- We believe markets are adjusting to an economic outlook of sticky inflation rather than a soft landing with declining inflation.

- Rates are likely to rise across the yield curve, but risk assets may show greater tolerance for higher rates.

- U.S. growth is surprisingly strong, Europe is stagnating, and China is beginning to improve.

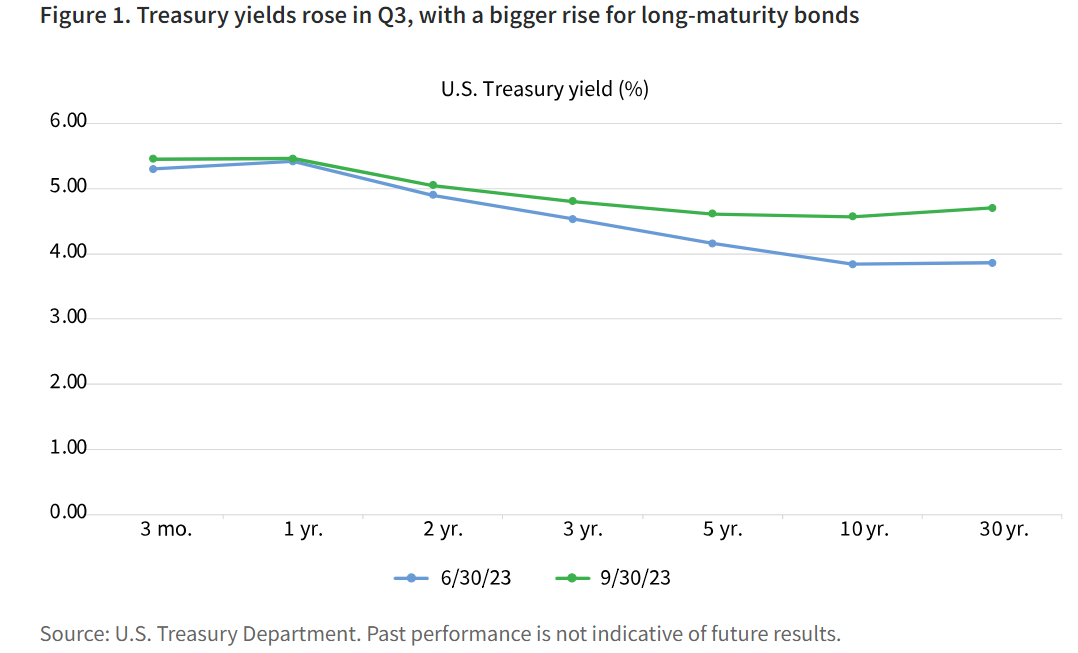

Recent economic data, we believe, suggests sticky inflation with positive GDP growth is more likely in 2024 than a soft landing. We expect that interest rates will stay higher for longer on the back of increased Treasury supply and hawkish Federal Reserve rhetoric. As fixed income markets are forced to consider this prospect, rates are likely to move higher across the yield curve.

At the same time, the markets’ confidence that the economy can tolerate higher rates appears to have risen, and risk assets have continued to show resilience. Risk assets may also draw fundamental support from large fiscal deficits, we believe. Higher rates and higher asset values can exist together. Weak data could change this trend. Housing might be the sector that shows weakness and could influence markets and the Fed.

The Fed does not appear to think that inflation is sticky. Given recent moves higher at the long end of the yield curve, we believe the Fed’s willingness to raise policy rates is much lower. Even hawkish members of the Federal Open Market Committee have signaled a preference for a pause. In our view, the Fed is unlikely to hike in November and will signal a hawkish pause in December.

In the near term, we expect the U.S. inflation rate will fall to the 3.0%–3.5% range, interest rates will remain elevated, and spreads will be flat to slightly tighter. We believe a U.S. recession is possible in the second half of 2024. If the U.S. avoids a recession in 2024, we believe the Fed may not cut rates at all. As liquidity continues to be withdrawn, financial market risks will increase, in our view

U.S. growth surprises

The Atlanta Fed’s Q3 GDP growth forecast has been fluctuating around 5%, indicating acceleration from previous quarters. Consumer spending is strong, as households have been spending more than they could if they only relied on their incomes. The gap between GDP and GDI (gross domestic income) indicates the difference between income and consumption. Real disposable income declined, at the pace of –0.2% M/M, two months in a row while households continued to spend. The saving rate dropped to 3.9% in August.

Manufacturing PMIs improved in September while services PMIs slowed. The labor market has remained strong. Total nonfarm employment increased by 336,000 in September, and the previous two months’ employment was revised up by 119,000. Housing activity is losing momentum after stabilizing early in the year. NAHB’s builder confidence index has dropped as mortgage rates — now above 7% — were observed to be slowing demand.

With Europe stagnant, the ECB pauses

The euro area continues to struggle with weak external demand and the energy transition, which is keeping manufacturing structurally constrained. Domestic activity has been losing momentum for the last couple of months. September PMIs remained in contractionary territory. The ECB hiked the key policy rates by 25 basis points (bps) and signaled the likely end of its tightening cycle in September. It raised inflation projections for 2023 and 2024 while reducing the 2025 projection to 2.1%, slightly above target. With the meeting statement, along with the 2025 inflation projection, the Governing Council of the ECB signaled its intention to pause rate hikes for a sufficiently long period.

China is beginning to improve

Chinese policymakers have announced a large number of “small” stimulus measures, as the property market and the overall economy looked likely to lose momentum early in the third quarter. In September, activity data started to surprise to the upside, showing early signs of stabilization. The policy announcements could likely put a floor to deteriorating sentiment and economic growth, although the durability of China’s recovery could become questionable.

China’s exports and imports ticked up in August, surprising to the upside. While the increase in exports was marginal, global demand might be showing signs of stabilization after a steady decline from the highs. Exports to many regions ticked up, but European demand continued to weaken. China’s commodity demand stayed stable in volume terms. Inflation is bottoming out as in the rest of the world.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Putnam

Read more commentaries by Putnam