Rocking with RAFI: International Evidence

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Points

-

Inherently tilted toward value, the Research Affiliates Fundamental Index™ (RAFI™) weights constituents based on their economic significance and captures rebalancing alpha by contra-trading against cap-weighted indices’ largest holdings.

-

With negligible incremental risk, a RAFI Global Index hypothetically outperformed a Cap-Weighted Global Index by 40 bps per annum and a Cap-Weighted Global Value Index by 2.2% from 2007 to 2022—a 16-year period covering the long value rout and its aftermath.

-

From 2007 to 2022, RAFI outperformed cap-weighted Broad and Value indices in Emerging as well as Developed ex US markets.

-

In the 2010s, value stocks crashed, relative to growth stocks and to the broad cap-weighted market, but value companies continued to pay out dividends.

When we launched RAFI (Research Affiliates Fundamental Index) in 2004, we knew the strategy had the potential to upend the way investors thought about index funds. From the early days of RAFI, some competitors attacked us for having the audacity to suggest that RAFI is a better index, calling it a clever repackaging of a value strategy. True, in part: RAFI has a stark value tilt, which is an exact mirror-image of the cap-weighted market’s willingness to pay a premium for perceived growth opportunities.

In those same early days, however, many recognized that the Fundamental Index approach offered investors the ability to capture rebalancing alpha by contra trading against a cap-weighted index’s biggest bets. Case in point: in 2007, Towers Watson coined the term smart beta, inspired by RAFI, to cover indices that did not link a stock’s price or market cap to its portfolio weight, and therefore enjoyed a rebalancing alpha. The performance of the Fundamental Index was attracting attention and investors.

In our recent article “RAFI Rocks!! Taking Smart Beta Back to Basics,” we look at RAFI’s live performance in the US market over the last 18 years. We show that over its history the Fundamental Index arguably remains the smartest smart beta strategy in the market, beating not only cap-weighted indices but also value indices. As a nod to the critics who said, “it’s just value,” we compared results to value indices; some of these same critics promptly took issue with that comparison. C’mon!! You can’t have it both ways! And, relative to value, the alpha is relentless. Where else can we find t-Statistics (on live index results, not on backtests or simulations!) of 4, 5, even 6?!?

In this article, we extend our analysis to the international markets, both developed and emerging. The strategy was invented in the US, on US data. These international results can be correctly viewed as out-of-sample tests (albeit correlated with US returns), as can the results since 2005 (after the invention of the concept). First, however, we look at the fundamental insights that undergird the success of RAFI, and importantly, where it converges with mainline understandings of value, and where it breaks new ground. After highlighting this international debut of RAFI—intellectually speaking—we take a fresh examination of what really happened to value during its hibernation. The underlying bricks and mortar of value companies remained strong, but the market’s ability to price these fundamentals broke down in spectacular fashion. Brought together, these individual plotlines underscore the unique role of, and continuing need for, RAFI—the overnight revolution nearly 20 years in the making.

Origins of RAFI

Before we look at “the how” of RAFI’s performance around the world, let’s review briefly “the why.” What inspired the strategy in the early 2000s and keeps it delivering for investors today?

Just as the Research Affiliates team approaches today’s investing challenges, we began 20 years ago by asking a few critical questions: Why should we want to commit more money to a stock after it has doubled in price than before it doubled? That doesn’t make a lot of sense. Why, then, would we choose to invest for the long term in a market-cap-weighted index strategy, an index that overweights the most popular, frothy, high-flier stocks and underweights unloved deep-value stocks? Could we create an alternative index, one that would be more reflective of composition of the macro-economy? Why not weight index constituents based on the fundamental size of a company’s economic footprint?

“Why should we want to commit more money to a stock after it has doubled in price?”

Our first test of this approach in 2003 was a sales-weighted index. We selected the 500 largest stocks by sales and weighted them by sales. The strategy outperformed the S&P 500 Index by 2.5% a year over our 30-year sample period that began in 1973. Our next test was an index that followed the same approach but used book value. We then tested the five-year averages of company profits and dividends, and even the number of employees. Each fundamental measure we tried generated about the same results—roughly an annualized 2% value-add over the 30 years.

That was our first “aha” moment: fundamental weighting, regardless of which fundamental metric we used, could produce value-add by breaking the link between the weight of a stock in the index portfolio and the price of that stock. If a stock’s price doubles and the underlying fundamentals do not, the strategy trims the holding. If a stock’s price tanks and its fundamentals do not, the strategy tops up the holding. These findings led to our design for RAFI, which uses a rules-based fundamental-weighting approach of four measures of company size—sales, cash flow, dividends, and book value—for security selection and rebalancing. Further extensions of this research led to the launch of our first Fundamental Index strategies in late-2004, and our 2005 FAJ article introducing the concept.2 By contra-trading against the market's biggest bets, the strategy captures a rebalancing alpha; in our view, this is a reliable source of alpha – a view that remains controversial to this day.

“The alpha engine is nothing more than rebalancing.”

Ironically, the source of the alpha has nothing to do with company fundamentals. The alpha engine is nothing more than rebalancing, as documented by Jack Treynor in his 2005 FAJ paper, “Why Market-Valuation-Indifferent Indexing Works.”3 If share price equals fair value, plus or minus a mean-reverting error, that mean-reverting error pulls down the return for any strategy that anchors on market cap or share price. Any strategy that is “valuation-indifferent” will recapture this performance drag. Random weighting, equal weighting, optimization-based strategies (if they do not anchor on market capitalization and do not constrain tracking error), and even throwing darts at the Wall Street Journal, all work nearly as well, for the same reason (albeit with large factor bets, that provide their own alpha, positive or negative) as detailed in Arnott et al. (2013).4

When the team at Watson Wyatt realized that a rebalancing alpha was the profit engine for RAFI, they coined the term “Smart Beta” to embrace any strategy that will by design capture this rebalancing alpha. That term has fallen out of favor, arguably because it was embraced by much of the asset management industry, including the factor investing community, and attached to a whole array of strategies that lacked that essential rebalancing alpha. As the term was applied to a host of ideas, both smart and dumb, with no common denominator other than their formulaic construction, it lost its relevance.

We believed then, and we believe now, that we succeeded in our goal of building a better index. RAFI’s performance speaks for itself, in the US market and in international markets. We show in “RAFI Rocks!! Taking Smart Beta Back to Basics” that RAFI US handily outpaced both the Russell 1000 and Russell 1000 Value indices over the 35-year period from 1988 through 2022. Specifically, based on an initial $100 investment, an investor in RAFI would have finished 62% wealthier ($5,500 versus $3,400) than an investor in the Russell 1000 Index and 81% wealthier ($5,500 versus $3,000) than an investor in the Russell 1000 Value Index.5

A fundamental weighting approach also creates an inevitable and substantial value tilt because growth stocks in the index are reweighted down to their economic footprint, while value stocks are reweighted up to their economic footprint. Unlike the value indices, RAFI includes all the growth stocks (provided their actual book of business is large enough to matter). Unlike the cap-weighted value indices, RAFI upweights the deepest value names far more than the mildest value names. The former diminish the value tilt, while the latter increases it. On average, they roughly cancel, creating a value tilt every bit as substantial as the cap-weighted value indices. But, with RAFI, that value tilt is dynamic. When the market pays a modest premium for growth, we have a modest value tilt; when the market pays a huge premium for growth (as it does today!), RAFI has a deeper value tilt than the value indices.

RAFI’s International Record

Let’s look out of sample (both geographically, by looking at non-US results, and across time, by looking at results after the strategies went live). The RAFI strategy has been live in international portfolios since June 2005 and in emerging markets portfolios since June 2006. For consistency, we will start our analysis in 2007, by which time there were live RAFI strategies in the US, Developed ex-US, Japan, UK, and Emerging Markets. Do the non-US results support the US results? Indeed they do.

Throughout this paper, we define “RAFI” as an equally weighted blend of the FTSE-RAFI, Russell-RAFI and RAFI Fundamental products, which date back to 2005, 2011 and 2019, respectively. We compare RAFI with the corresponding passive cap-weighted (hereafter, “CW”) benchmark, both broad market and value. For these CW benchmarks, we equally weight the relevant FTSE and MSCI indices. We blend these indices (FTSE-RAFI and Russell-RAFI, or FTSE and MSCI) to avoid cherry-picking, and in recognition that both RAFI and CW investors have alternative choices at their disposal. The blend makes a negligible difference, compared with using the individual indices.

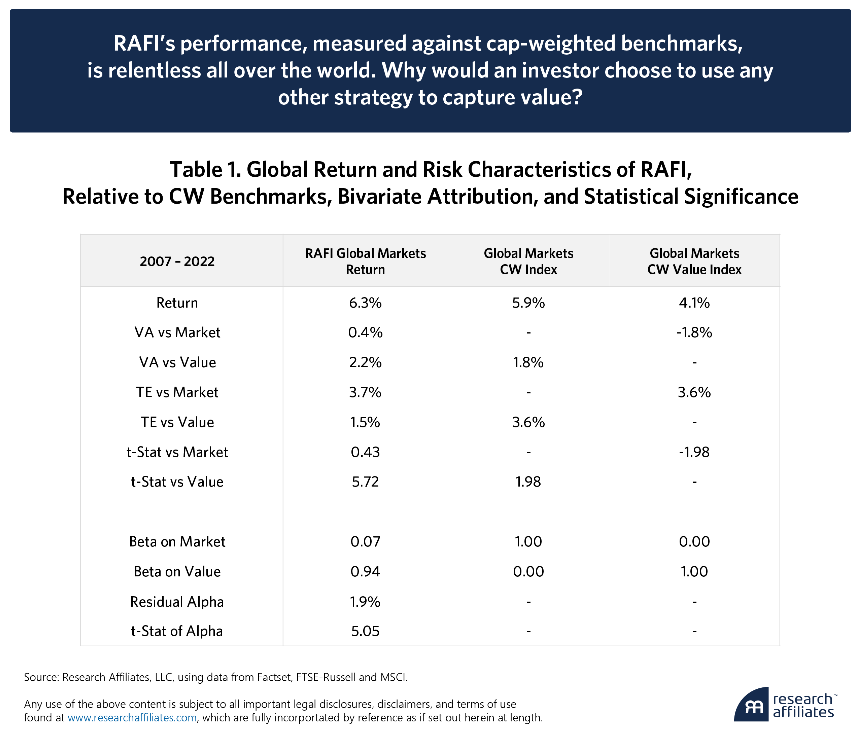

When we compare RAFI Global (a blend of FTSE-RAFI, Russell-RAFI and RAFI Fundamental) with the CW Global Index and the CW Global Value Index (using the average of MSCI ACWI and FTSE All-World indices), we find the same consistent outperformance that RAFI demonstrated in the US market. When we compare the RAFI Global Index -with the Cap-Weighted Global benchmarks (a blend of FTSE All World and MSCI ACWI), in Table 1, the return beats the CW market, even during a span when CW Global Value lagged the broad market by 178 basis points (bps) per annum. RAFI’s structural value tilt is self-evident in its tracking error (relative to Global CW, the tracking error is 3.7%, while relative to Global CW Value, its tracking error is a scant 1.5%); adding 2.2% in incremental performance with only 1.5% tracking error is massively significant. Also, note that its bivariate attribution supports the fact that RAFI is roughly as value-tilted as the CW Value indices (RAFI’s beta on Value is 0.94, while against the global market its beta is 0.07).

When we drill down to individual regions in Appendix 1, we find a similar picture, whether we’re looking at developed or emerging markets, or at the US or developed ex-US. These relative gains in performance are earned with negligible incremental risk. Note that the market beta and the value beta sum to barely above 1.00 in all cases, and the residual risk (which cannot exceed the lesser of RAFI’s tracking error relative to the market or relative to value) is around 1.5% to 2.9%.

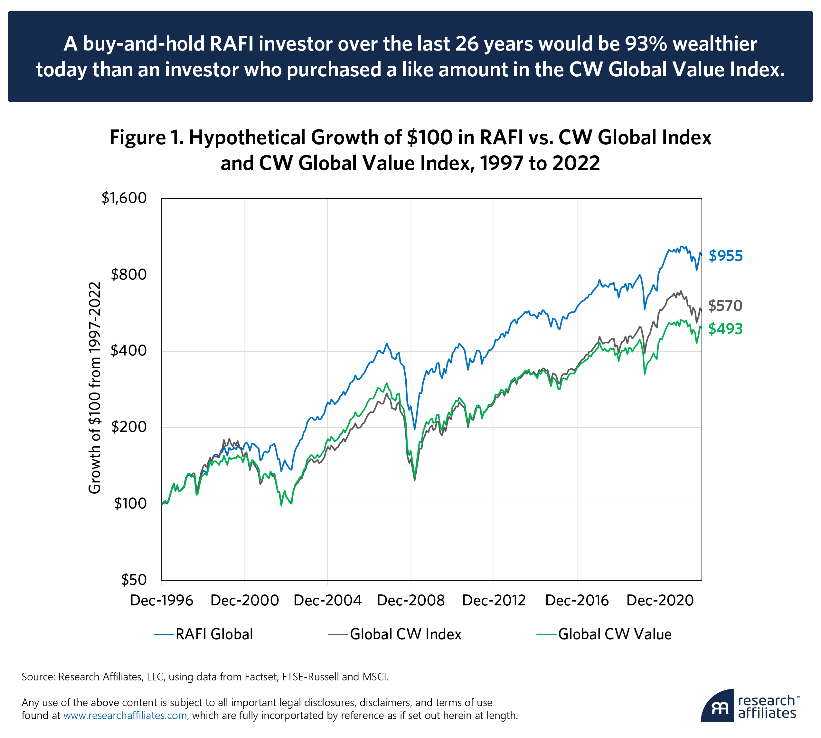

Granting that RAFI was not yet a live strategy in the early years of the following chart, let’s look back a bit further. In Figure 1, we compare how a hypothetical RAFI Global investor would fare versus investors in each of the two CW Global Indices (broad market and value) over the 26 years from 1997 through 2022. We can’t go back further because All-World and EM value begin in 1997.

-

Assuming dividends were reinvested and no fees, trading costs, or taxes were incurred during the holding period, a $100 investment in the global stock market at year-end 1996 (the CW Global Index, a solid gray line) would have grown to $570 by year-end 2022.

-

For value, it was a tumultuous quarter-century, with global value severely underperforming during the dot-com bubble, winning handily over the next seven years, giving it all back during the 13½-year value rout ending August 2020, and finally recouping much of the loss by the end of 2022. At the end of this roller-coaster ride, a $100 investment in the CW Global Value Index at year-end 1996 (solid green line) would have lagged the broad market, growing from $100 to $493.

-

Meanwhile, an investor in RAFI over the same 26-year span would have seen their $100 investment grow to $955 (solid blue line).

The main hurdles in RAFI’s performance versus the broad index were the value meltdowns in the late 1990s during the dot.com bubble and the value crash from 2017 through August 2020. The strategy’s dynamic value tilt was no match for frothy growth-dominated bull markets. Nonetheless, RAFI handily outpaced CW Global Value during each of the major moves in value, relative to the broad market, over the 26 years.

Appendix 2 shows similar graphic comparisons, and Appendix 3 shows summary statistics for Developed and Emerging Markets and for the US and Developed ex-US. Note that for the US CW benchmarks we used Russell and S&P indices, rather than FTSE and MSCI indices. Appendix 3 also shows an attribution of returns into dividend income, growth in income and changes in valuation multiples (in this case, changes in the dividend yield). We will discuss this attribution shortly.

Rolling through the Value Rout

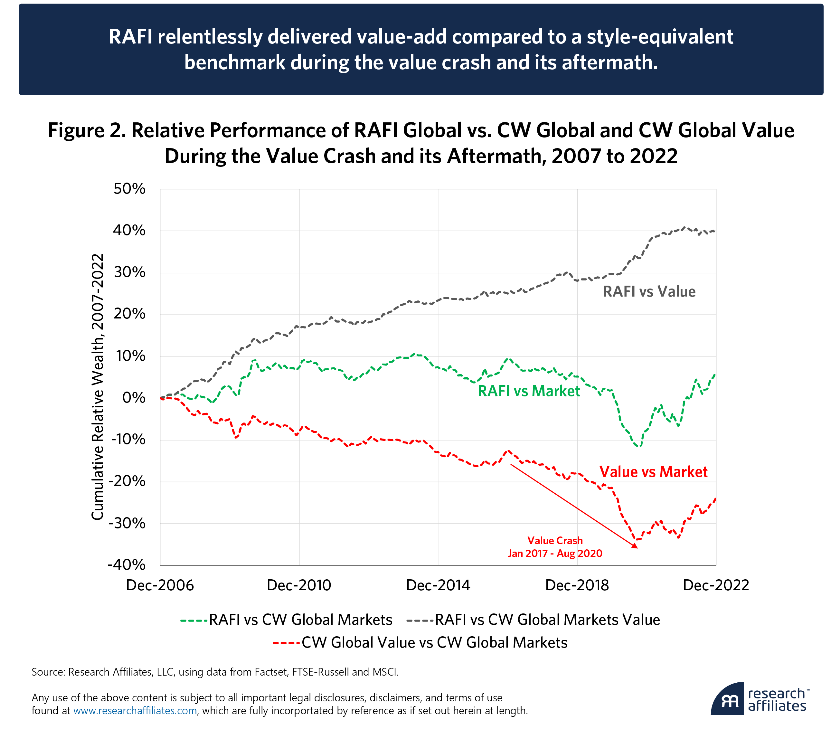

Let’s look more closely at how the indices behaved during the long dry spell for value from 2007 to mid-2020 and during the value rebound that followed in 2021 and 2022. Figure 2 drills down to the 16-year span from 2007-2022, which spans the 13½ year value rout and its subsequent rebound. In Global markets, Developed markets, and the non-US developed markets, the value meltdown was much the same as in the US market. The rout began early in 2007 and continued into August 2020, and was the granddaddy of all value meltdowns.6 Regardless of whether we use the classic Fama–French definition of value (which is based solely on price to book value), or a more nuanced multivariate comparison, value peaked in March 2007 and didn’t hit bottom until August 2020—an absolute horror show for value investors.7

Here, we examine the relative performance between RAFI Global, CW Global and CW Global Value. The performance of RAFI versus the broad CW Global market closely mirrors the ups and downs of CW Value versus the broad market. But RAFI relative to CW Value exhibits a relentless alpha (green dashed line). The RAFI investor finishes this 16-year period with nearly 40% more wealth than the CW Global Value investor (the black dashed line).

The rout was the granddaddy of all value meltdowns.

Not shown here (but easy to infer from Figure 1), for the full 26 year span the RAFI investor is 67% wealthier than an investor in the CW Global Index and 93% wealthier than an investor in the CW Global Value Index. This graph shows what a t-statistic of 5.7 looks like. Against CW Global Value, Global RAFI generally wins when value wins and when value loses, never underperforms over any rolling 24-month span, and has no drawdowns larger than 1.8%. While past is not prologue, and these live index results offer no assurance that an investor will have similar outcomes in the future, we personally find these track records very comforting.

As Figure 2 illustrates, the relative performance of RAFI versus the broad CW Global Index (the dashed green line) and the CW Global Value Index versus the broad market (dashed red line) moved up and down in lockstep, similar to the relationships in the US market. Over the 16-year period, however, the gap between the two lines grew steadily wider. RAFI’s value-add relative to the value index was nearly relentless.

From August 2020 through December 2022, RAFI’s global performance relative to the broad-market and value indices closely resembled its US performance in the late stages of the dot.com bubble from 1998 to early 2000. RAFI’s dynamic value tilt—adding greater value exposure as value stocks fall further out of favor—is the proximate cause of RAFI’s extraordinary gains relative to both the market and to value.8 Over the 16-month value rebound, RAFI Developed ex-US beat the CW Developed ex-US Value index (and the broad market) by roughly 2,000 bps, not unlike RAFI’s win in the US market after the dot.com bubble burst.

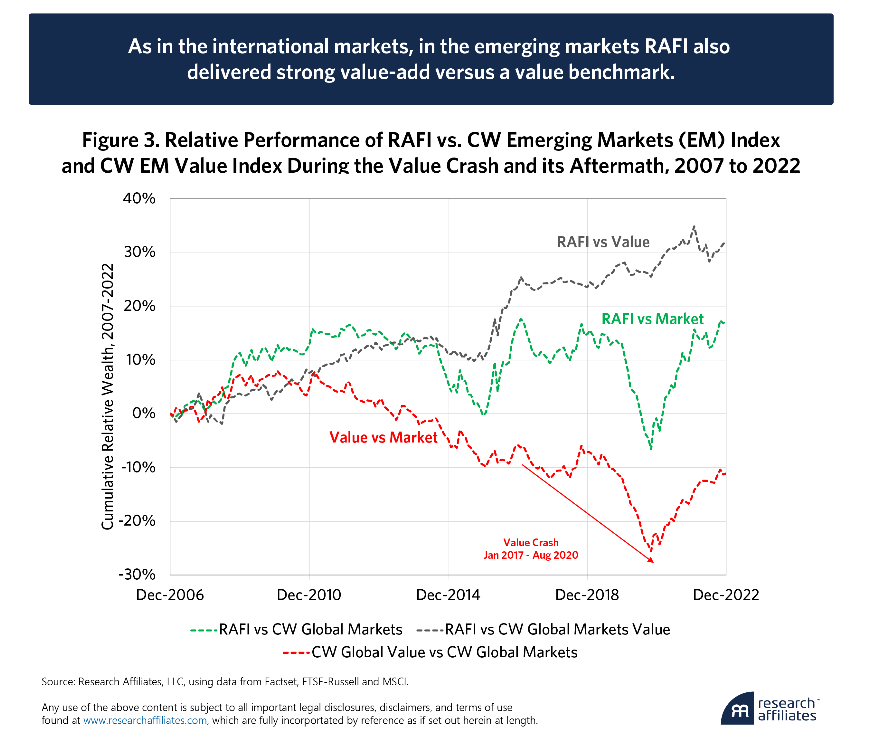

The history in the emerging markets "rhymes" with developed markets history, but with different timing. From 2007 to 2010, value continued to win in emerging markets, very handily in 2007 and 2008, but eking out only modest gains through 2010. As shown in Figure 3, RAFI beat conventional CW Value during these four years, most particularly as Emerging Markets began to crash in mid-2008, and in the tumultuous aftermath of 2009-10. The bear market in emerging markets value, relative to the broad CW emerging markets, didn’t begin until 2011, with the value crash in emerging markets reaching its crescendo in 2019 and 2020, ending in October, two months later than in the developed markets.

Appendix 4 shows similar comparisons for the US, Developed, and Developed ex-US markets. In all cases, the value added by RAFI and the value added by CW Value, both measured relative to the CW broad market, move in near-lockstep, with the result that RAFI beats CW Value with startling regularity.

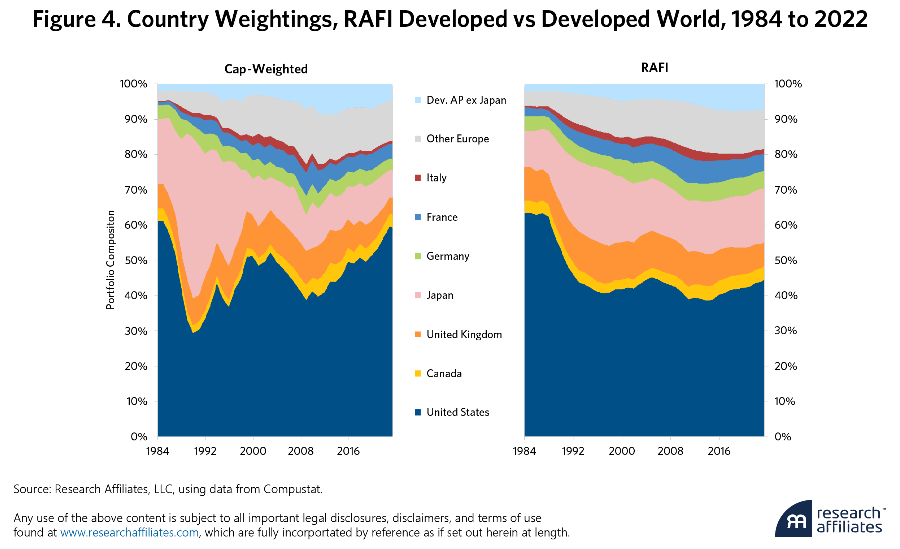

The Impact of Country Weights

For all the similarities between the relative performance of RAFI indices to cap weighted indices across regions, there is an additional element to consider when allocating to regions that encompass multiple countries. Just as the presence of multiple sectors within the US provides a rebalancing opportunity for RAFI, as it trims its exposure to portions of the economy whose price appreciation has recently outpaced business growth, so too does the presence of multiple countries present a rebalancing opportunity.

An investor in a cap-weighted global developed portfolio would have invested more than 45% of his equity exposure in Japan when prices of Japanese equities peaked in 1989. (Figure 4.) That weight to Japan proceeded to drop precipitously as the country’s companies fell out favor, bottoming below 8% in 2022. Conversely, Japan reached a maximum weight of 21% in a simulated RAFI index and never fell below a 10% weight. Anchoring on fundamental measures of size prevented the RAFI strategy from getting carried away with the exuberance with which the market embraced Japan during the Nikkei bubble, while also maintaining a slightly larger exposure when Japanese share prices hit their low relative to their developed markets counterparts.

A fun thought experiment, when looking at the above graphs, is to consider which seems to be the passive strategy. If they were not labeled, most would choose the graph on the right as the passive strategy. In the mid-1980s, the US was the dominant economic powerhouse, but Japan and the Asian Tigers were ascending. From that point forward, the relative dominance of major economic powers in the developed world was relatively steady. And yet, the graph on the left shows the markets’ constantly shifting expectations for future growth. Which investment strategy should fare better? A strategy with country allocations that peak, just as the relative performance peaks, as we see on the left, or country allocations that require us to trade when expectations diverge markedly from the current reality?

By 1989, Japan was expected to eclipse the US as an economic power, as evidenced by its cap-weight markedly exceeding the US, in the developed world index on the left. During the 1990s, Japan’s economic power (as evidenced by the fundamental size of Japan-based public companies, on the right) kept growing, while the markets’ expectations from that growth diminished, setting the stage for Japan’s three lost decades. As in Japan, the US share of the developed world stock market (on the left) seems to rise or fall a bit ahead of changes in the US economic footprint (on the right), but the relationship is weak, and the market seems always to substantially overestimate future good or bad news.

The Power of the Value Effect

As we observed in the US, value stocks all over the developed world underperformed horrifically from 2007 to 2020 (and in emerging markets from 2011 to 2020). But on the basis of their fundamentals—specifically their dividend distributions—portfolios of value companies did not. Investors expected the worst from value companies, and priced them accordingly, at ever-deeper discounts relative to the broad markets. But value indices soldiered on, delivering dividend growth roughly pari passu with the broad markets.

Robert Shiller won the Nobel Prize for his work showing that share prices are much more volatile than the underlying fundamentals of their respective companies. He suggested that this excess volatility, relative to the underlying fundamentals, was evidence of market inefficiency.9 This has direct relevance to the value crash of the 2010s. Value stocks crashed, all over the world, relative to growth and relative to the broad CW markets, but value companies did not. A rarely-discussed implication of this divergence between value stocks and value companies is the persistence of a “value effect,” even when value stocks were struggling. The value crash, all over the world, was wholly a consequence of a downward revaluation in value stocks, measured relative to their underlying fundamentals. Their fundamentals were doing just fine!10

History shows that value stocks’ dividends track those of the constituent stocks in broad market indices. When the dividends of one group falter, as they did during the global financial crisis, European/EM debt crisis of 2011, and the Covid crash, the dividends of the others follow suit. The dividend income of value stocks may be slightly more vulnerable to financial crises than the income of growth stocks, but not in a single instance since 1985 did value stocks’ income weaken enough to justify the relative performance routs they faced.

It bears mention that the dividends of value stocks do, as expected, grow more slowly than the dividends of growth stocks. Fama and French (2007) coined the term “migration” to describe a mechanism by which portfolios of value stocks deliver dividend growth similar to (and often faster than) portfolios of growth stocks. With each annual rebalance, growth stocks drop out of the growth index when their valuation multiples fall too far. These low-PB or low-PE stocks are replaced with new high-fliers, which reduces the book value or earnings base of the growth portfolio. The opposite happens with the value portfolio, with some stocks regaining favor in the market and trading at higher PB or PE ratios, and no longer qualifying for the value portfolio.11 These are replaced with new unloved stocks at depressed valuation multiples. This means that the PB or PE ratio falls, hence the underlying book value or earnings will rise, with each and every rebalance.

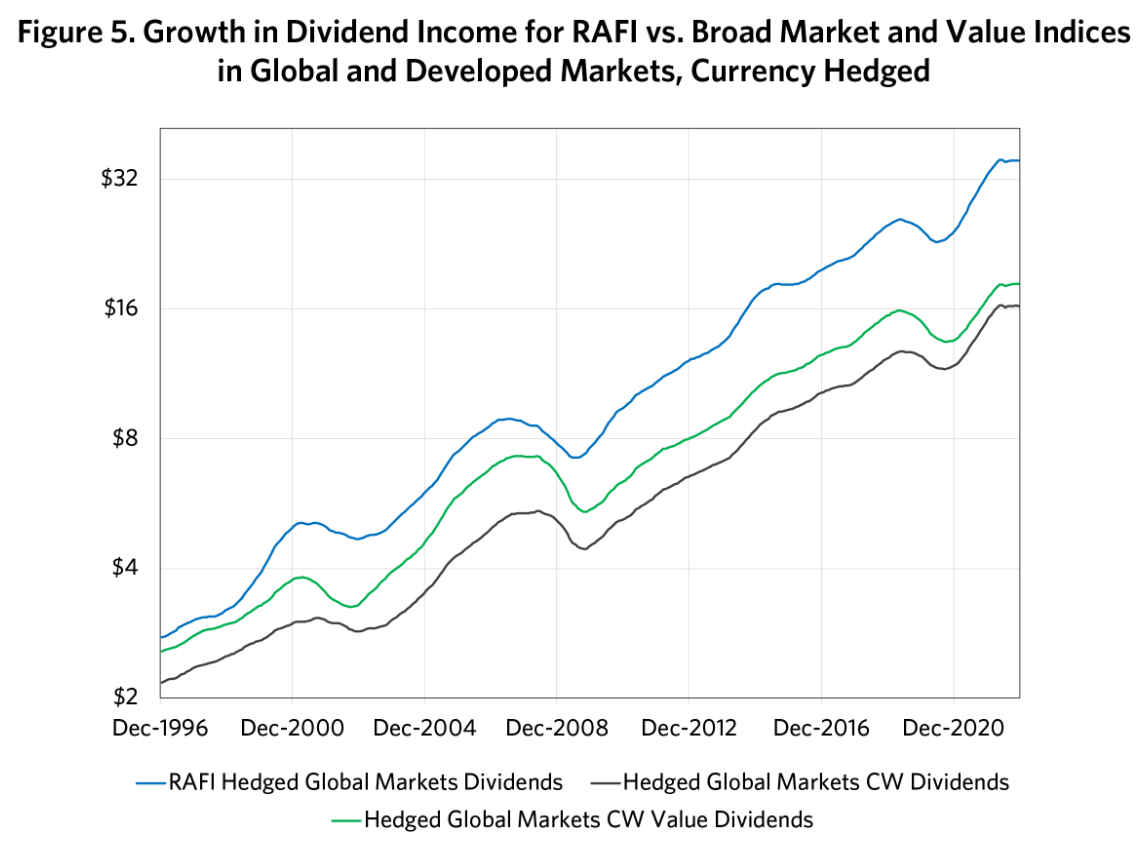

Suppose an investor put $100 into the CW Global index at the end of 1996. With a yield of 2.02%, the investor would have garnered a modest $2.13 income stream. With income reinvested (and no taxes, trading costs, or spending to interfere with the compounding), that $2.13 dividend income would have grown, in currency-hedged terms, to $13.51 by the end of 2022. From equivalent starting points, dividends for the CW Global Value Index started at $2.39 and ended at $15.01. So much for the growth portfolio making up for a lower yield by delivering faster growth. Meanwhile, RAFI’s annual dividend income grew from $2.58 to $28.98, more than double that of the CW Global index.

The value investor sees an 18% higher income stream taper to a 12% premium after 26 years. That’s a long time for the growth investor to settle for less income in hope of faster growth! Meanwhile, the RAFI investor’s 27% income premium soars to a 118% premium in just 26 years. The growth records for US, Developed ex-US, and Emerging markets show a similar pattern in Appendix 5.

A simplistic worldview might suggest that the higher yield of a value portfolio and of RAFI is a tradeoff for less growth in dividends (and earnings, sales, etc.) compared with a more rapid rise in income for the growth investor. Absent the Fama-French migration effect, this is correct. Once migration bolsters the dividend income growth of a value portfolio, and impedes the income growth of a growth portfolio, this differential disappears. The value portfolio trades newly-lower-yielding stocks that no longer qualify for the value portfolio, in exchange for newly-high-yielding deep value stocks. The rebalancing alpha of RAFI is nothing more than this same Fama-French “migration” effect on steroids: while the value portfolio rebalances at the margin, with stocks added or dropped from the index, RAFI rebalances the entire portfolio, to a higher yield (and lower PE, PB and PS ratios) with every rebalance!

Suppose the relative cheapness of value stocks compared to the market—the essential reason for the higher yield on value stocks—were stable over time. In that case, the relative performance graphs for the RAFI and CW indices would—by mathematical identity—track the oh-so-steady spread between the dividend income lines plotted in the charts of Figure 5. The differences in the growth of dividend income would hardly justify the volatility we observe in the relative performance between growth and value, or between value and RAFI indices. A logical conclusion, then, is that the volatility in the excess return of value stocks relative to the broad market (which is of course strongly driven by high-flying growth stocks) is a consequence of constantly changing consensus market expectations regarding the future prospects for value companies relative to the broad market, with no empirical support for these fast-changing expectations.

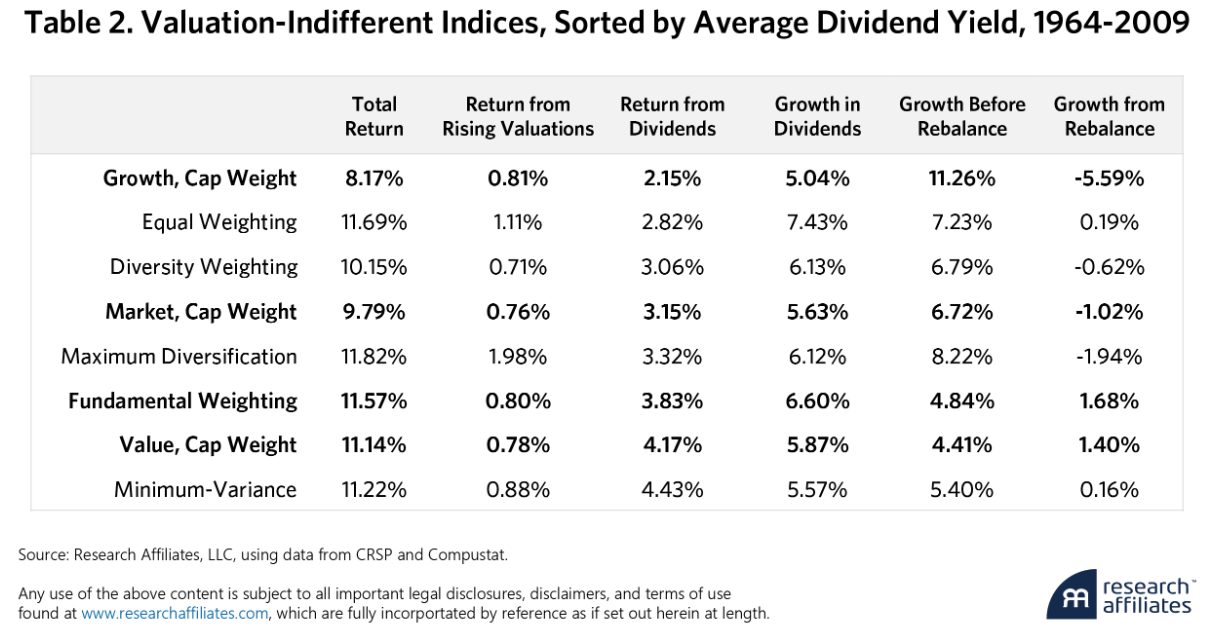

We explored this phenomenon in a 2012 paper in the Journal of Portfolio Management, which concludes with the exhibit reproduced here as Table 2. In it, we can see that CW Growth enjoyed annual dividend growth of 11.26% from 1964 through 2009, but lost 5.59% from migration, for a net growth from dividends of 5.04%.12 Over that same span, CW Value sees an anemic 4.41% growth in dividend income, plus 1.40% from migration, leading to the “paradox” of faster dividend growth, at 5.87%, than the CW Growth portfolio. Add in the 2% higher dividend yield, and we find nearly a 3% higher total return. “Fundamental Weighting,” a de-tuned version of RAFI,13 fares better still by retaining some of the faster-growing stocks in CW Growth and gaining more from the rebalancing alpha.

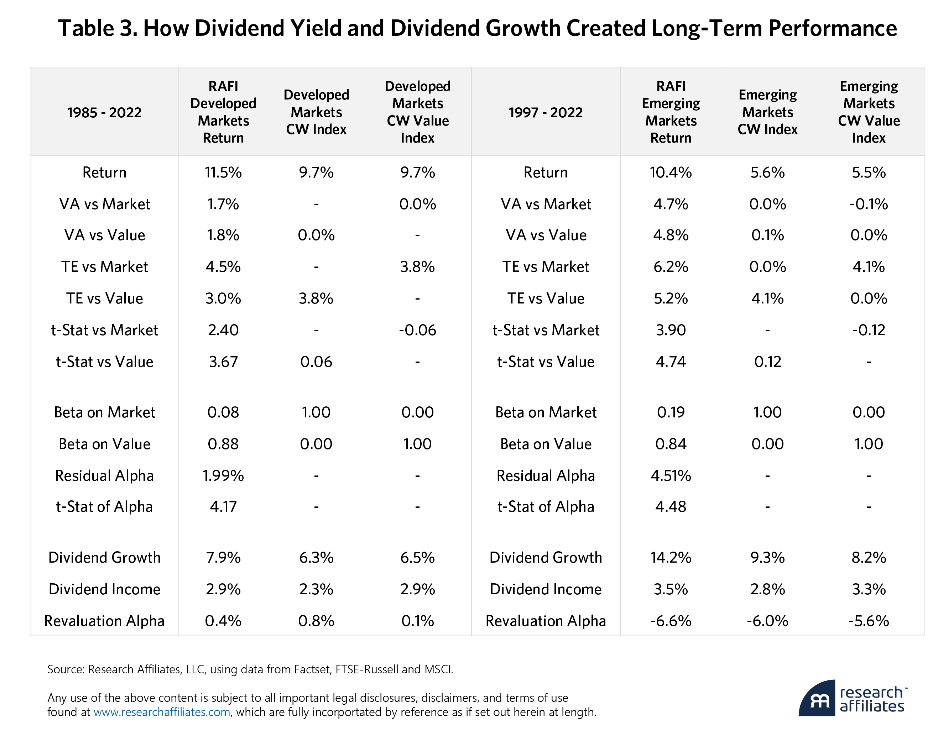

We end where we began, examining relative returns and the sources of those returns. We began with the live timespan from 2007 to 2022. Let’s now go back as far as we can find reliable data across the CW broad market, CW value, and RAFI strategies. These data begin in 1985 for the developed economies and 1997 for emerging economies (hence also 1997 for the All-World, which includes emerging economies). For developed markets, the live statistical significance is actually a bit better than the backtest, for emerging markets less so. The emerging markets are more mature, less volatile, and likely more efficient than in their early years. In all cases, the alpha is massively significant.

Consider Table 3 below. The return on almost any asset is the sum of income (for stocks, that’s dividends), growth in income, and changes in valuation levels (plus a small compounding effect). Over the past 38 years, the CW Developed Value portfolio delivered almost exactly the same return as CW Developed broad market portfolio, meaning that the value added before 2007 was nearly identical to the value lost since 2007. But the attribution tells a different story. The CW Value index enjoyed 20 bps faster dividend growth per year than the broad market (6.5% versus 6.3%), hence 40 bps faster than the growth portfolio.14 This is on top of the 60 bps higher dividend yield (2.9% versus 2.3%). So, value should have beat the market by 80 bps per annum. Over a 38-year span, this compounds mightily. But these benefits for the value investor were almost exactly offset by a revaluation alpha: the dividend yield for the CW Developed indices—but not for Developed Value—tumbled between 1985 and 2022. The decline was large enough to create a revaluation alpha of 80 bps per year, meaning that the price investors were willing to pay for each $1 of dividends rose by 80 bps per year.15

Consider that conventional CW growth strategies select faster-growing stocks than the stocks in a CW Value portfolio, by a wide margin. But, as we have seen, CW Value recoups that growth shortfall, due to a rebalancing alpha—helpful for value and massively hurtful for growth—that Fama and French call “migration.” RAFI magnifies that rebalancing alpha, by applying it across the entire portfolio, not just in choosing stocks to add and drop. The incremental dividend growth rate in RAFI is the source of its rebalancing alpha.

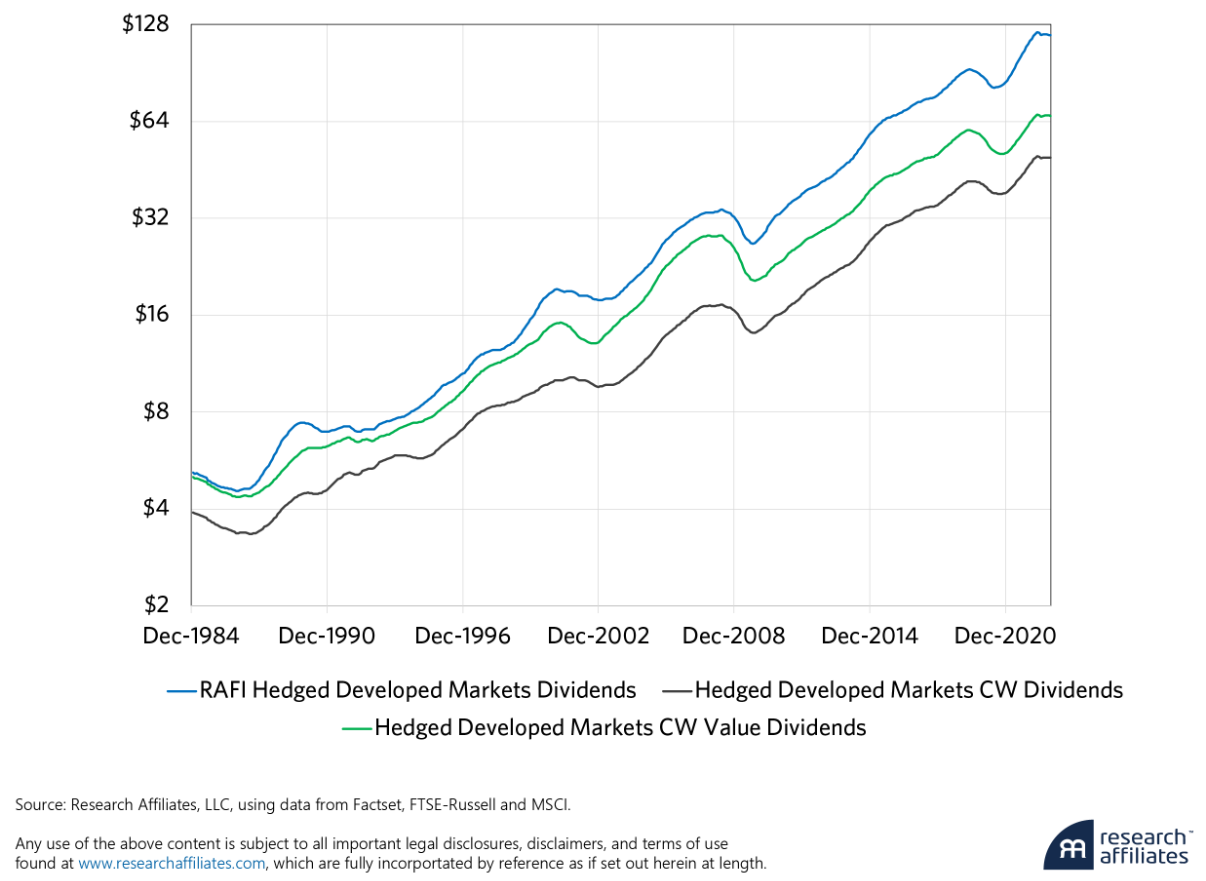

The historical non-US evidence (in Appendix 3, as reviewed earlier) supports the US finding that the dividends generated by a RAFI portfolio grow faster than the dividends earned by a broad market portfolio, by a margin large enough to deliver a substantial excess return versus the market. Again, this has nothing to do with RAFI selecting faster-growing stocks; it’s strictly a function of rebalancing into cheaper stocks with almost every rebalancing trade.

Conclusion

Results since 2007, after the 2004 launch of RAFI, the 2005 publication of “Fundamental Indexation,” and the launch of non-US developed and emerging markets RAFI variants in 2005 and 2006, can be viewed as “out-of-sample” tests. These tests confirm:

- that RAFI, worldwide, exhibits a stark value tilt, exactly as we acknowledged from the beginning;

- that the value tilt is, on average, very nearly the same as the value tilt for the CW Value indices;

- that RAFI magnifies the “migration” (rebalancing) alpha of CW Value; and

- that the incremental return relative to CW Value is large and exhibits strong (in some cases extraordinary) statistical significance.

In closing, we show how much of the return—for RAFI, for Value, and for the broad market—comes from income, from growth in income, and from revaluation. The last of these contributors garners shockingly little attention, even though it is so very important. Revaluation alpha matters because it is non-recurring and can seduce us into thinking that there are tremendous gains (or losses), when all that’s really happened is a one-off change of the market, and with that change, relative valuation has changed.

While we believe that RAFI represents a sensible alternative—or complement—to CW indexing, critics correctly observed its stark value tilt. Reciprocally, from the perspective of the broad macroeconomy, the CW market is a growth-tilted index. Toyota and GE are vastly larger than Tesla and NVIDIA in economic terms, even if the market is happy to value the latter pair far more highly than the former. Cap-weighting reflects a market-centric worldview; RAFI reflects an economy-centric worldview. From a market-centric worldview, RAFI is nothing more than a cleverly constructed value index that happens to soundly and reliably outpace CW Value. From an economy-centric worldview, the CW broad market portfolio is nothing more than a cleverly constructed momentum-chasing, popularity-weighted growth strategy.

Early critics of the idea did their clients and fans a costly disservice by discouraging the embrace of the idea. Had their investors embraced RAFI, if only to replace their allocations to value strategies, they would have earned thousands of basis points of incremental wealth, since the time we launched RAFI in 2004. We would go so far as to suggest that RAFI, to this day, remains arguably the best so-called “smart beta” strategy yet offered, when measured relative to a style-equivalent benchmark. For those who prefer to view it as a value strategy, we find it difficult to imagine any better way for our clients to manage their value allocations.

Please read our disclosures concurrent with this publication: https://www.researchaffiliates.com/legal/disclosures#investment-adviser-disclosure-and-disclaimers.

1. We are grateful to Ryan Giannotto of FTSE-Russell for his insights, and to Grant Kasser and Xi Liu of Research Affiliates for their contribution in gathering data and carrying out many of the analytics in this paper.

2. Arnott, Robert D., et al, 2005. “Fundamental Indexation.”

3. Treynor, Jack, 2005. “Why Market-Valuation-Indifferent Indexing Works.”

4. Arnott, Robert D., et al, 2013. “The Surprising Alpha from Malkiel’s Monkey and Upside-Down Strategies.”

5. Arnott, et al. 2023. “RAFI Rocks!! Taking Smart Beta Back to Basics.”

6. Relative performance for Emerging Markets Value, relative to the broad CW Emerging Markets, peaked in 2011, not 2007, and its severe crash started in 2018, not 2017.

7. There are minor exceptions. If we define our value and growth universe using a modified price/book value, incorporating intangibles (see Arnott et al., 2021), or if we use price/cash flow, the value factor recouped the GFC losses and made a small interim peak (a new high in cumulative relative performance, albeit by a scant 1-2%) in 2013. And, if we use price/sales, there is another small interim peak in 2017. No formulation of value, if based on relative valuation multiples, fails to underperform severely over the full 2007-2020 span. Arnott et al. (2021) also shows that the entire underperformance of value was a consequence of a plunge in relative valuation multiples, for value relative to growth; none was due to the fundamentals of a value portfolio underperforming that of a growth portfolio. The stocks were reeling, even as the underlying companies were doing fine.

8. It bears mention that RAFI’s average tilts (by sector, by country, and by style) contribute only about one-fourth of the RAFI alpha. RAFI’s stock selection (selecting on company size rather than market cap) contributes roughly another one-fourth. Dynamic shifts in the sector, country and style tilts comprise fully half of the RAFI alpha.

9. One of the great ironies of the history of the Nobel Prize is that Fama and Shiller shared the 2013 Nobel Prize in Economic Sciences, one for leading the development of the Efficient Market Hypothesis (EMH), and the other for suggesting a source of market inefficiencies!

10. Academe still ignores the importance of what we call “revaluation alpha,” the excess return of a factor or strategy that is due to changing relative valuation multiples. Many academics were openly considering the “death of value” in 2019 and 2020 (and some to this day), based on the evaporation of the statistical significance of the alpha for the value factor and associated long-only strategies. They fail to consider that downward revaluation in relative valuation multiples is inherently a non-recurring—and often mean-reverting—contributor to performance. We have written repeatedly on this topic, and find it shocking that academe still ignores the highly relevant distinction between revaluation alpha and alpha that comes from the underlying fundamentals of the associated portfolios.

11. I’m ignoring the demotions that fall into the small-cap list, as they are a minor part of the migration puzzle.

12. Even the CW broad market suffers from rebalancing, as stocks are deleted when they’ve fallen from grace and are trading cheap, then replaced with new high-fliers that are trading rich. The 4% average turnover for the CW market indices leads to a 1.02% “migration” effect. In other papers, we have shown that even a CW broad market portfolio can be constructed without much of this performance drag, merely by changing the rules by which stocks are added or dropped from the index.

13. Fundamental weighting, for the purposes of this article, begins with a portfolio of the 1000 largest market-cap stocks, reweighted using RAFI weightings, so it misses out on the roughly 50 bps return from selecting stocks on their fundamental business scale, and it suffers from some of the 102 bps rebalancing drag of the CW 1000 index. This was a concession to JPM referees, who did not want to see a commercial product (RAFI) featured in a scholarly journal.

14. Academia refers to this phenomenon—portfolios of growth stocks delivering slower growth in dividends or earnings than portfolios of value stocks—as a paradox. But it’s no paradox; it’s nothing more than the migration effect. If a growth investor chooses to avoid the growth drag from rebalancing (by not rebalancing) that won’t help. The problem is that some growth stocks fail to deliver the previously expected growth that was already amply recognized in their high valuation multiples. High-valuation-multiple stocks consist of those that deserve high multiples and those that do not; there are precious few growth stocks that ultimately deserve more than the consensus multiple. This is the “noise in price” model that Jack Treynor so elegantly demonstrated in 2005.

15. This is analogous to the analysis that I carried out in 2003, in my Financial Analysts Journal Editor’s Corner, entitled “Dividends and the Three Dwarfs” (March/April 2003), except at that time we separated real dividend growth from inflation. This is a topic that we may revisit in the months ahead, focusing on RAFI vs. CW in a global context.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All