Capital Markets Outlook offers perspective on the global economy and asset classes with insight on market history.

Jason Vaillancourt is a Global Macro Strategist on the Capital Market Strategies team. He provides in-depth global macroeconomic research to Putnam clients and the broader financial community.

- After a CPI surprise, central bankers want their inflation-fighting efforts to be taken seriously.

- The real interest rate has only recently turned positive, making policy its most restrictive since 2007.

- Wide-ranging opinions on the state of the economy and business cycle point to a possible market inflection.

There are periods of time in the investing world when contradictions and disagreement among “experts” run rampant. Often, those periods tend to coincide with inflection points in cycles, although you only really know that with the benefit of hindsight, in my opinion. My two decades of experience managing multi-asset portfolios reinforced the following first principles in times of stress.

- The way to compound wealth and give investors the best chance of success has remained unchanged:

- Be a little bit more right than wrong.

- Try and structure positions so the magnitude of wins is larger than the magnitude of losses.

- Ruthlessly exploit diversification wherever you can find it.

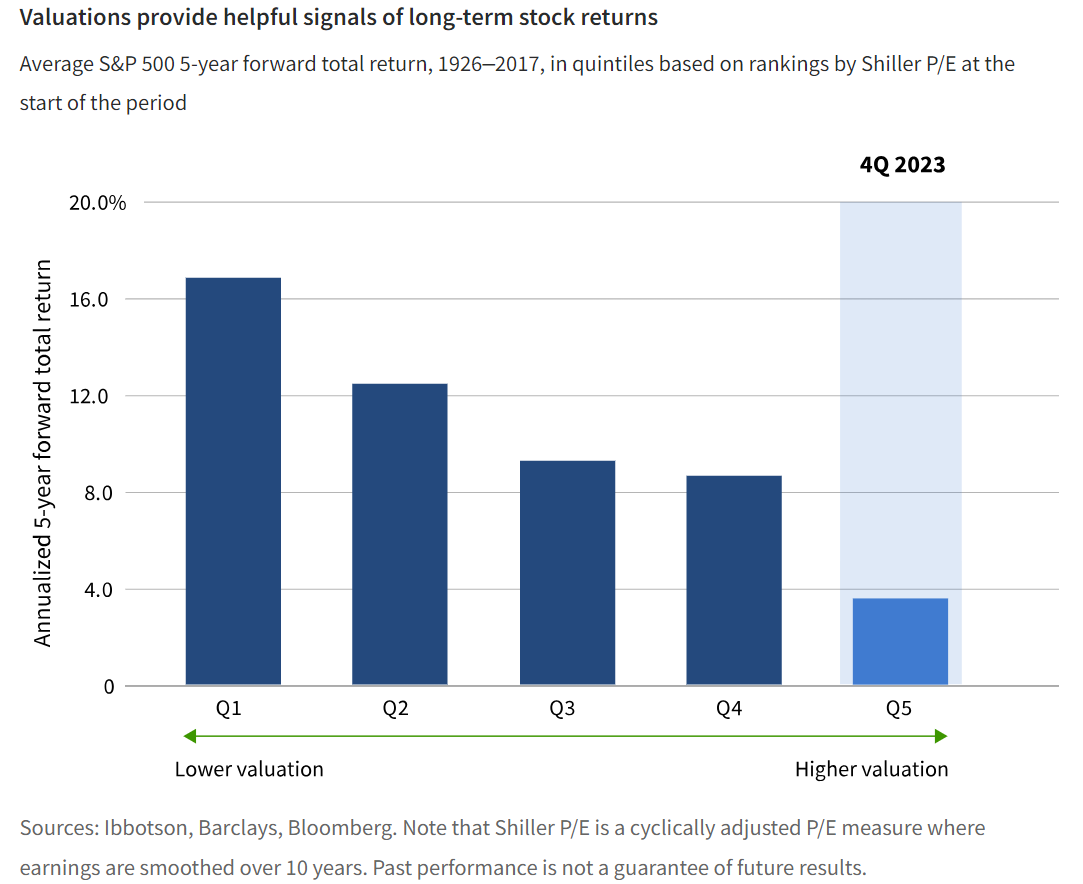

- And while we know that valuation is a poor timing tool, over a long enough horizon, it is undefeated.

We chafe when we hear pundits say things like “You can’t time the market.” Surely, if one is measuring success over days or weeks, that is probably true. But for those who are long-term investors, and not traders, valuation remains a compelling tool.

Caution has been rewarded

In writing the Capital Markets Outlook over the past decade, I have primarily sought to be a pragmatic realist, as opposed to a perma-bull or perma-bear, neither of which is particularly helpful to anyone. It is true we have leaned toward recommending a relatively risk-averse posture over most of the previous couple of years. But, in fairness, the S&P 500 has provided a price return of pretty close to zero since the summer of 2021 with quite a bit of volatility (which makes for a pretty lousy Sharpe ratio). And when it comes to recession forecasting, it is certainly unhelpful to investors to be the boy who cried wolf. But if you care at all about capital preservation, then a healthy dose of skepticism and paranoia can be helpful.1

Central banks seek inflation inflection

The Federal Reserve and the ECB certainly continue to have a healthy amount of paranoia about whether inflation will quickly return to target, and it was reinforced by the slight upside surprise in the month-on-month change in core CPI for August2 released on September 13. In an interview on the sidelines of the Kansas City Fed’s annual Jackson Hole Symposium, Chicago Fed President Austan Goolsbee said, “All this discussion about, ‘Oh maybe we should change the (inflation) target and declare victory,’ … you can’t do that until you’ve hit the target.” And so it seems likely that predictions by economists like Olivier Blanchard and others that the Fed will, de facto, increase its target from (a mostly arbitrary) 2% to (an arbitrarily somewhat higher) 3%, have fallen on deaf ears. What’s more likely is that central bankers have actually heard these prognostications and are stubbornly pushing back against them.

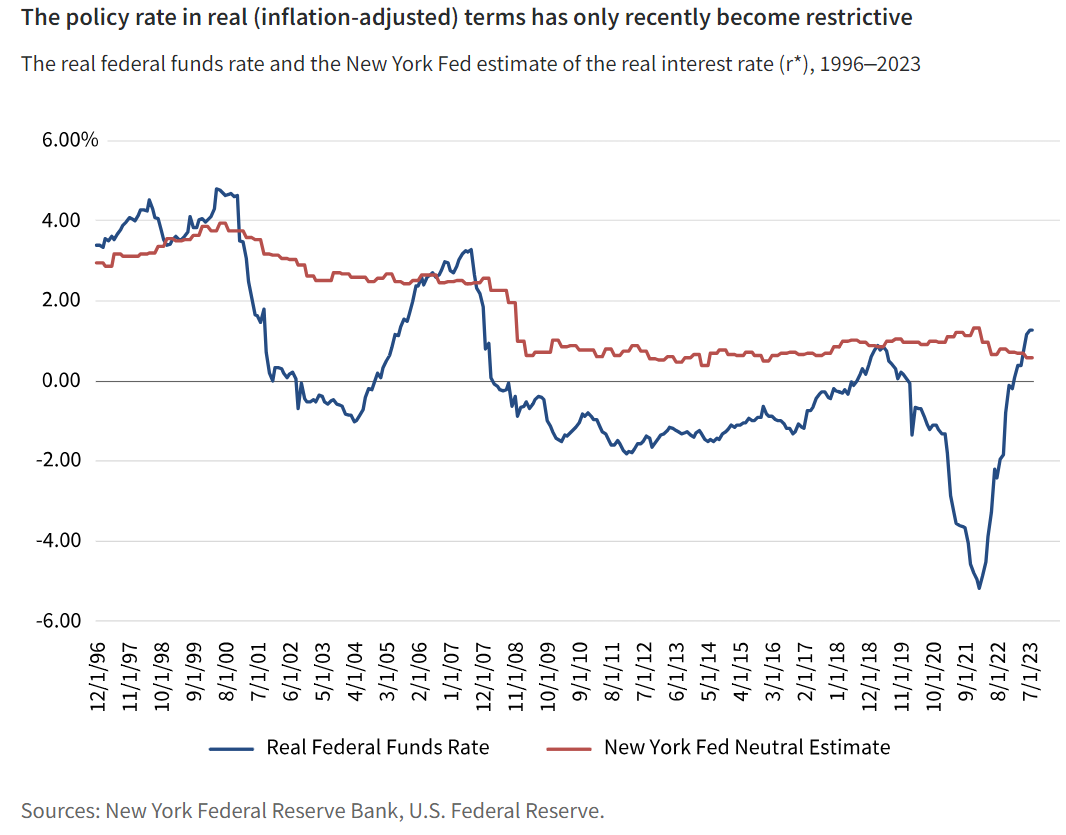

Rates are tightening for real

Regardless of whether the Fed and the ECB choose to increase the policy rate again or are, in fact, finished with this tightening cycle, “it’s a real rate that will matter,” as Powell pointed out in his September press conference. Given that the real rate is a nominal rate less inflation, it can change as inflation moves, without any change in the nominal level. Therefore, if inflation continues to decline into 2024, monetary policy will continue passively tightening if central banks choose to do nothing.

We have written before about the so-called natural (or neutral) rate of interest — what policymakers sometimes refer to as “r*.” It is an unknowable, theoretical interest rate that is neither expansionary nor contractionary to economic growth. There is an entire body of academic literature dedicated to figuring out how to best measure r*. Perhaps one of the best-known estimates is produced by the New York Fed based on the research of Kathryn Holston, Thomas Laubach, and John Williams. Interestingly, the current real federal funds policy rate (the federal funds target less core PCE) has only just moved into “restrictive” territory over the past few months. This metric now reflects the most restrictive monetary policy setting the U.S. economy has had since mid-2007.3

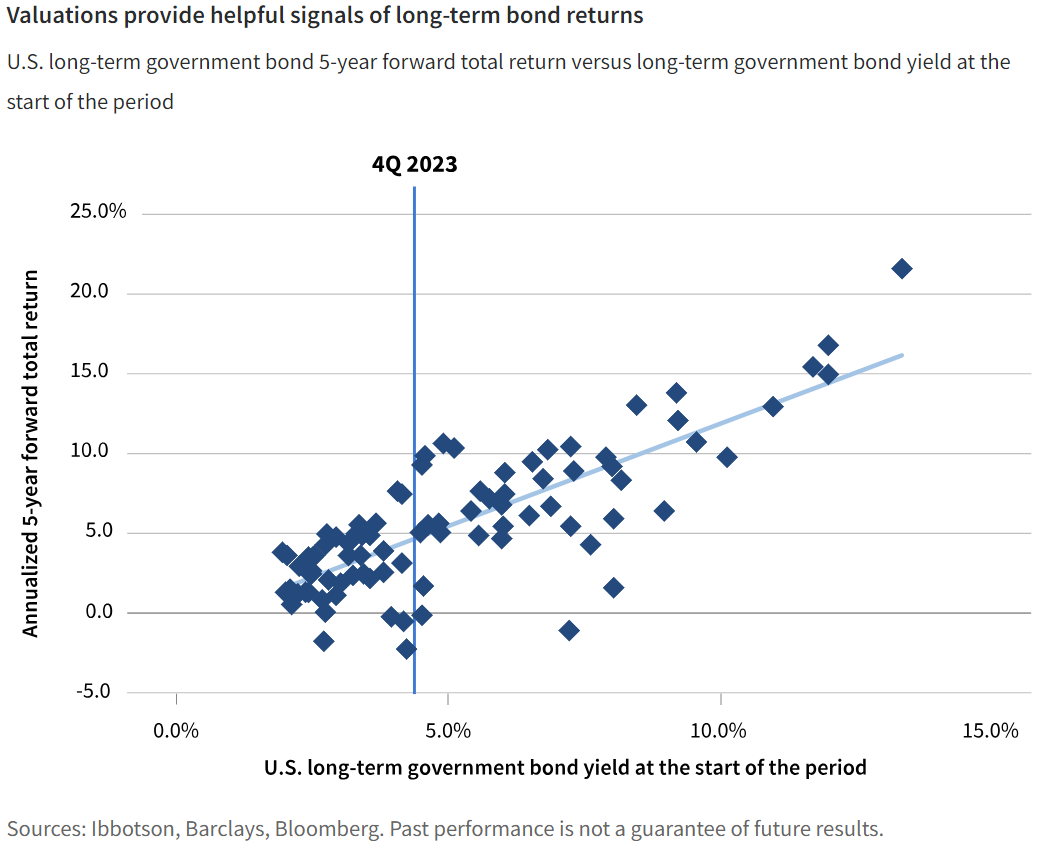

Government bonds compete with stocks again

And with central bankers coming out of the Jackson Hole Symposium seemingly optimistic about the prospects for an economic soft landing, 10-year Treasury yields are now back above levels not seen since the 2008 GFC.4 Higher nominal government bond yields are a compelling investment alternative in rapidly aging developed market economies, providing safe income in a world that had been starved of it for so long. Also, for the first time in almost two decades, Treasury yields are actually higher than the combined dividend-plus-buyback yield available in the equity market. The Fed continues to have the luxury of behaving as though only one part of its mandate matters, but we may not be far from the first negative payroll print, which will again force the Fed to choose its priorities. In that environment, we believe that duration will once again act as a good hedge against economic slowdown, producing compelling yield and the possibility of price appreciation. We continue to advocate for lower exposure to risky assets in favor of the renewed diversification benefit of bonds.

1. After all, “Just because you’re paranoid doesn’t mean they aren’t after you.” Written by Joseph Heller in Catch-22, sung by Nirvana on “Nevermind.”

2. Of which Harvard economist Jason Furman (@jasonfurman) noted, “One month is noisy so would not read too much into it. BUT a lot of the previous reassurance was based on just two months of data. Which is also noisy.” Twitter, September 13, 2023.

3. And nobody reading this needs a reminder about what came afterward.

4. Core European bond yields are also now at the highest levels since the European sovereign credit crisis, culminating with Mario Draghi’s 2012 “whatever it takes” speech.

This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon as research or investment advice regarding any strategy or security in particular.

This material is prepared for use by institutional investors and investment professionals and is provided for limited purposes. This material is a general communication being provided for informational and educational purposes only. It is not designed to be investment advice or a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. The opinions expressed in this material represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the material. Predictions, opinions, and other information contained in this material are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

This material or any portion hereof may not be reprinted, sold, or redistributed in whole or in part without the express written consent of Putnam Investments. The information provided relates to Putnam Investments and its affiliates, which include The Putnam Advisory Company, LLC and Putnam Investments Limited®.

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund's bond investments are likely to fall if interest rates rise.

Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions.

Our investment techniques, analyses, and judgments may not produce the outcome we intend. The investments we select for the fund may not perform as well as other securities that we do not select for the fund. We, or the fund's other service providers, may experience disruptions or operating errors that could have a negative effect on the fund. You can lose money by investing in a mutual fund.

In the United States, mutual funds are distributed by Putnam Retail Management.

Putnam Retail Management

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Putnam

Read more commentaries by Putnam