The Bank of England (BoE) has been climbing a metaphorical mountain since 2021 in an effort to tame inflation. But the central bank surprised markets by pausing its rate hike cycle last week.

The decision was a close call with a single vote separating a pause from another hike. The better-than-expected August U.K. inflation report, especially the improvement in the services component, was pivotal. But a number of recent economic readings also factored into the narrow decision. U.K. July gross domestic product surprised to the downside, contracting 0.6% month over month, with a broad-based decline in output across major sectors. The British unemployment rate has risen to 4.3%, the highest since September 2021. Business insolvencies have neared the peak they touched during the global financial crisis of 2008.

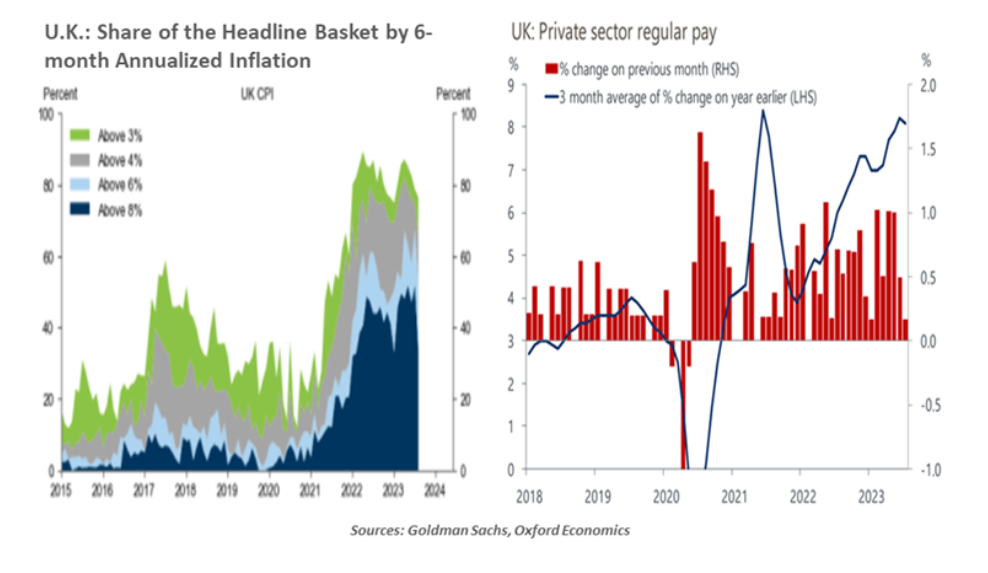

On the other hand, inflationary pressures remained broadest in the U.K. with 65% of the headline consumer price basket running above 4% annualized in the past six months. Higher unemployment has not had any impact on wages, with the latter now growing faster than inflation. Regular pay (ex-bonuses) was up 7.8% year over year in the three months to July, the highest annual growth rate since 2001.

The main transmission channel from higher policy rates to consumers is mortgage rates. While the mortgage crunch is substantial, the share of British households exposed to rising mortgage costs has declined markedly from 43% in 1991 to below 30% in 2022. Many mortgage rates are fixed, typically for two to five years, further delaying the impact of raising rates. While the value of mortgage arrears is rising, which would lead to more defaults, the number unable to repay remains relatively low.

To use BoE Chief Economist Huw Pill's metaphorical reference, the central bank is not yet on the top of Table Mountain, nor will it go down Switzerland’s steep Matterhorn. The BoE’s pause at base camp is just a brief stop on its way to the summit.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust