- Many emerging markets outside of China offer attractive opportunities.

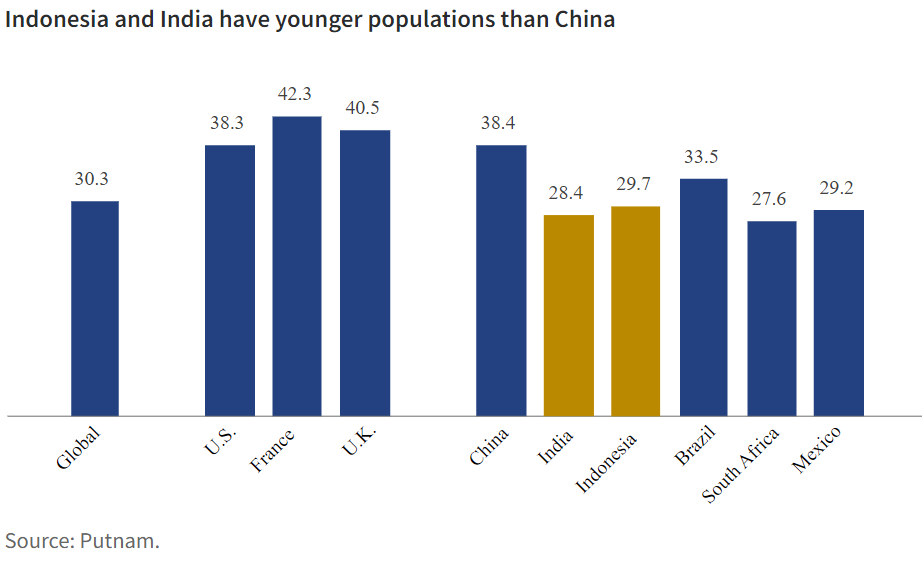

- We see promising potential in countries with younger populations and forward-looking policies, such as India, Indonesia, and Mexico.

- In the post-pandemic global economy, reshoring is changing the relative advantages of markets.

- Learn more about investment opportunities in emerging markets outside China by exploring our ETF.

Emerging market equities offer a wide variety of exciting investment opportunities, but many of these are often overshadowed by the dominance of China both in terms of index weight and investors’ mindshare. We believe an ex-China strategy could be a valuable addition to investor portfolios for a number of reasons. The benefits include a potentially more attractive performance profile, greater diversification benefits, and the ability to focus on some of the more exciting companies, countries, and themes in emerging markets for benchmark-aware strategies.

China stocks dominate the EM index

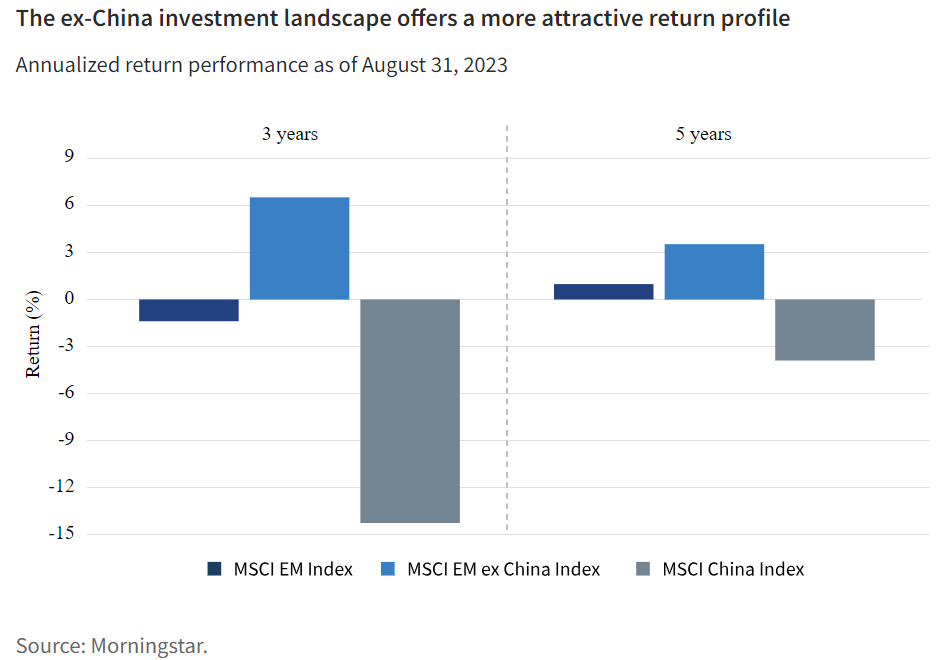

Historically, China has been a performance headwind and a geopolitical risk driver. Over the trailing three- and five-year periods, the MSCI China Index has seen negative absolute returns, weighing on results for the MSCI Emerging Market Index. We also believe ongoing tensions both within China and on the global stage could continue to cause concern among investors and serve as an overhang on Chinese stocks.

Unsurprisingly, China is the largest country in the MSCI Emerging Market Index. Since year-end 2014, China’s weight in the MSCI Emerging Market Index has grown by almost a third, rising from a 22% weight to a 30% weight. Today, China has 748 stocks in the MSCI Emerging Market Index, which accounts for roughly 52% of the total number of index constituents (1,421 stocks total as of August 31, 2023).

China’s index share was boosted by the 2018 inclusion of a small portion of the A share market, which represents publicly listed shares of mainland Chinese companies trading on two exchanges — the Shanghai Stock Exchange and the Shenzhen Stock Exchange. While the original inclusion of A shares brought the weight to 5%, our base case is that inclusion continues to grow over time. Based on an MSCI hypothetical projection published in 2018, 100% inclusion would have brought China’s total weight to over 40% of the MSCI Emerging Market Index. In short, we believe the emerging market index has become a “China+” index at the expense of exposure to the more dynamic and faster-growing economies of the developing world.

Outside China, many emerging markets offer more attractive potential

As the risks of excessive exposure to China become better understood, we believe there are numerous beneficiaries across emerging markets that could offer investors more exciting growth prospects. We are particularly excited about the setup in India. Despite the potential for a global slowdown, our outlook for the Indian economy is promising. Various indicators suggest domestic economic activity is accelerating, as tax collections are up over 20% and manufacturing PMI remains at expansionary levels. Overall, India’s GDP growth is expected to be 6% or more over the course of this year, and inflation is moderating to around 5%.

Another country we believe warrants a closer look by investors is Indonesia. We believe attractive demographics (a young and growing population), high consumer confidence, and a stable, forward-thinking political setup could help drive growth. Furthermore, Indonesia is a key source of the base metal nickel. However, rather than simply exporting this commodity, the government is focused on incentivizing companies to become global players in growth areas that depend on nickel, such as the EV battery supply chain.

A young population can help accelerate economic growth. It can mean a larger labor supply and a workforce that is more willing to adopt new technologies, in traditional industries like information technology, and also in newer areas such as fintech and sustainability. This can increase productivity at the individual level and drive innovation and meaningful economic growth at the national level. Furthermore, younger workers are typically just beginning their wealth gathering, which can lead to attractive levels of savings growth as well as increased consumption. This can all exist along with a lower drag on government systems in the form of health care needs and government-provided financial support. Younger populations can contribute meaningfully while asking very little in the form of subsidies or government care.

Supply chain diversification and reshoring change investment opportunities

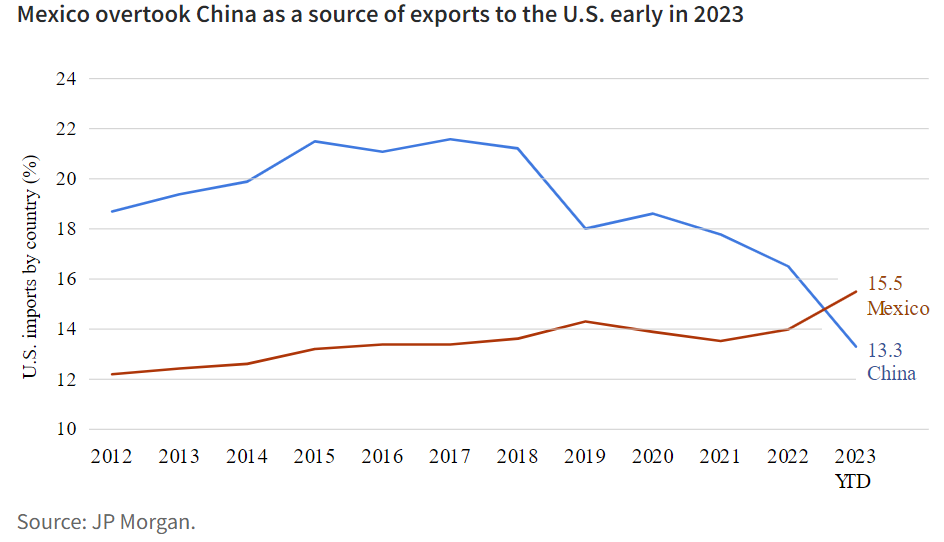

A trend that we believe could have a meaningful impact on emerging markets beyond China is reshoring. Deglobalization is gaining steam in the wake of Covid-related supply chain issues and ongoing geopolitical tensions. As many companies look to diversify away from China, we are looking to countries we think could benefit from increased trade opportunities. Mexico, a strong equity performer this year, has seen strong share gains in U.S. imports, while China has seen notable losses. Also, manufacturing as a percentage of GDP is trending up, and Mexico has generally seen tightening in labor markets and wage growth. We believe Mexican equities are still relatively undervalued and offer potential for rerating given the exciting company-specific fundamental growth stories and the stabilizing macroeconomic environment.

Ultimately, we believe investing in emerging markets ex-China offers investors the potential for attractive returns, diversification, and exposure to some of the faster-growing themes in this universe. This may be an attractive investment option for those seeking compelling long-term growth opportunities without the risks associated with meaningful investment in China.

Learn more about investment opportunities in emerging markets outside China by exploring our ETF.

335137 10/23

Putnam ETFs are distributed by Foreside Fund Services, LLC. Foreside is not affiliated with Putnam Investments.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. Gross total return (GD) indexes reinvest as much as possible of a company’s dividend distributions. The MSCI Emerging Markets ex-China Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets excluding China. The MSCI China Index is an unmanaged index of Chinese equity securities. You cannot invest directly in an index.

Certain information contained herein (the “Information”) is sourced from/copyright of MSCI Inc., MSCI ESG Research LLC, or their affiliates (“MSCI”), or information providers (together the “MSCI Parties”) and may have been used to calculate scores, signals, or other indicators. The Information is for internal use only and may not be reproduced or disseminated in whole or part without prior written permission. The Information may not be used for, nor does it constitute, an offer to buy or sell, or a promotion or recommendation of, any security, financial instrument or product, trading strategy, or index, nor should it be taken as an indication or guarantee of any future performance. Some funds may be based on or linked to MSCI indexes, and MSCI may be compensated based on the fund’s assets under management or other measures. MSCI has established an information barrier between index research and certain Information. None of the Information in and of itself can be used to determine which securities to buy or sell or when to buy or sell them. The Information is provided “as is” and the user assumes the entire risk of any use it may make or permit to be made of the Information. No MSCI Party warrants or guarantees the originality, accuracy, and/or completeness of the Information, and each expressly disclaims all express or implied warranties. No MSCI Party shall have any liability for any errors or omissions in connection with any Information herein, or any liability for any direct, indirect, special, punitive, consequential, or any other damages (including lost profits) even if notified of the possibility of such damages.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Putnam

Read more commentaries by Putnam