A Time of Gratitude and Opportunity

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe run-off election looks tight in Argentina, where I’m attending a Young Presidents’ Organization (YPO) event in Buenos Aires. The two candidates, Economy Minister Sergio Massa and libertarian outsider Javier Milei, are polling relatively close, with Milei enjoying a slight advantage.

It’s an understatement to say that Argentine voters are not happy with the state of the economy. The number one issue on people’s minds right now is out-of-control consumer prices, which rose at an annual rate of 142.7% in October, if you can believe it.

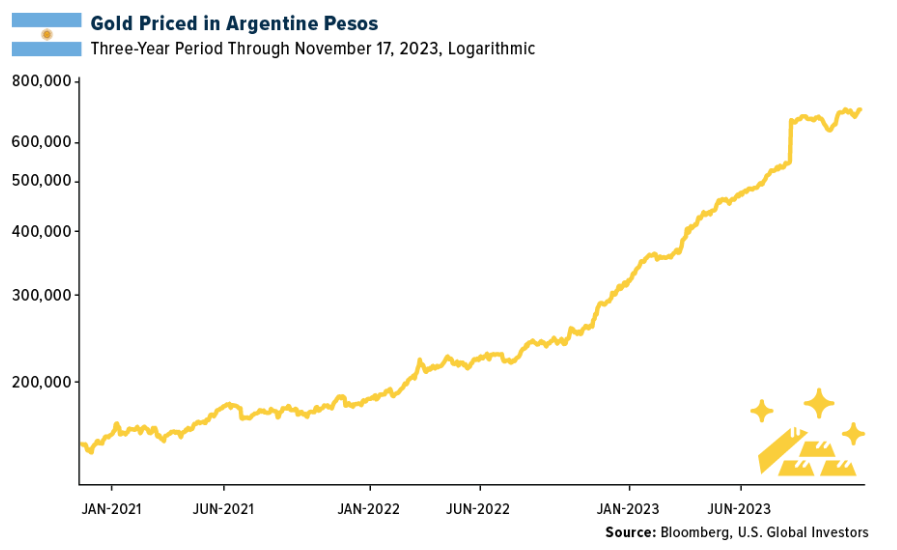

When I visited Argentina in August, just three months ago, one U.S. dollar was valued at 270 pesos. Today, on the black market, a greenback will get you over 1,000 pesos, if you can believe it. As a result, gold priced in ARS is at an all-time high of approximately 700,000 pesos, up 4.6 times from just three years ago.

Milei has a plan. The wild-haired author and economist says that, if elected, he will dump the peso for the USD and restore stability to the country. He’s also in favor of real assets such as gold and Bitcoin, joining a growing number of world leaders that have expressed support for the world’s leading cryptocurrency.

Even though it’s difficult for most Argentines to get their hands on U.S. dollars, they like paper money as a store of value. In India, as you know, families prefer gold, with Indian women owning six times more gold than can be found in Fort Knox.

While at the YPO event, it was a privilege to meet and chat with the U.S. ambassador to Argentina, Marc Stanley, who I was pleased to learn is from Dallas, Texas.

As Thanksgiving approaches, I find myself reflecting on the many reasons we have to be thankful for in this land of plenty. In particular, the season offers a moment to appreciate the shifts in our economy, as seen through the lens of our traditional Thanksgiving celebrations.

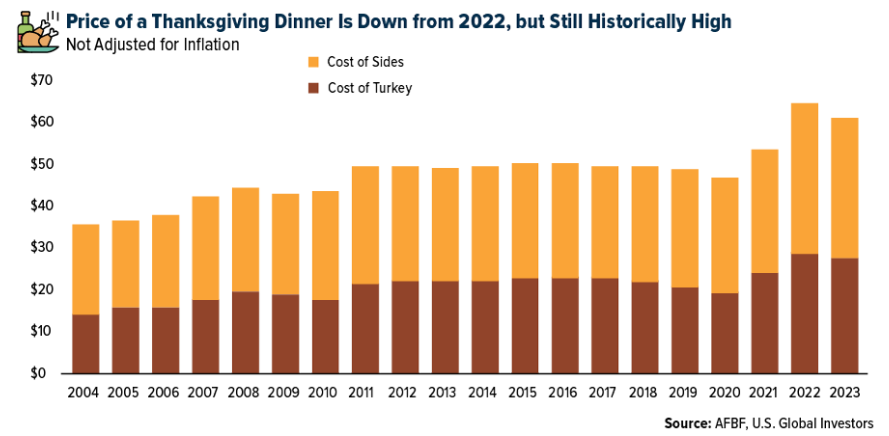

This year, the cost of a typical Thanksgiving feast for 10 is approximately $61.17, marking a 4.5% decline from last year’s historically high prices, according to the American Farm Bureau Federation. The centerpiece, a 16-pound turkey, now accounts for 45% of the Thanksgiving basket at an average $27.35, a 5.6% decrease from 2022.

Although the overall cost for a Thanksgiving dinner is still 25% higher than pre-pandemic levels, and although the price for some items rose slightly from last year, including pumpkin pie mix and dinner rolls, the overall decrease is a positive sign that inflationary pressures may be receding.

Besides the Federal Reserve’s monetary tightening efforts, one of the reasons for this is the resilience and superior efficiency of the U.S. food market. Despite global challenges like food inflation and supply chain disruptions, American consumers spend an estimated 6.7% of their disposable income on food, the lowest of 104 countries measured by the United States Department of Agriculture (USDA). This efficiency is a testament to the effective risk management that stabilizes agriculture markets in the U.S., a factor that keeps food prices comparatively low.

Thanksgiving Travel To Hit Near-Record High

Shifting the focus to travel, the American Automobile Association (AAA) projects a significant increase in Thanksgiving travel this year. With 55.4 million travelers expected, the U.S. is poised to witness the third-highest Thanksgiving forecast since AAA began tracking holiday travel in 2000.

This includes 49.1 million Americans driving to their destinations, benefiting from lower gas prices compared to last Thanksgiving. As of today, a gallon of regular gas costs $3.33 on average in the U.S., a more than 10% reduction from the same time last year, AAA says.

The number of air travelers is also on the rise, with 4.7 million people expected to fly over Thanksgiving.

If this ends up happening as AAA expects, it will mark the highest number of passengers since 2005.

These trends not only signal a return to normalcy post-pandemic but also hint at growing consumer confidence, an essential ingredient for economic growth.

Election Years And The Stock Market

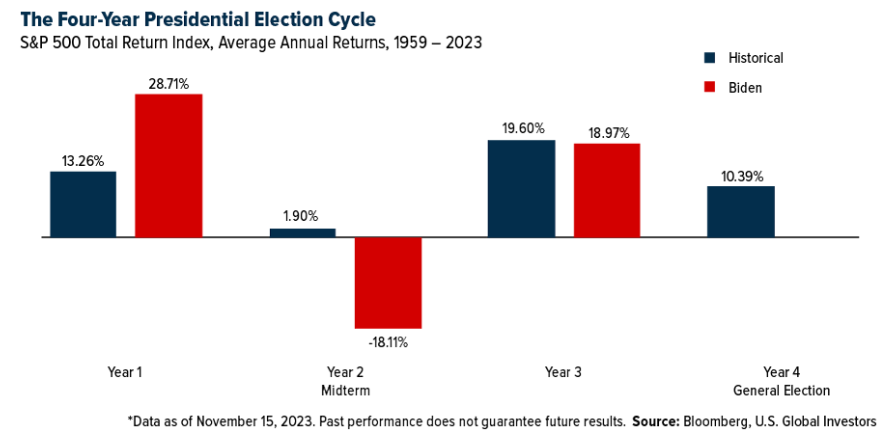

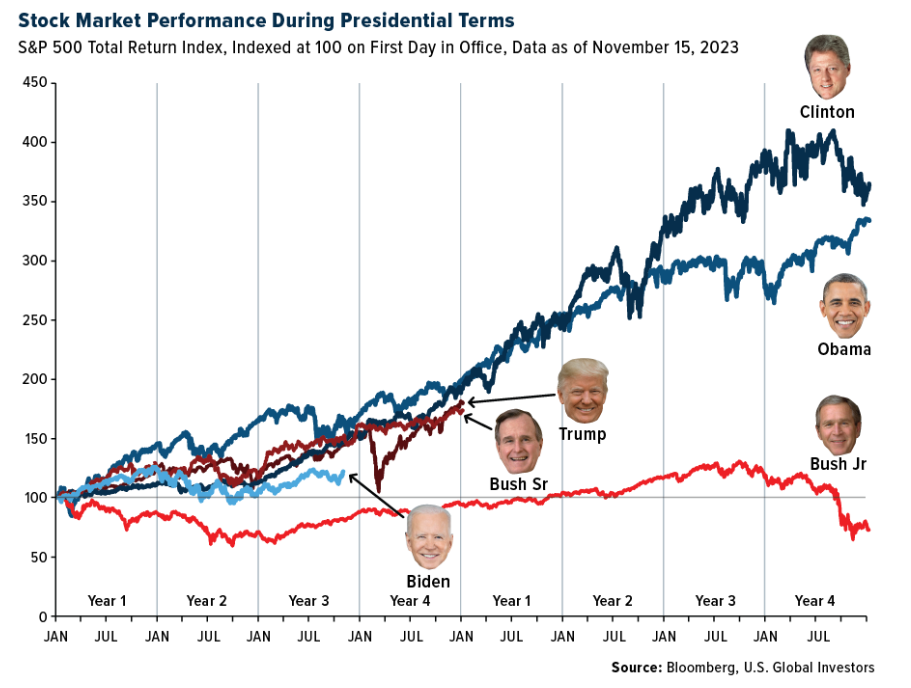

Turning our gaze to the stock market, it’s crucial for investors to understand how presidential elections can impact investments in the short term. Stocks have historically performed best during the third year of a president’s term, climbing 19.6% on average. If today marked the end of 2023, President Joe Biden’s third year in office, stock returns would be just under the average.

Contrary to what you might think, the data shows that stocks have trended upward regardless of which party wins the White House. As I’ve said many times before, it’s the policies that matter most, not the political party—and neither of the two major parties has a monopoly on good or bad ideas. Ours is a hyperconnected world, after all, and there are macro forces greater than the office of president that can have a significant impact on the performance of equities.

Indeed, over the decades, the S&P 500 has shown remarkable stability during presidential matchups, especially when there’s an incumbent running for reelection. Since 1952, the only three times when the market fell in an election year (1960, 2000 and 2008) were when two new candidates were on the ballot, according to Comerica’s weekly market update.

Here’s some good news: Real GDP growth has been strongest during the election year of first-term presidents, followed by even stronger expansion in the year following their reelection. Markets tend to favor certainty, even if the president is generally unpopular, as is the case with Biden.

The next thing we have to look forward to is primary season, which begins on January 15. I urge investors to stay the course. Expect volatility, but historically, stocks have returned 11.3% in the 12 months following primaries, compared to 5.8% in similar periods of non-election years, Comerica says.

The message is clear: It’s time in the market, not timing the market, that investors should be concerned about.

Happy Thanksgiving!

As we gather with family and friends this Thanksgiving, let’s be thankful for living in a country where food is (mostly) affordable, travel appears to have fully rebounded and our capital markets remain resilient amid political and economic uncertainties.

Let’s embrace the opportunities that lie ahead, especially in the upcoming election year, with the potential for the Fed to start lowering rates.

On behalf of the U.S. Global Investors team, I wish you and your family a happy, healthy and joyous Thanksgiving!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.94%. The S&P 500 Stock Index rose 2.22%, while the Nasdaq Composite climbed 2.37%. The Russell 2000 small capitalization index gained 5.38% this week.

- The Hang Seng Composite gained 1.61% this week; while Taiwan was up 3.15% and the KOSPI rose 2.50%.

- The 10-year Treasury bond yield fell 21 basis points to 4.438%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Allegiant Air, up 16.6%. Panama-based Copa Holdings earned $4.39 per share, ahead of the $3.32 consensus on better revenue, lower non-fuel unit cost, and lower non-operating expense with the settlement of the company’s convertible notes.

- Container import volumes at U.S. ports accelerated into the fall this year defying most expectations and historical peak season declines despite many reports of weak volumes and falling rates. The monthly data from logistics technology platform provider Descartes Systems Group points to surprising strengths.

- According to CIBC, while there are concerns over a weakening Canadian consumer paired with comments by U.S. domestically oriented airlines on softer demand during this off-peak season, Air Canada says its demand profile remains healthy. The airline noted differences between the two markets – the U.S. market restarted from the pandemic earlier than other parts of the world, which drove a faster recovery in its domestic market. U.S. domestic capacity is ahead of 2019 levels, which has created a supply/demand imbalance in this market, especially as travelers have looked to international destinations.

Weaknesses

- The worst performing airline stock for the week was Skymark Air, down 2.5%. According to Bank of America, United Airlines lowered Asia-Pacific flying in January/February by -12.6%/-8.5%, respectively. All reductions were driven by updated China schedules as United had previously loaded pre-pandemic schedules for the market, much of which is prohibited by flight restrictions between the countries. Outside of San Francisco to Beijing and Shanghai, United has now removed all China flights from its schedules through mid-February.

- Cargo volume is not weak, so the outlook is not gloomy. However, global economic recovery is required given the large supply of newly built vessels. Budgets are now being made under the assumption that the outlook for fiscal year 2024 is not very encouraging. Downside risk is falling, owing to countermeasures including slower steaming speeds.

- Chinese capacity is growing faster than demand. Domestic ASKs were up 17.2% (-2.0% month-over-month) and up 13.0% (-0.0% month-over-month) versus October 2019 levels for China Eastern and China Southern. China Air’s domestic ASK was up 19% versus its 2019 level.

Opportunities

- ISI tracks web traffic to airline websites as a proxy for bookings. Airline web traffic increased 6% year-over-year for the week, compared to 7% higher year-over-year in the trailing four-week period. Visits to most carriers’ websites accelerated, except for Alaska, Hawaiian, Spirit and United.

- Air cargo could benefit from a reduction in ocean shipping reliability next year as box lines contend with antitrust rule changes. Reliability was by far the most important driver of choice, ahead of environmental impact and price. Airfreight rates could rise – indicating higher demand – when ocean schedule reliability decreases. Airfreight rates reached a peak in April last year when ocean reliability was at its lowest.

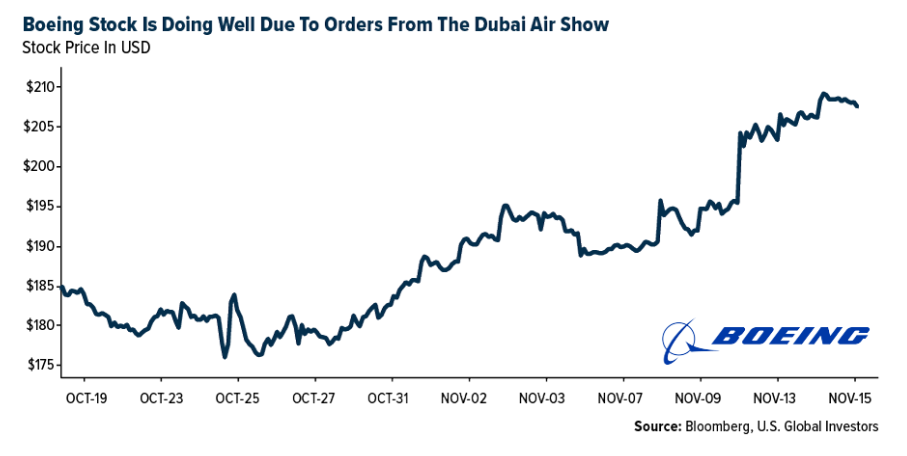

- According to Goldman, Boeing has seen strong new aircraft orders recently, including from the Dubai Air Show. That includes demand across the airplane product set, both narrowbody and widebody. China remains a potential incremental addition to demand, though the medium-term skyline remains full even if that does not come through soon. Goldman continues to believe Boeing new aircraft supply is well below demand, but that deliveries will ramp up substantially through end of 2023, into 2024, and beyond.

Threats

- Two articles by Aviation Week highlight continuing ATC issues in the U.S. and Europe. The FAA hired 1,500 controllers in fiscal year 2023 (September through year-end) and has requested a budget for 1,800 in 2024. Even with the boost in new hires, however, they will need 10 years to meet minimum controller staffing needs. Additionally, ATC system upgrades planned in France are expected to reduce 20% of flights from major French airports in January/February. Air France will have to cancel 4,300 flights over the two months.

- Following the driest October at the Panama Canal since the 1950s (41% lower rainfall than usual), tanker and bulker fluidity is expected to worsen. The Panama Canal now has a queue of 120 ships in waiting, above the 90-ship average over the past seven years. Canal waiting times have increased to six to eight days in September from two to three days in June. Given the transit challenges, tankers/dry bulkers have lengthened trade routes as canal bottlenecks build.

- According to Bank of America, the impact of the geared turbofan (GTF) engine issue on Wizz Air’s capacity is larger than anticipated. Although the compensation from Pratt & Whitney (PW) is reassuring, the earnings outlook until fiscal year 2026 estimate (FY26E) is uncertain. With 45 aircraft grounded due to the impact of the PW GTF engine issue, there is no capacity growth in fiscal year 2025 estimate, followed by a big step-up in FY26E. This, along with the airline’s Middle East exposure, makes the next two years an operational challenge, and creates uncertainty for its ultra-competitive unit cost position.

Luxury Goods And International Markets

Strengths

- Retail sales were the bright spot of economic data that came out of China this week. Sales increased 7.6% while Bloomberg economists were expecting 7.0%, above September’s 5.5%. This was the strongest growth reported since May, and was mainly supported by leisure products, communication equipment, and automobiles.

- Bank of America’s latest Global Fund Manager Survey shows 76% of respondents were convinced that the Fed had finished its rate hike cycle, up from 60% in October and the highest level since the survey began tracking the topic in May. The survey also revealed a big drop in cash holdings to a two-year low, along with the first overweight in the equity positioning since April 2022.

- Williams Sonoma, a home furnishing company, was the best performing S&P Global Luxury stock, gaining 20.6% in the past five days. Shares gained after the company reported a quarterly earnings beat. RBC Capital Markets said that the company is well positioned to gain market share, but the road ahead is likely to be bumpy.

Weaknesses

- Bloomberg reported that prices for used Rolex and Patek Philippe watches fell to a fresh two-year low on the secondary market last month as demand continues to decline amid rising supply. The Bloomberg Subdial Watch Index dropped 1.8% in October, sinking to its lowest level since 2021. The Index, which tracks prices for the 50 most traded watches by value on the secondary market, is now down 42% since its peak in April of 2022.

- Burberry Group Plc cautioned that its annual revenue target is in jeopardy as sales stagnated in the latest quarter, attributing the struggle to a downturn in global luxury demand. With CEO Jonathan Akeroyd’s efforts to revitalize the brand amid lackluster consumer response to designer Daniel Lee’s creations, Burberry shares plummeted to their lowest point in over a year, losing more than one-fifth of value in 2023.

- Faraday Future Intelligence was the worst performing S&P Global Luxury stock, losing 28.1% in the past five days. The company announced a quarterly earnings miss. However, the quarterly net loss shrank 35% to $78 million from $119.9 million a year earlier. Net loss per diluted share also fell to $3.78 from $27.67.

Opportunities

- Softer-than-expected inflation data in the U.S. may suggest that the Federal Reserve tightening cycle is over. Fed fund futures imply expectations of no further rate hikes in the current year and about 100 basis points of cuts next year, according to FactSet. Interest rates in the U.S. dropped while the U.S. dollar corrected, supporting domestic and international equities.

- Bloomberg reported China is considering providing at least CNY 1 trillion ($137 billion) of low-cost financing to urban village renovation and affordable housing programs as it looks further to support the housing market. This could be Beijing’s largest step to-date to support the housing market and it could start as early as this month.

- JPMorgan hosted a luxury conference this week in the heart of Paris, at its headquarters located in Place Vendome, built by King Louis XIV in 1686. It was the King’s wish for the center of Paris to hold a strong public square. Place Vendome is also home to many luxury stores. Shops on the Rue Saint-Honore are busy with tourists from around the world. The JPMorgan conference was well attended, showing strong interest in luxury goods and services.

Threats

- Bain & Company, a consulting group in the luxury sector, said that the sector is experiencing normalization. Last year the sector was able to grow, on average, at 20%. This year the growth rate should be around 8-9%, much closer to the sector’s long-term average of 6%. The company expects the growth to slow down next year to 4-5%, below its long-term average. Bain & Company expects a slower first half of 2024 and a stronger end of 2023.

- In October, Li Auto surpassed Tesla in car sales, delivering a record 40,422 electric vehicles compared to Tesla’s 28,626 units, marking a significant turnaround from September. Li Auto, focusing solely on SUVs with a unique fuel tank charging system, plans to maintain a similar delivery pace in the ongoing quarter and anticipates delivering 41,700 to 42,600 vehicles monthly in the fourth quarter. Despite China representing only about one-fifth of Tesla’s sales by monetary value, Tesla faces growing threats from domestic rivals like Li Auto, BYD, and XPeng, all of which continue to gain momentum and expand their market presence.

- Federal prosecutors announced the largest-ever U.S. seizure of counterfeit designer goods, valued at over $1 billion, leading to charges against Adama Sow and Abdulai Jallow for running the illicit operation from a Manhattan storage facility. Indictments reveal that Sow, residing in Queens, and Jallow, based in Manhattan, face up to 10 years in prison if convicted, with over 83,000 knock-off items, including handbags and accessories from renowned brands, seized from their controlled premises.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was uranium, as proxied by the Sprott Physical Uranium Trust, rising 6.59%. Positive fundamentals exist with limited new supply and increasing demand for nuclear power to play a bigger role in electricity with the production of greenhouse gases. According to Bank of America, polyethylene data published by the ACC indicated a big increase in U.S. production and exports year-over-year in October. More specifically, polyethylene production in October was 4.95 million pounds, up 3.9% month-over-month and up 16.6% year-over-year.

- According to BMO, the spot Hot-Rolled Coil Steel (HRC) prices in the U.S. increased nearly 19% over the past two weeks to $950 per ton (the highest since June) as mills stood firm on pushing spot prices higher amid limited spot availability. Looking ahead, with lead times extending into January, utilization rates still relatively subdued, scrap prices expected to increase again in November, and typically seasonally stronger first quarter demand period still forthcoming, in their view, mills currently continue to maintain pricing power and are likely to attempt further price increases.

- Copper steadied after its biggest advance in a month following key U.S. inflation data, while top industry executives gathered in Shanghai to discuss the metal’s outlook which was largely skewed to the bearish side with the patchy recovery in China. Higher initial jobless claims also reinforced the view that the Fed is finished raising interest rates, allowing copper to have its best weekly gain since July.

Weaknesses

- The worst performing commodity for the week was wheat, dropping 3.67%, as cheaper supplies from Russia and Ukraine squeeze domestic prices lower. SQM’s third-quarter revenue and net income fell by 31% and 47%, respectively, on a yearly basis, according to consensus. EBITDA should fall 54% yearly and 13% quarterly to $765 million due to the sharp decline in lithium prices from the rally in the third quarter of last year, according to Itau BBA.

- Global oil markets will not be as tight as expected this quarter, as upward revisions to demand are outpaced by upgrades to supplies, the International Energy Agency said. The IEA boosted forecasts for world fuel consumption this year on surprising strength in China, and still anticipates a supply shortfall during the fourth quarter. However, it will be roughly 30% smaller than previously projected, at about 900,000 barrels a day.

- Zinc inventories on the London Metals Exchange (LME) jumped 139% on Thursday, the biggest daily increase in five years, as reported by Bloomberg. Zinc is the second worst performing metal on the LME this year despite exchange inventories being relatively low all year by historic standards. New zinc supplies from Australia and Russia are forecast to keep the market in surplus.

Opportunities

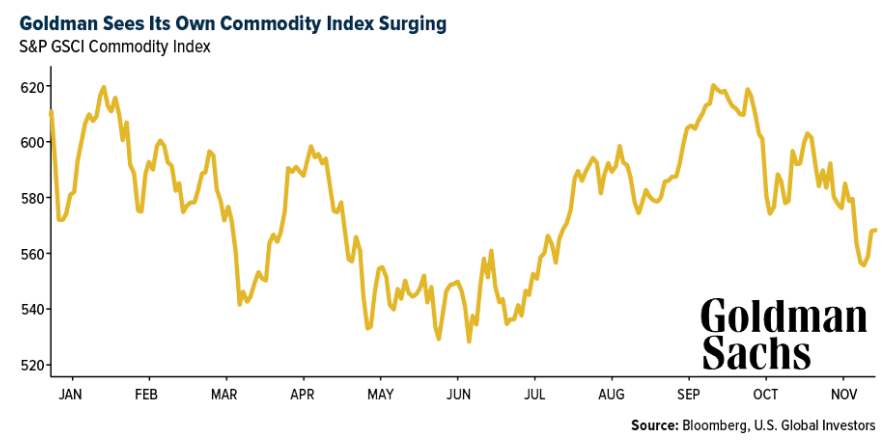

- Goldman recommends going long commodities in 2024, as the bank expects somewhat higher spot commodity prices, strong carry, and sees hedging value against geopolitical supply disruptions. Goldman forecasts a 21% GSCI 12M total return. The group believes that a fading monetary policy drag, receding recession fears, and reduced industrial destocking will support demand and spot prices in 2024. They now forecast Brent to rise to a 2024 average of $92 per barrel.

- According to Bank of America, China’s investment in renewables and electric vehicles has single-handedly carried especially the copper market this year. Looking beyond China and into next year, the latest IEA forecasts of renewables installations and BofA’s car production forecasts suggest that U.S. copper demand could expand by around 10%, two-thirds driven by renewables and one-third by the automobile industry.

- Glencore Plc will buy a majority stake in Teck Resources Ltd.’s coal business, ending a months’ long saga that transfixed the mining industry and setting the stage for the commodity giant to exit the coal business itself. The two companies have spent much of the year in a bitter public fight after Teck rejected an unsolicited $23 billion offer from Glencore, which proposed creating two new metals- and coal-focused companies. The Glencore offer, while unsuccessful, was enough to disrupt an earlier plan by Teck to spin off its coal business.

Threats

- China is amid a breakneck expansion of its copper industry that is reshaping global flows of the essential metal for the world’s energy transition. The Asian nation’s grip on the supply of other green metals like lithium, cobalt, and nickel, used in electric vehicle batteries, has already prompted worried Western governments to encourage separate supply chains. Meanwhile, China’s production of refined copper — and its share of world output — is heading for a record this year after a burst in construction of new smelters.

- The risks posed in Panama, where First Quantum Minerals operates its flagship mine, outweighs the rewards, Orest Wowkodaw of Scotiabank says. First Quantum’s shares are down 48% over the past month due to heightened uncertainty around the Cobre Panama mine’s future, made more acute on Monday after the company said it would curb some operations due to a port blockade by protesters. The fate of the mining contract is now in the hands of the country’s supreme court, with a ruling expected after November 23.

- At Friday’s opening trades in crude oil, technically over the past four weeks oil has descended into a bear market. However, analysts at Goldman Sachs Group said they expect OPEC+ to act to further support prices when the group meets next week. That message led to a 4% rally in crude on Friday. In the U.S. the net national saving rate has now turned negative. Outside a recent reading and during the GFC, the net national savings rate has only had been negative since the government began collecting data in 1947. Clearly the consumer is losing momentum.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was Celetstia, rising 158%.

- The decentralized exchange PancakeSwap has launched a gaming marketplace. The new platform lets developers build, launch, and update games with Web3 elements such as cryptocurrency and NFTs, writes Bloomberg.

- Bitcoin was in sight of $38,000 this week, a level last seen in May 2022, amid an ongoing rally spurred by expectations of fresh demand for the token from ETFs, according to Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Gas, down 59%.

- Coinbase Global is one of the most important investors in the world of cryptocurrency. It’s the all-time biggest backer of industry startups in terms of number of deals, according to PitchBook data. However, in recent months, its investing activity has fallen off, writes Bloomberg.

- The head of Dubai’s crypto regulator is poised to depart after less than a year on the job, just as authorities prepare to impose sweeping fines on non-complaint digital-asset firms operating in the Emirate, writes Bloomberg.

Opportunities

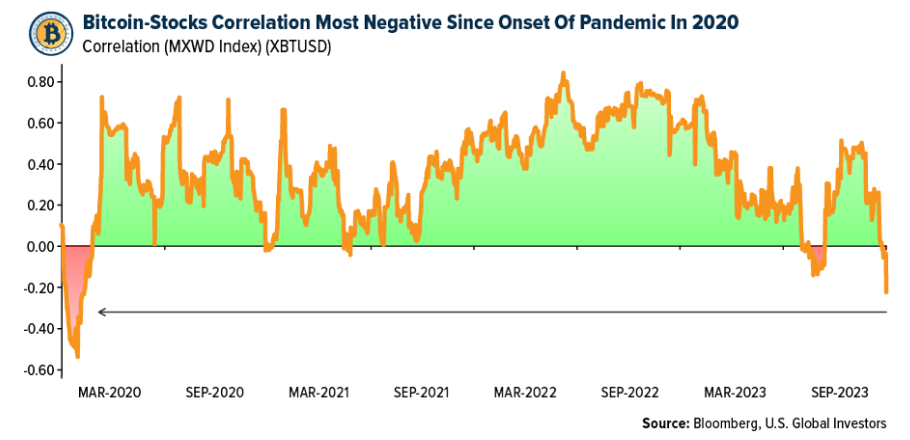

- A 30-day correlation coefficient for Bitcoin and MSCI Inc’s gauge of world stocks now sits at -23, the most negative since the onset of the pandemic in early 2020. A reading of 1 indicates assets are moving in lockstep, while -1 would show they’re moving in opposite directions, writes Bloomberg.

- CoinShares, one of Europe’s largest cryptocurrency asset managers, has secured the option to acquire exchange-traded funds from competitor Valkyrie, which is preparing a spot Bitcoin fund that’s awaiting regulatory approval, writes Bloomberg.

- Tether Holdings is taking steps to become one of the world’s top Bitcoin miners as the $87 billion stablecoin operator makes a hefty investment in the already highly competitive sector. The company plans to spend about half a billion dollars over the next six months, writes Bloomberg.

Threats

- Terraform Labs co-founder Do Kwon was sentenced to four months in prison by a Montenegrin court for attempting to travel with a forged passport. The police said he was in possession of multiple passports including a forged Belgium and Costa Rican one, writes Bloomberg.

- Jump Trading Group has parted ways with Wormhole, the crypto project it injected about $320 million in almost two years ago following a massive hack, as the market maker retrenches in the digital-assets space, writes Bloomberg.

- Ethereum layer-2 solution Polygon recently witnessed an extraordinary surge in gas fees. It topped the charts with an increase of over 1,000%. This spike, peaking at $.10, was primarily driven by POLS minting activity, writes Bloomberg.

Gold Market

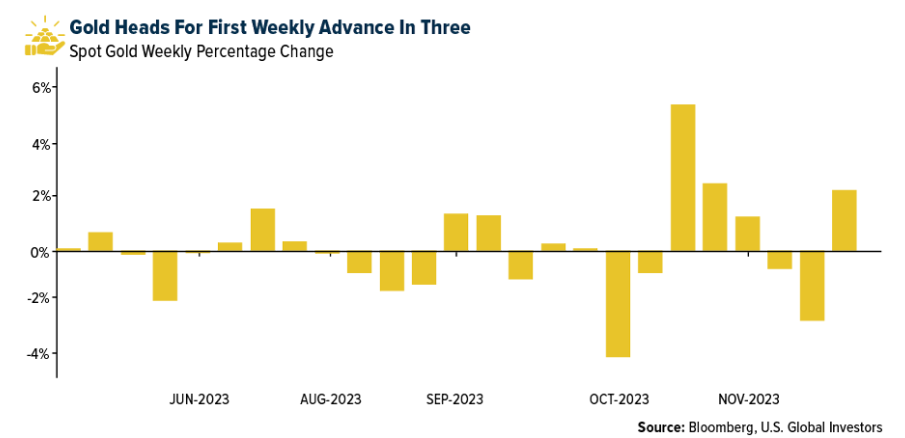

This week gold futures closed at $1,983.20, up $45.50 per ounce, or 2.35%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 4.23%. The S&P/TSX Venture Index came in up 3.96%. The U.S. Trade-Weighted Dollar tumbled 1.89%.

Strengths

- The best performing precious metal for the week was palladium, up 8.50%, likely on the prospects of interest rate cuts that could spur industrial growth and stronger auto demand. Gold jewelers made brisk sales in India on the Diwali weekend with consumers’ interest riding on a recent drop in prices. Jewelers feared hesitancy among buyers during the festival season after bullion prices jumped due to the Israel-Hamas War in early October. This week, gold headed for its first weekly gain in three, as reported by Bloomberg.

- According to Canaccord, B2Gold reported a better-than-expected quarter with 4% higher production than their forecast and 15% more ounces sold. Combined with cash costs that were 2% higher, EBITDA of $259 million was 19% ahead of their forecast of $217 million.

- Argonaut Gold reported adjusted basic earnings per share for the third quarter that beat the average analyst’s estimate. Adjusted basic earnings per share (EPS) was $0.01 versus a $0.47 loss per share (Bloomberg Consensus) Revenue of $104.8 million, +39% year-over-year, versus the estimate $107 million. Gold production was 53,911 equivalent ounces, a +17% increase from last year.

Weaknesses

- The worst performing precious metal for the week was gold, but still up 2.35%. According to BMO, Lucara Diamond Q3/23 production was 98,000 carats, lower than the consensus of 107,000 carats, driven by lower processed head grades. Given the weaker diamond market environment and the uncertainty around the timing of sales of the >10 karat diamonds, revenue expectations have been lowered to $160-190 million ($200-230 million previously) on diamond sales of 365,000-385,000 carats.

- According to Stifel, Orla Mining released Q3 financial results after pre-reporting strong gold production of 32,400 ounces and increasing its FY23 production guidance. Adjusted EPS and cash flow per share (CFPS) came in at $0.02/$0.06, lower than their estimated $0.05/$0.07, driven by higher operating costs, tax expense and exploration spending.

- According to Morgan Stanley, the volume of India’s rough diamond imports in October increased by 29% YoY (10% MoM) and their value appreciated 9% YoY (but down 1% MoM). This implies that rough prices may have declined by 15% YoY and 10% MoM. The value of polished stone exports from India—a proxy for demand—was down 33% YoY (25% MoM), while volumes decreased by 33% YoY (20% MoM), implying aggregate prices remained flat YoY, but down by 5% MoM.

Opportunities

- Calibre has agreed to purchase on a non-brokered private placement basis 66,666,667 common shares of Marathon at C$0.60 per share for gross proceeds of C$40million. Marathon shareholders will receive 0.6164 of a Calibre common share for each Marathon common share held, implying a value of C$0.84 per Marathon common share.

- UBS expects gold to reach new heights in 2024 and 2025 as the cycle matures and softer data ahead shifts the narrative to recession risks, falling real rates and Federal Reserve policy easing with the likely re-emergence of strategic positioning from investors, underpinned by a continuation of strong official sector purchases and steady fundamental demand. If they run their gold models at spot and assess what is priced in based on EV/EBITDA, free cash flow (FCF) yield and net present value (NPV), they calculate the SA gold equities are pricing in $1,800 per ounce, implying 20% plus upside risk if their 2025E average gold price forecast of $2,200 is achieved.

- Wheaton Precious Metals announced the acquisition of two existing streams from Orion Mine Finance for $450 million. These include gold and palladium/platinum streams on the Platreef project (South Africa, owned by Ivanhoe Mines) and a gold/silver stream on the Kudz Ze Kayah project (Yukon, owned by BMC Minerals). Concurrently, Wheaton announced an agreement to create a new stream on the Curraghinalt Project (Ireland, owned by Dalradian Gold) for $75 million ($20 million upfront).

Threats

- De Beers plans to stockpile unsold diamonds after the world’s biggest producer responded to plunging prices by allowing its buyers to refuse to purchase all the stones they are contracted to buy. “We build up stocks of those because we are confident that over time the diamond price will increase and we will be able to sell that supply into the growing demand that we believe will come,” Chief Executive Officer Al Cook said at a briefing in Gaborone.

- Precious metals are being stolen from catalytic converters. The new and the old metals would later be blended under intense heat, then shipped to a refinery. Recycling catalytic converters costs less than mining ore. But it carries a risk, as Stillwater discovered after paying more than $170 million for used ones, many of them stolen, according to an indictment handed up this spring on Long Island that implicated the mine.

- Russian gold is still finding its way into international markets despite being blocked from sales in the United Kingdom. Russia switched to Dubia and sold 96.4 tons of gold through the United Arab Emirates (UAE) in 2022, making it the country’s largest supplier as reported by Bloomberg. Last week, the U.K. issued sanctions on counter parties in the UAE that delt with Russian gold trading, seeing those threats coming, in April 2023, Russian shipments of gold to Hong Kong have picked up dramatically with 68 tons of imports this year. China could easily be the counterparty to these gold trading flows.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (09/30/2023):

Copa Holdings

Air Canada

United Airlines

Alaska Air Group

Hawaiian Holdings

Boeing

Air France-KLM

Tesla

Burberry Group

B2Gold Corp.

Lucara Diamond Corp.

Calibre Mining Corp.

Wheaton Precious Metals Corp.

Ivanhoe Mines Ltd.

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The S&P 500 Total Return Index is calculated intraday by S&P based on the price changes and reinvested dividends.

The Bloomberg Subdial Watch Index tracks prices for the 50 most traded watches on the secondary market by value.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All