Housing markets are cooling but unlikely to end in a bust.

There were only a few good things that came out of the pandemic. One of them was historically low interest rates that helped those looking to borrow. Homeowners across markets were able to lock in cheap mortgages at attractive prices.

Those factors, combined with a new normal of working from home, drove a home-buying frenzy. Residential real estate prices in much of the world rose sharply, recording gains of up to 40% from their pre-pandemic levels in high-income countries last year.

But good times don’t always last. Prospective home buyers have come to realize this over the course of 2023. The housing market in many nations has been turned on its head by high mortgage rates, falling property prices, and stretched affordability.

Borrowers looking to secure new mortgages or refinance existing ones are seeing a sizeable increase in payments on the back of aggressive central bank tightening and the ensuing rise in longer-term interest rates. The jump in interest costs hurts families in almost all economies; however, the hit to household balance sheets varies across markets.

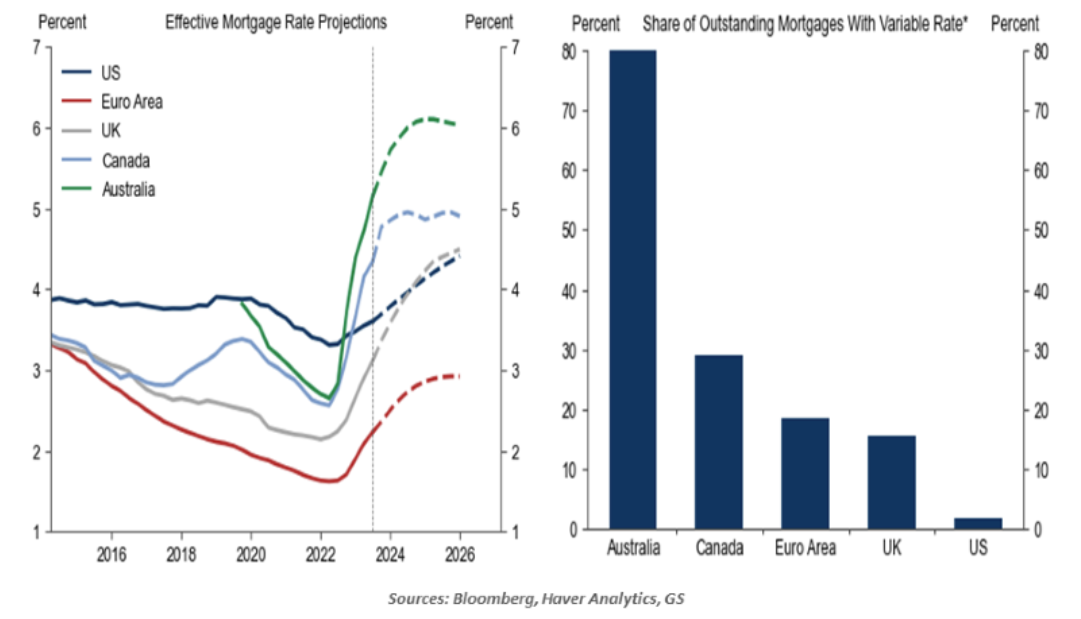

The key differentiators are the share of fixed vs. floating rate mortgages and the amount of debt held by homeowners. Among the major advanced economies, Australia, Canada, and the U.K. have witnessed the biggest rise in effective mortgage rates for new loans since 2022. Short-term or variable mortgages are the norm in these countries.

As part of its policy response at the height of the pandemic, the Reserve Bank of Australia (RBA) provided banks access to cheap three-year fixed interest credit, which was passed onto borrowers in the form of ultra-cheap home loans. This led to a surge in fixed-rate borrowing and refinancing. However, according to RBA data, 590,000 loans pegged to near-zero interest rates switched to much higher floating rates in 2022, with another 880,000 mortgages to roll off this year and 450,000 in 2024.

A combination of higher borrowing costs and the prevalence of short-term fixed-rate mortgages are contributing to higher payments for Canadians and Britons too. Mortgages in these markets typically have rates locked for a period of just two to five years. Data from the U.K. Office for National Statistics shows that over 1.4 million British households will be affected by much higher monthly repayments this year alone, as they roll off fixed-rate deals that were set when policy rates were near zero.

Unfortunately, there is more pain in store for homeowners in these regions. As interest rates reset and borrowers refinance or take new loans, the effective mortgage rate will rise further in the coming months (see above chart).

Low borrowing costs triggered a refinancing boom in the U.S., too. Because of long rate locks, rising rates have not yet impacted many U.S. homeowners. While the new 30-year fixed mortgage rate surged to 8% recently, the average rate on an American home loan is still under 4%. The preservation of purchasing power is one of the reasons behind the resilience of American consumer spending.

This situation will change gradually in the coming years as homeowners relocate. In the U.S., people move homes at a rate of about 5% each year. As this occurs, it will create a headwind for consumption.

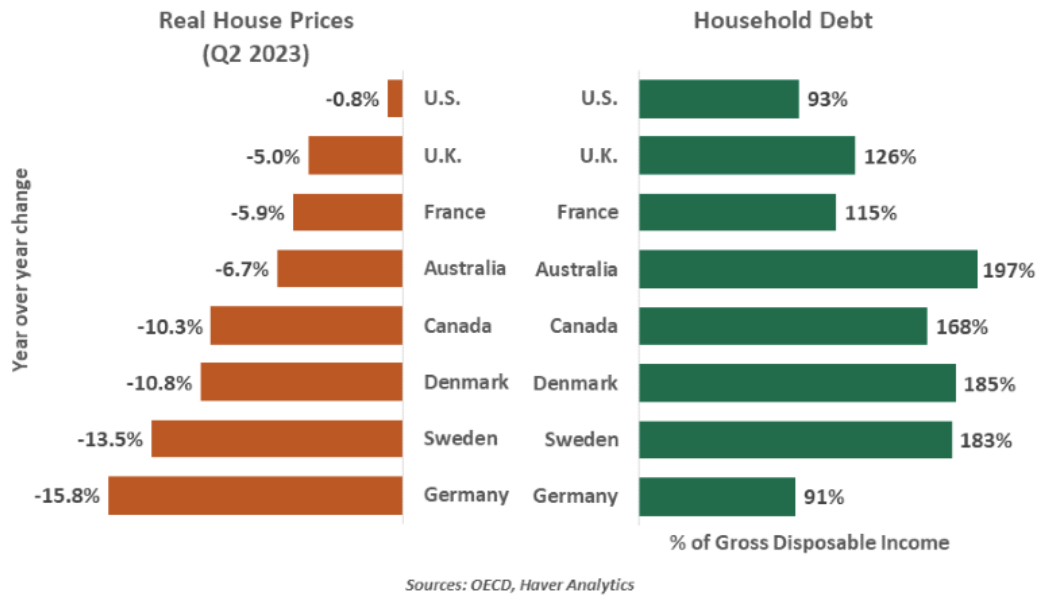

Within Europe, lender offerings and rules vary noticeably. Some countries have much longer interest rate locks than others; some have experienced more significant growth than others. As shown in the chart, house price performance within the EU shows considerable variance.

Increased debt service burdens are gradually restraining household income and spending. Borrower credit quality has fallen somewhat and mortgage delinquencies have risen somewhat (albeit from low levels). Canadian and Australian families are among the most vulnerable, as those countries have very high levels of household debt. While uncomfortable, the hit to households should be manageable, as strong labor markets and rising interest rates should help offset the pressure from rising interest expenses.

Amid higher financing costs, house prices are falling across the developed world as demand moderates. The correction is substantial in markets where floating or short-term fixed rate loans account for the lion’s share of outstanding mortgages. The hotter a market was in the boom, the more significant its cooling today.

All good things come to an end, but so do all the bad things. While mortgage rates are unlikely to return to pandemic lows anytime soon, they are also unlikely to stay as high as they currently are beyond 2024. Easing borrowing costs will, in due course, make the housing market more active and attractive again.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

More Exchange-Traded Products Topics >