A robust growth backdrop, a key input for cross-asset positioning, benefited from pent-up demand and an accommodative fiscal policy stance.

Multi-asset strategies harness return streams across diverse asset classes, including stocks, bonds, alternatives and options. Investor perception of growth prospects is one common thread in cross-asset performance, because it plays a strong role in driving risk appetite.

Looking back, 2023 stands out for growth that proved surprisingly resilient, given inflation headwinds and the tightest monetary policy in decades. Defying a widely expected recession, activity surprised to the upside. This was especially true in the US, where consensus expectations for real gross domestic product (GDP) now range from 2% to 2.5% growth, a modest acceleration from 2022 and slightly above the long-term average.

In fact, robust third-quarter growth rattled markets, as investor worries swung from a looming recession to an overheated economy and expectations shifted to higher-for-longer rates. Growth should decline toward—or somewhat below—long-term averages, enabling monetary policy to gradually normalize. This would support equity exposure and renewed diversification benefits from government bonds.

Strong Growth Benefited from Pent-Up Demand

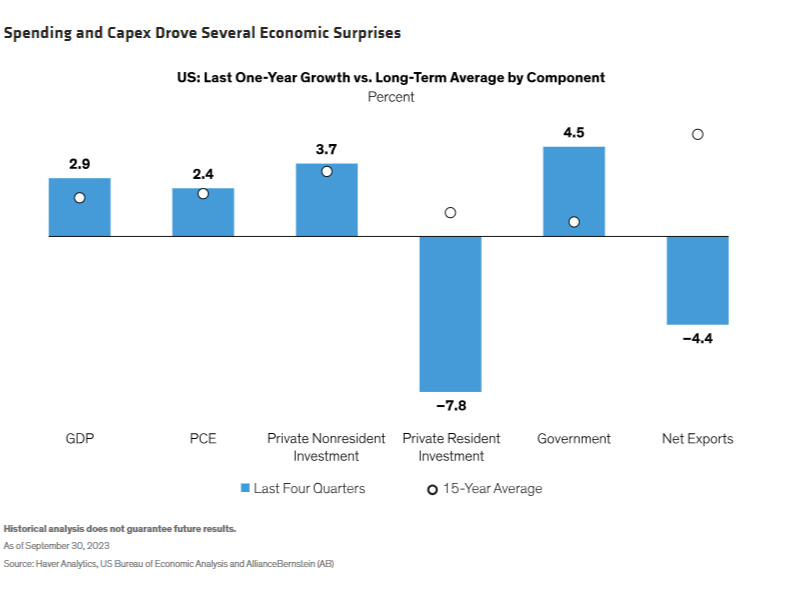

US GDP growth averaged 2.9% over the past 12 months, above its 1.9% long-term average (Display). Consumer spending and business investment were modestly above average, but government spending grew by 4.5%, well above its 0.7% average—a sizable boost to above-average GDP growth. We expect all three components to slow in coming months, as pent-up demand and one-off benefits diminish.

Thanks to a robust labor market and consumer willingness to spend on travel and other services, personal consumption expenditures grew by 2.4% over the last four quarters, slightly above the 15-year trend. We expect jobs growth to normalize as employment gaps close, and for the savings rate to gradually return to its pre-pandemic level, which should help cool consumer spending.

Business investment weathered the fastest rate-hike cycle in decades. A continued recovery from pandemic-era underinvestment helped, as did a modest boost from government incentives for investment under the CHIPS and Science Act (CHIPS Act) and Inflation Reduction Act (IRA). Business spending cooled in the third quarter, and we expect it to stay below trend for a few more quarters.

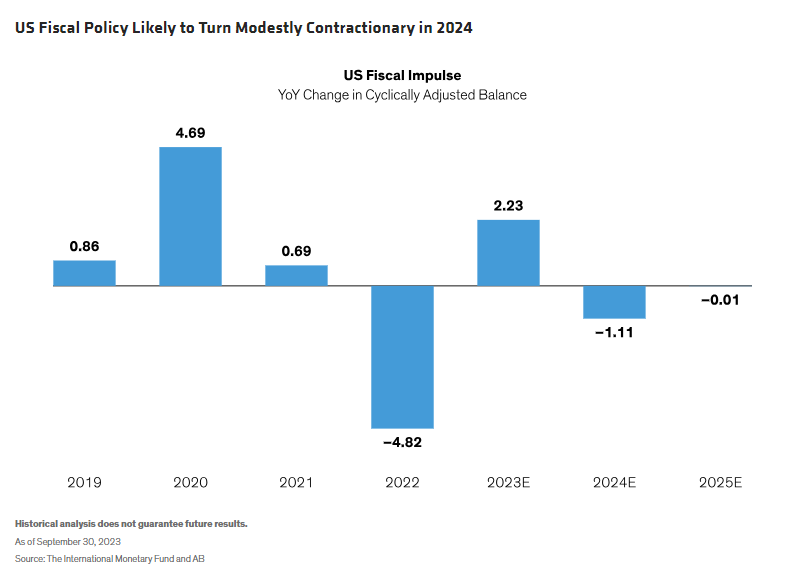

Meanwhile, a rebound in direct spending by federal and state governments bolstered government expenditures. As a result, the fiscal impulse—direct spending, transfers and tax credits such as those in the CHIPS and IRA measures—is now around 2.2% of 2023 GDP, above expectations from a year ago and a tailwind versus 2022. Next year’s fiscal policy is expected to be more modestly contractionary (Display), suggesting that this driver of above-average GDP growth is also likely to fade.

CHIPS and IRA Likely to Accelerate Change, Not Reflation

At times, the CHIPS Act and IRA are cited as potential long-term drivers of higher inflation, but we see their impact on the overall economy as small. Business investment’s recent resilience benefited from both secular and cyclical tailwinds; the secular tailwinds, but not the cyclical ones, seem likely to last.

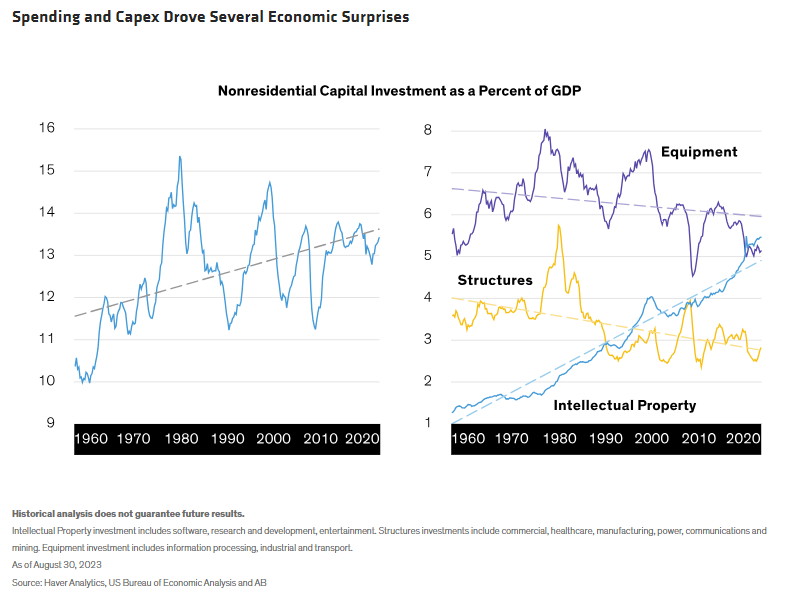

On a secular level, business investment has steadily become a larger share of the economy over the past 60 years, mainly because of robust growth in tech and R&D investment. Cyclical tailwinds, by contrast, have likely played out for the most part. After underinvestment during the pandemic, business investment has recovered to near its historical trend (Display, below left).

The CHIPS and IRA have changed the path of US domestic investment in semiconductors and renewables, respectively, with investment in manufacturing structures now 2.5 times pre-pandemic levels. But the impact on GDP growth over the past four quarters has been only 0.3% (Display, below right, yellow line). We expect the GDP impact to fade, but these sectors will see other important benefits.

Ongoing efforts to drive corporate efficiencies through automation and digitization have been bigger growth drivers, and we think this type of investment has room to run over the next few years, especially with AI’s rising influence across intellectual property (Display, below right, blue line).

CHIPS Act: A Boost for US-based Semiconductor Manufacturing

Since the CHIPS Act was passed in 2022, US$200 billion of new investment in US-based semiconductor manufacturing facilities has been announced. Many countries offer similar incentives, and the act’s main goal is to bring chip manufacturing capacity back to the US, so it isn’t expected to spur a big pickup in global semiconductor investment.

In fact, global capex plans for 2023 and 2024 are fairly subdued, but US investment could rise by about 60% from starting levels, assuming a five-year horizon for the announced projects. This will help US semiconductor manufacturing, although the initial GDP impact seems relatively small.

IRA: Lifting the Trajectory of Renewables

Since IRA’s enactment, nearly 300 announced initiatives have totaled over US$250 billion. Spanning solar, battery, storage, wind and hydrogen technologies, they should expand renewables output. Capacity additions of low-emitting technology through 2035 could reach 50 gigawatts per year versus the pre-IRA estimate of about 30 gigawatts, accelerating the achievement of US climate goals. Carbon emissions could shrink by 40% to 50% versus 2005—a major improvement over the pre-IRA estimates of 25% to 35%.

The yearly investment pace will likely vary, but the annual average is an estimated US$30–$55 billion, equivalent to a 0.1% to 0.2% GDP contribution the first year. It’s a meaningful advance for renewables, but much like CHIPS and semiconductors, isn’t likely to lead to persistent higher US growth and inflation.

Translating Macro Views into Asset Allocation

Fiscal policy, through direct government spending and tax incentives such as the CHIPS Act and IRA, has bolstered GDP growth, and they’re among many inputs that inform multi-asset allocations. Macro conditions and trends, as well as quantitative momentum and risk/return signals, for instance, are also in the mix.

We expect a gradual slowdown from above-expectations and above-trend growth. Meanwhile, inflation remains high but has continued to normalize. In this environment, we think it makes sense to have moderate exposure to risk assets, such as equities.

In addition to US stocks, we favor exposure to the UK, which currently offers compelling value. We’re cautious on emerging-market stocks, especially China, as policymakers seem to be prioritizing economic rebalancing over growth at all costs. Overall, we prefer a growth style tilt emphasizing quality fundamentals, such as strong balance sheets, positive earnings and attractive valuations.

Inflation has eased recently, but central banks will likely keep rates higher for longer. With the highest yields in 15 years, bonds offer attractive income potential and, in our view, renewed potential for diversifying equities. We favor US sovereigns, since policy tightening has been more extreme.

A global recession will likely wait for now, but unknown unknowns warrant caution. Multi-asset investors should allocate around the notion of economic resilience and a slow, steady normalization—not persistent reflation. As always, staying flexible and selective can help navigate a dynamic landscape.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to revision over time.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© AllianceBernstein

Read more commentaries by AllianceBernstein