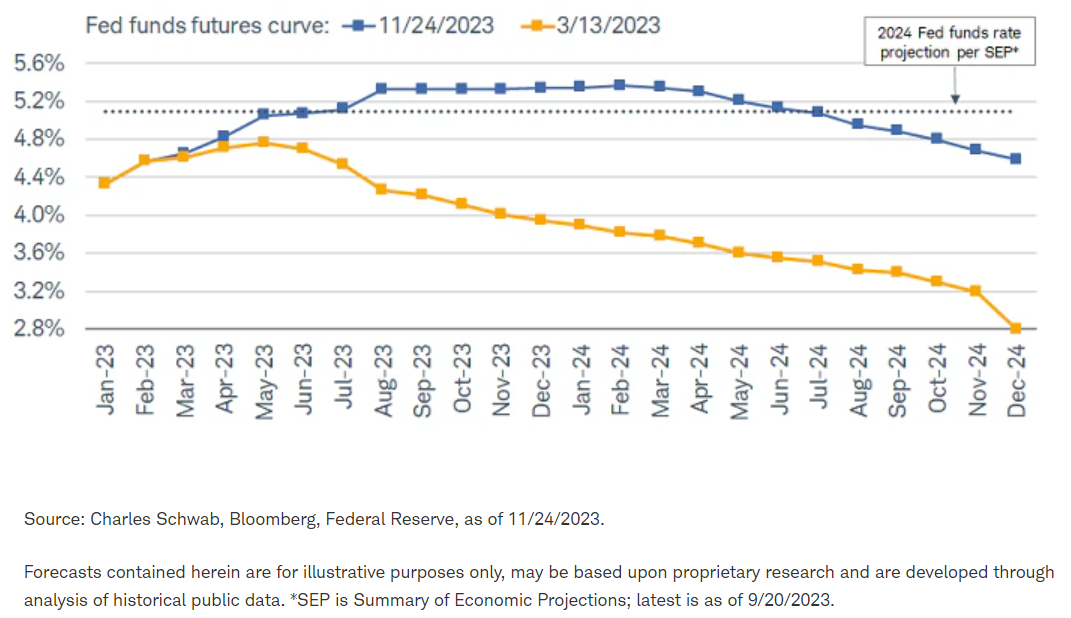

The table above also shows a very wide span (from 59 days to 874 days) in terms of the period between the Fed's final rate hike in a cycle and the subsequent initial rate cut. This brings up the expectation, based on the fed funds futures curve, shown below via the blue line, that rate cuts could begin by the mid-point of 2024.

Rate path a moving target

Perhaps because many Fed officials, including Fed Chair Jerome Powell, have been suggesting the Fed is not expecting to be cutting rates any time soon, the expectation around the start to an easing cycle will likely remain a moving target in 2024. We say "remain" because expectations were a moving target throughout 2023. As shown via the yellow line in the chart above, in the immediate aftermath of the mini banking crisis, the expectation was that the Fed would be cutting rates by the summer of 2023—obviously, quite a premature expectation.

Along the lines of the admonition "be careful what you wish for," it may be the case that if the Fed is cutting rates by mid-2024, it's because of further deterioration in the economy—specifically the labor market. In fact, one of our key expectations for the year to come is that the Fed will begin to shift its focus from the inflation side of its dual mandate to the employment side of its dual mandate.

Employing a changing backdrop

The unemployment rate has started to move higher, now approaching 4%, having troughed at 3.4% in early 2023. As shown in the blue line in the chart below, once the unemployment rate began to move higher in the past, the increase persisted. There is much less month-to-month volatility in the unemployment rate relative to employment metrics like payrolls. Also highlighted in the chart via recession bars is the lagging nature of the unemployment rate—not far off its trough heading into recession, and typically high and still rising heading out. It's why we regularly remind investors that a high unemployment rate doesn't bring on a recession; a recession ultimately causes the unemployment rate to jump. (The same works at the end of recessions, with the recovery beginning first, followed by an eventual move down in the unemployment rate.)

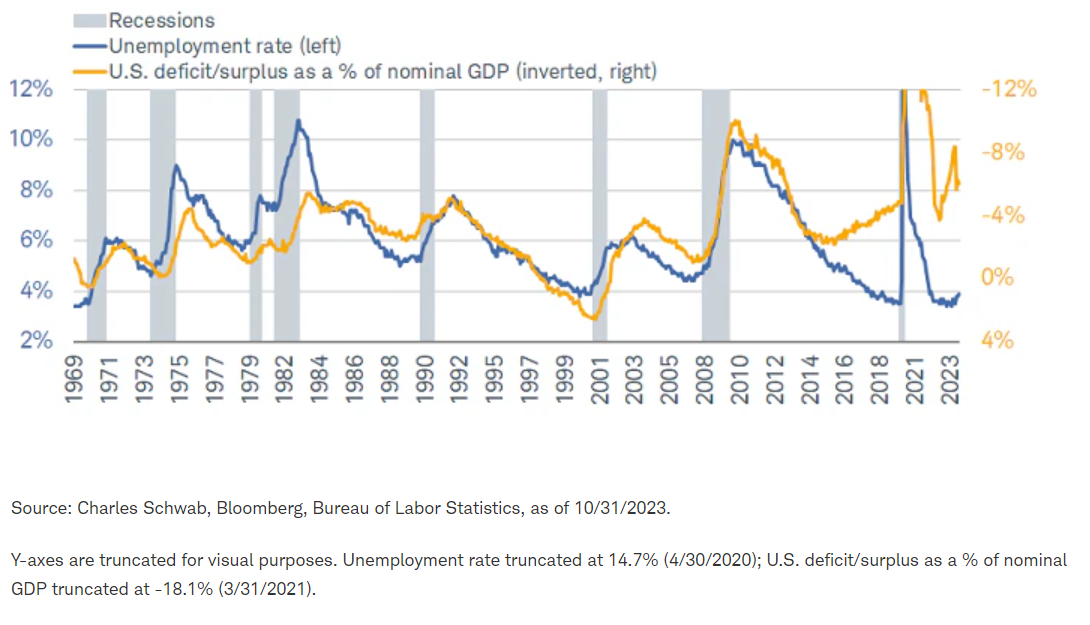

Unemployment/deficit both up

This is where we tie in the hot topic of the federal budget deficit and accompanying national debt, which has surged to more than $33 trillion. The United States has had a budget deficit every year for the past 22 years and a budget surplus in only five years over the past 50. This is not likely improving any time soon, with the Congressional Budget Office (CBO) projecting deficit to grow from nearly 6% now to 10% of GDP over the next 30 years.

As shown via the orange line (inverted) in the chart above, what's unique about this cycle's hefty deficit is that it's been accompanied by a still-low unemployment rate. As you can see historically, loftier budget deficits were typically accompanied by higher unemployment rates, as fiscal spending was combatting weak economic growth/recessions. Today, there is a yawning gap between the two, suggesting less flexibility in terms of fiscal firepower to combat a recession.

New era upon us?

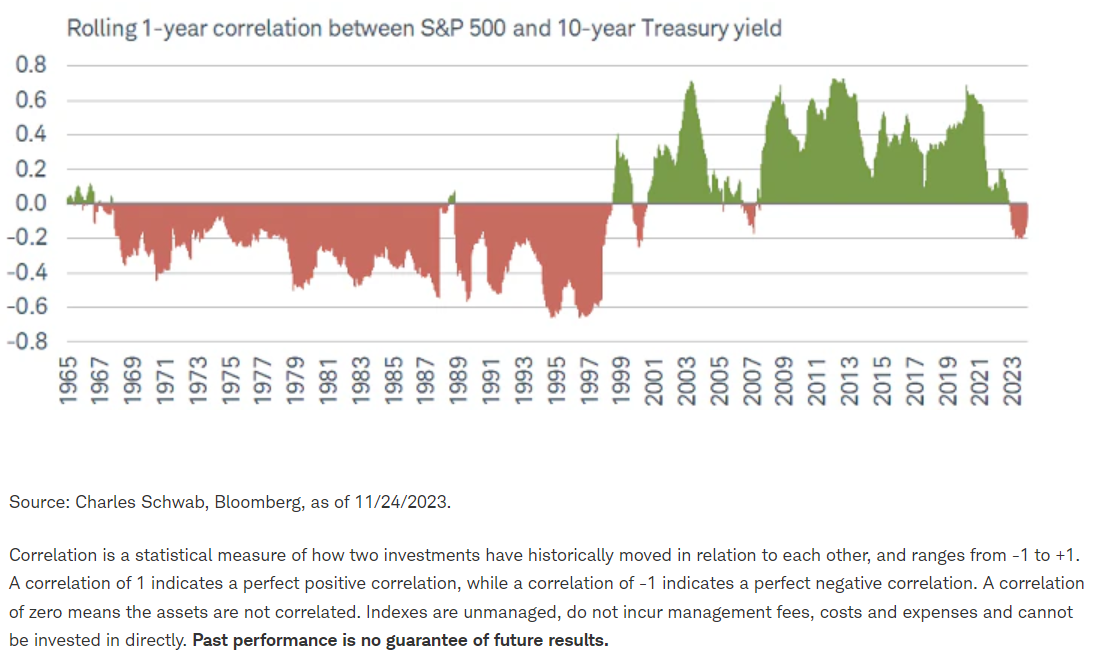

Let's transition to a more detailed look at the equity market outlook for 2024. We continue to believe that the correlation between bond yields and stock prices will remain negative. This has been a key part of our thesis that we have transitioned to a secular era which does not resemble the "Great Moderation" era from the late-1990s to the start of the pandemic (Say Goodbye…to Great Moderation? | Charles Schwab).

As shown below, during nearly the entire span of the three-decade period preceding the Great Moderation era, bond yields and stock prices were inversely correlated, which reversed and remained mostly positive for more than two decades prior to the pandemic. This is not an unnavigable environment, it's just different from what many investors got used to during the Great Moderation.

What's old is new again

Rates of change

As noted, a key to our outlook on the stock market for 2024 is the interest rate environment. As implied by our cartoon at the beginning of this report—created by Schwab's exceptional resident cartoonist Charlos Gary—bond yields are likely going to be in the driver's seat when it comes to equities' direction and volatility.

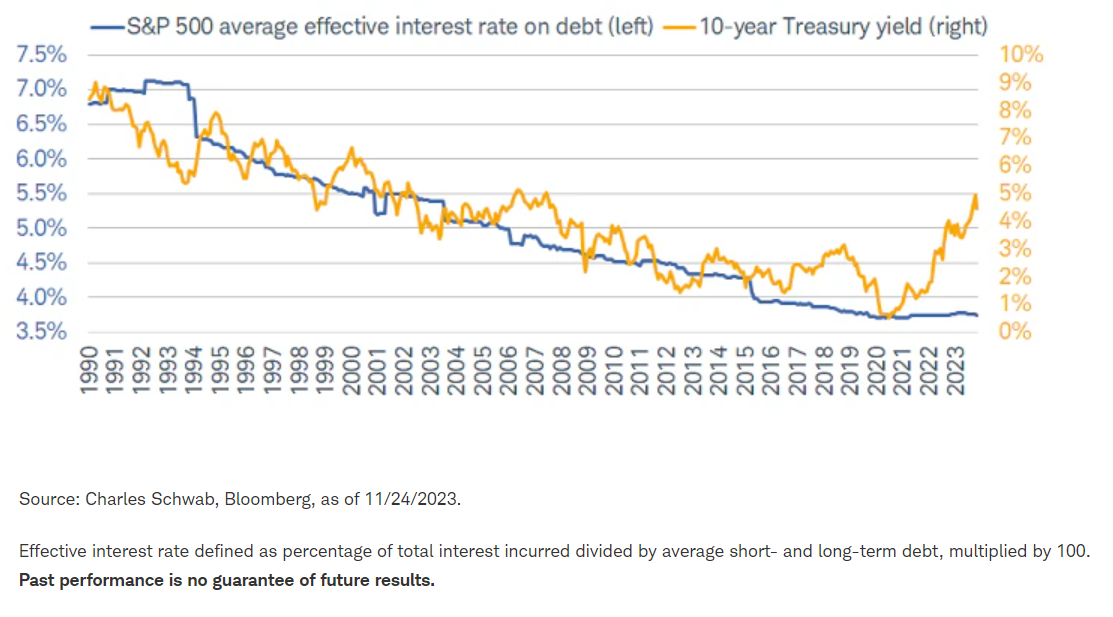

One way that might manifest is via higher debt servicing costs for companies in a higher-for-longer rate environment. Investors had enjoyed a secular decline in interest rates and bond yields leading up to the pandemic, which changed rather abruptly in 2022 when global central banks started aggressively hiking interest rates to combat inflation, leading to that year's bear market.

The low interest rate ship has sailed for now, which means the cost of capital has risen sharply. As shown in the chart below, that quick rise should start to take a toll on corporations when it comes to the interest owed on their debt (historically, there is about an 18-month lag between a move in Treasury rates and companies' effective interest rates)—especially those that either didn't term out their debt when rates were low or have debt coming due in the next year. Importantly, it's likely more of a simmering problem over time vs. the bottom falling out all at once.

Rate tide has turned

Higher rates are not only important for debt, but also for market multiples, like traditional price/earnings (P/E) ratios. As we pointed out in our outlook for 2023, periods of higher inflation and interest rates tend to coincide with lower P/Es. Thankfully, inflation pressures have continued to ease; but inflation volatility and a higher-for-longer interest rate environment would suggest earnings growth has to start to do more heavy lifting in 2024.

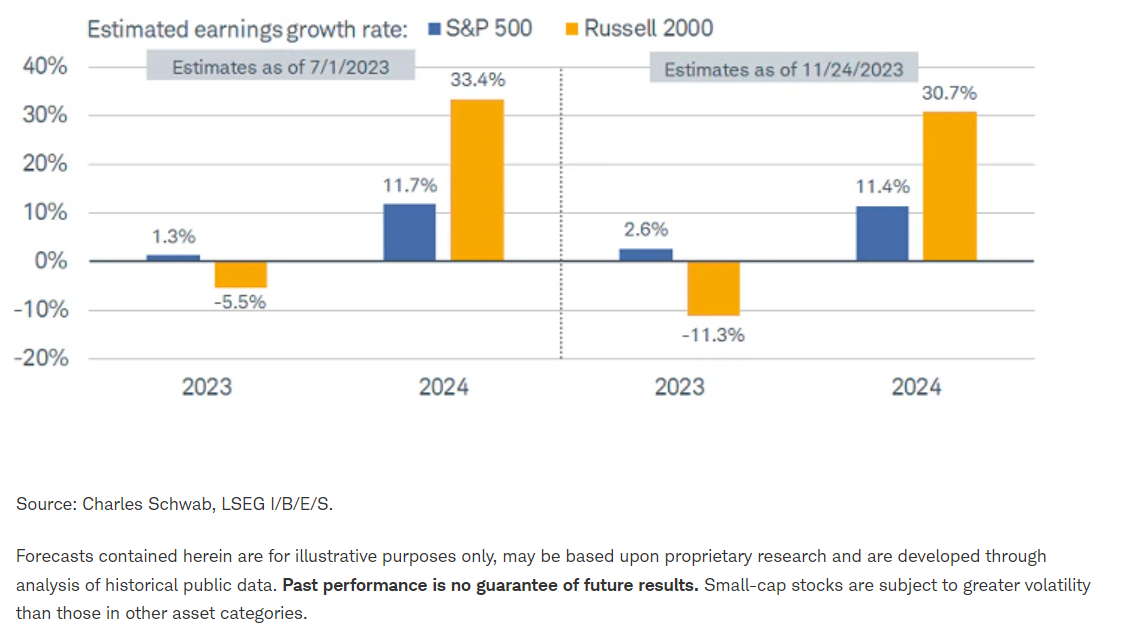

That expectation would be satisfied in 2024 if the consensus is correct in expecting double-digit earnings growth for both the S&P 500 and Russell 2000—a significant improvement relative to 2023. We have some skepticism about the lofty expectations; and indeed, excitement waned a bit as third quarter 2023 earnings season came to a close. As shown in the chart below, 2024 estimates been lowered; but an actual economic contraction would mean estimates are still too high.

That said, the hefty "swing factor" for small caps may be enticing for investors looking for opportunities down the capitalization spectrum. As LSEG I/B/E/S estimates show, the estimated earnings growth rate for the Russell 2000 is expected to improve from -11% in 2023 to +31% in 2024; one reason there may be attractive opportunities in the small-cap universe.

Small caps' "swing factor"

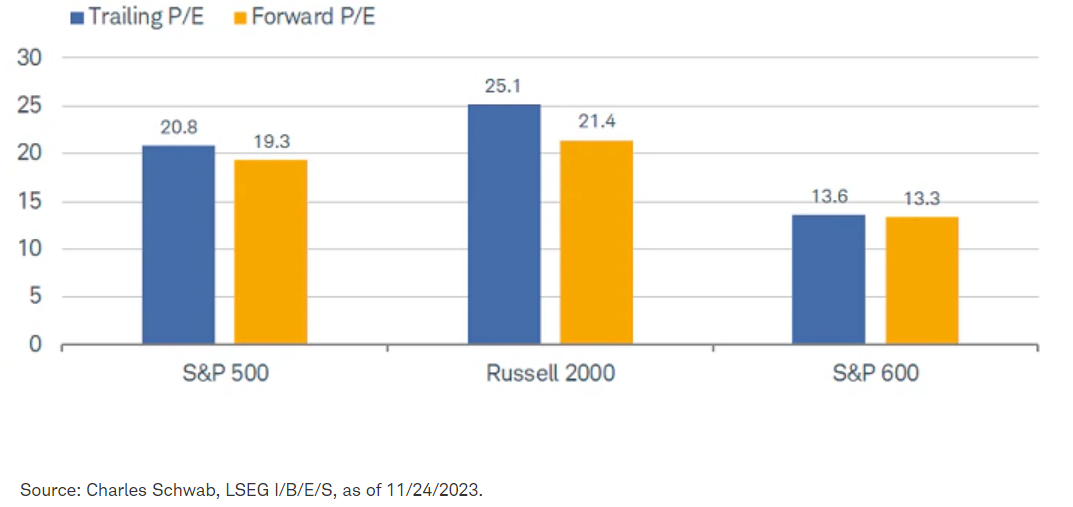

The stronger swing in small caps' earnings growth means forward P/Es look healthier, too, as shown in the chart below. While there will undoubtedly be revisions to estimates moving forward, taking them at current face value implies the market will look better from a valuation perspective next year.

Important caveat: there is a stark difference in multiples between the Russell 2000 and the S&P 600, which underscores our continued emphasis on quality. Unlike the Russell 2000, the S&P 600 is constructed with a profitability filter. For our stock pickers out there, the S&P 600 represents a higher-quality "source" of ideas in 2024.

Quality is cheaper

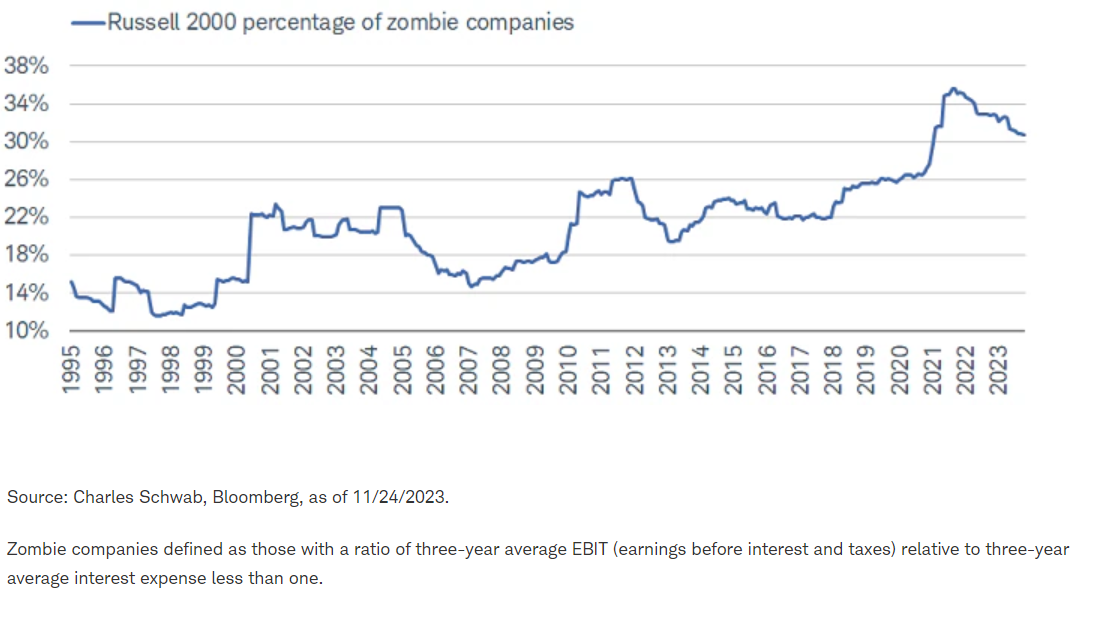

We have pounded the table on quality-oriented factors (characteristics) in 2023—especially when it comes to small caps. Within the Russell 2000, there is still a considerably large swath of "zombie" companies (those that don't earn enough to pay interest expense on their debt). As shown in the chart below, more than 30% of Russell 2000 members are zombie companies—down from the recent all-time high, but still quite elevated relative to history.

Zombies still walking

There are tailwinds for small caps in 2024, not least because a large chunk of the group already endured another bear market in 2023, making valuations relatively more attractive. However, we think the recovery could be choppy, especially in a more volatile interest rate and economic environment.

Small caps have historically outperformed when unemployment was high and the economy was transitioning out of recession ("early cycle"). Today, the unemployment rate is still quite low, and the economy is still showing signs of being "late cycle." For investors interested in small caps offering a value bias, we encourage heightened discipline and a factor focus around profitability, profit margin strength, and high interest coverage.

Mega caps giveth and taketh away

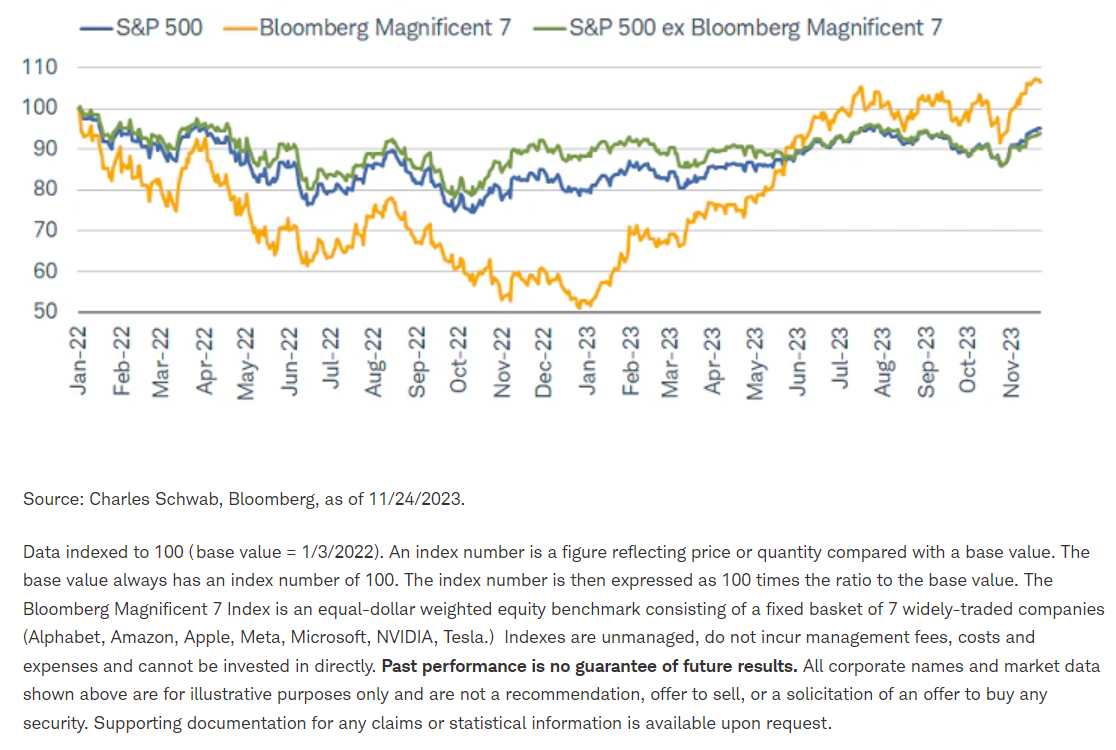

The dominant market theme in 2023—and likely heading into 2024—has been the supremacy of the "Magnificent 7" (Mag7) group of stocks, which pushed cap-weighted indexes like the S&P 500 higher during the year. Without the Mag7, the S&P 500's 2023 year-to-date gains are in the low single digits. In fact, as shown in the chart below, since the S&P 500's prior all-time high in early-January 2022, the Mag7 is up by more than 6%, but the "other 493" are actually down by nearly 6%.

Not always magnificent

Memories fade quickly, however. Had it not been for the Mag7's deep plunge in 2022, the market would have fared better in its bear market descent throughout that year. This underscores an important aspect of the mega-cap highfliers worth noting for the future: they are not immune to the business cycle and can also be a drag on cap-weighted indexes. That in turn underscores our emphasis on diversification when it comes to the mega caps and the rest of the market. It might sound odd when they're leading the charge, but it comes in handy when they're falling behind.

To be sure, the Mag7 scores quite well on a variety of quality metrics we favor—notably, high interest coverage and strong cash positions; supporting the notion that even in a weaker growth/higher rate environment, the Mag7 cohort can still do well. If we do see a harder landing, however—and if it occurs earlier in the year—there may be more potential upside in segments of the market that lagged in 2023; likely manifesting in the form of rotation out of the Mag7.

One theme we believe will shift from 2023 to 2024 is around artificial intelligence (AI). AI has both captured investors' hearts and minds, and contributed to the outperformance of both the Mag7 and technology stocks more broadly; but it's been in conjunction with narrow market performance. We believe a theme in 2024 will be less about AI's "creators" and more about AI's "adopters"—across the spectrum of industries and sectors—as companies increasingly focus their capital spending on productivity-enhancing investments.

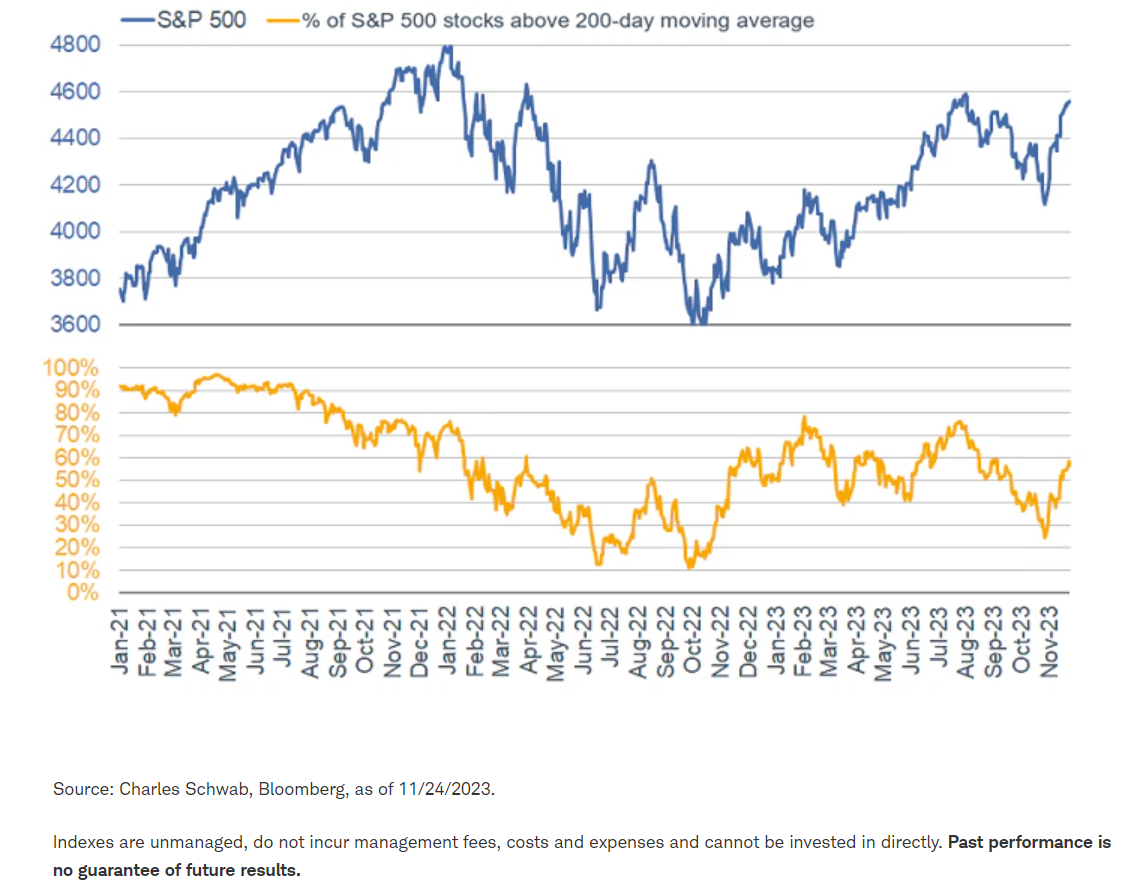

Waiting with bated breadth

A late-cycle-for-longer environment means that market breadth risk is key to watch heading into 2024. As cap-weighted indexes have climbed since late October, underlying breadth has continued to look weak—forming a similar setup to late-2021. As shown in the chart below, less than 60% of the S&P 500's members are trading above their 200-day moving averages; with breadth experiencing a series of lower highs and lower lows. Without a sustained improvement in breadth, we'd continue to raise the caution flag about the underlying health of the market.

Breadth not yet strong

Key to the shape of the market landscape in 2024 is how the economy reacts to the lagged effects of tighter monetary policy and more color on what we believe is a secular shift away from low interest rates. Our focus heading into 2024 remains on factors that do well alongside debt servicing costs growing in importance. Investors can screen for quality factors—like strong free cash flow, lots of cash on the balance sheet, high interest coverage, and healthy real revenue growth—across the spectrum of sectors, without having to make monolithic sector calls.

Memories

Notwithstanding our nuanced "rolling recessions" diagnosis, a formally declared recession is more likely than not in 2024 (its start point declared, as usual, long after the start). Frankly, in our view, a recession sooner-rather-than-later would be a better scenario for the economy, monetary policy, and the stock market. Based on history, the odds of the Fed perfectly "sticking the landing" are low. In this unique cycle, although the Fed may want to push against a recession, it is also sensitive to the risk of letting the inflation cat back out of the bag.

On that note, we're often asked what period in history does the current cycle most resemble. There are several facets of the late-1960s cycle that ring familiar. It's a comparison our friend Nancy Lazar, the chief economist of Piper Sandler Macro, believes rings familiar as well. Nancy was a recent guest on our new podcast—On Investing, hosted by me (Liz Ann) and Kathy Jones—and you can hear many of her thoughts here: This Week's CPI Data and the State of the Economy | Charles Schwab

In a nutshell, rate cuts by the Fed into late 1967 helped reaccelerate real GDP and push the unemployment rate down. But it also reignited inflation, forcing an aggressive tightening cycle which triggered the 1970 recession and sharply higher unemployment. The Fed then compounded the error by easing aggressively, even though core inflation remained elevated, setting off the 1970s' era of stagflation. We have no doubt this is a scenario Jerome Powell's Fed would like to avoid.

Best-case scenario for the economy in 2024 is for rolling recessions to morph into more durable rolling recoveries. Once the economic path is clearer, we expect less bifurcation within the market (i.e., less violent swings in leadership) as the year unfolds. That should bode well for groups that have failed to participate in the advance since the bear market low in October 2022.

Summing it up

The distinct characteristics of this economic and market cycle, and the Fed's reaction function to inflation and the labor market, have introduced greater uncertainty about a recession. One can still be avoided, either by a continuation of the "roll through" as we discussed and/or courtesy of better supply/demand fundamentals (e.g., a continued decline in energy prices). However, the ZIRP (zero interest rate policy) era is over; and while the bond market may have adjusted to this reality, the equity market may not have just yet. Active management is likely to have a better year in 2024.

Our outlook does provide some runway to the upside to equities, but possibly with the necessity of some economic pain nearer-term, in the interest of less-tight monetary policy. Heading into 2024, another short-term concern is around investor complacency, witnessed in attitudinal sentiment indicators showing elevated optimism amid extremely low volatility. As was the case in 2023, short-term market swings often move contrary to extremes of sentiment.

Specifically, for investors who have sector and asset classes exposures within portfolios that are now stretched both to the upside (e.g., Mag7) and downside (e.g., smaller cap stocks), periodic rebalancing is prudent in the interest of "adding low and trimming high" and staying in gear with the market's eventual mean reversions. We also (always) remind investors of the benefits of diversification—both within and across asset classes—especially if, as we expect, the investing backdrop will be characterized by wider global dispersion in term of both inflation and growth patterns.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk, including loss of principal. Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors. Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical information is available upon request.

Diversification and asset allocation strategies do not ensure a profit and cannot protect against losses in a declining market.

Rebalancing does not protect against losses or guarantee that an investor's goal will be met. Rebalancing may cause investors to incur transaction costs and, when a non-retirement account is rebalanced, taxable events may be created that may affect your tax liability.

Schwab does not recommend the use of technical analysis as a sole means of investment research.

Securities issued by small-cap companies may be riskier than those issued by larger companies, and their prices may move sharply, especially during market upturns and downturns.

Futures and futures options trading involves substantial risk and is not suitable for all investors. Please read the Risk Disclosure Statement for Futures and Options prior to trading futures products.

International investments involve additional risks, which include differences in financial accounting standards, currency fluctuations, geopolitical risk, foreign taxes and regulations, and the potential for illiquid markets. Investing in emerging markets may accentuate these risks.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively "Bloomberg"). Bloomberg or Bloomberg's licensors own all proprietary rights in the Bloomberg Indices. Neither Bloomberg nor Bloomberg's licensors approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits