A return to the Great Moderation Era looks unlikely, which might lead to an increasingly volatile—and somewhat unfamiliar—inflationary, economic, and geopolitical landscape.

It's human nature…or perhaps investor nature…to be myopic at times and focus on the short-term; especially recently with hyper-sensitivity to all things inflation and the labor market, given uncertainty regarding Federal Reserve policy. Every day, the probabilities around what the Fed will do at the next one or two Federal Open Market Committee (FOMC) meetings are pored over by investors trying to gain an edge. If only the Fed would ease its foot off the economic brake, we might assume the inflation dragon had been slayed and we could return to something resembling the pre-pandemic era. How likely is that?

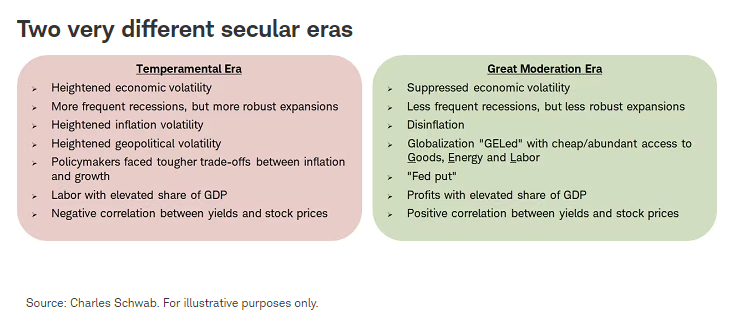

Let's widen the lens and ponder the possible transition we're in the midst of, to perhaps a different secular environment. The secular era that preceded the pandemic is often referred to as the Great Moderation; one during which disinflation reigned, economic volatility was subdued—save for the global financial crisis—and there was a steady tailwind associated with the epic decline in interest rates.

The Great Moderation era doesn't have an official start point, but in general it's seen as kicking in during the 1990s, although some references date as far back as the early 1980s. The era was punctuated by a number of key characteristics in addition to low economic volatility and disinflation; including longer economic cycles with less frequent recessions, a Fed quick to press the easy policy button all the way to zero, profits representing an outsized share of gross domestic product (GDP), and a positive correlation between bond yields and stock prices.

The era that preceded the Great Moderation and started in the mid-1960s—which we've been calling the Temperamental era—had a very different set of characteristics. They included heightened economic volatility with more frequent recessions (but sharper expansions), as well as greater inflation and geopolitical volatility. It was also an era when labor, via wages, represented a much larger share of GDP relative to profits, and when there was a consistent negative correlation between bond yields and stock prices.

Let's have a look at some of these relationships. Looking at GDP, shown below, the swings were larger and recessions—via the gray bars—were more frequent during the Temperamental era; but there was also more robust growth during expansions. Once the inflation dragon was finally slayed in the early 1980s—and following a mild and brief recession in 1991, the U.S. economy became much less volatile, with only two recessions prior to the pandemic. But as you can also see, both the economic highs and lows were lower than during the Temperamental era.

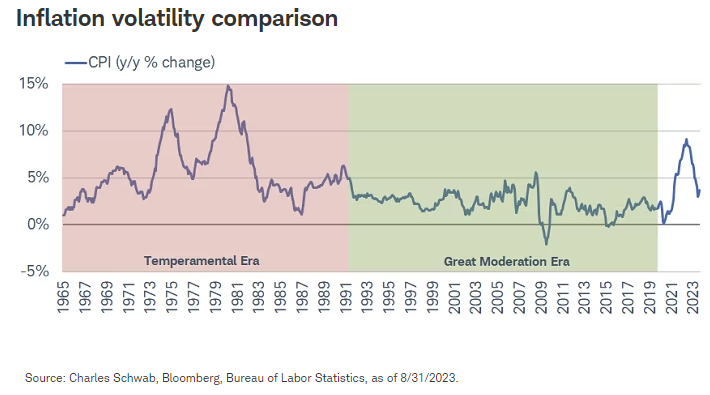

Moving on to inflation, during the Temperamental era, inflation volatility was on a tear—punctuated by the extreme peaks during the mid-to-late 1970s, as shown below. Those extremes were exacerbated by the Fed's decision on both occasions to declare victory early and ease policy, only to see the inflation genie let out of the bottle again. That led to the insertion of Paul Volker as Fed Chair, who "pulled a Volker" by aggressively raising interest rates to get the inflation genie fully back in the bottle. That directly hit the economy, with the famous double-dip recessions in the early 1980s; but it laid the groundwork for the Great Moderation era to come.

Disinflation during the Great Moderation was aided by a number of forces that were "GEL'ing." We've been using the GEL acronym in reference to the abundant and cheap access to Goods, Energy and Labor; courtesy of globalization, the U.S. energy boom and China ascendence into the World Trade Organization (WTO) in 2001. For the most part, all three of those ships are sailing.

We don't ascribe to deglobalization in its simplest form, but instead believe what we're seeing is a combination of regionalization and supply-chain rationalization/diversification. In large part due to the ravages of the pandemic, companies have shifted from a just-in-time to a just-in-case inventory mindset. Add climate change and geopolitics into the mix, and you have the brew for a more volatile inflation era. By the way, that's distinct from saying it's going to be a perpetually high inflation backdrop. We continue to believe in the near-term disinflationary trend; but we expect more inflation (and yield) volatility looking longer-term.

Labor power ascending?

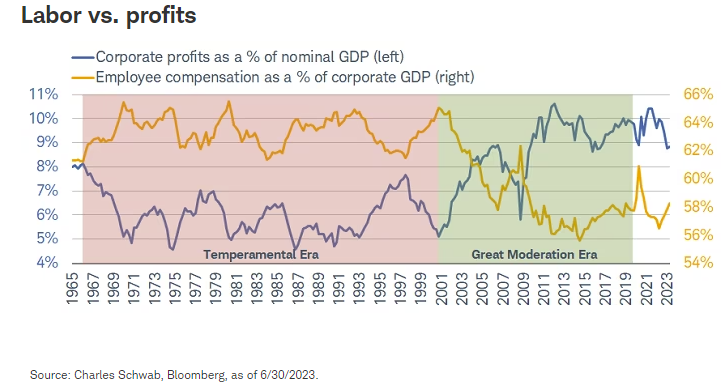

Another interesting relationship that shifted notably between the two eras was profits vs. labor. As the tech bubble was bursting in 2000, it ushered in a rather large shift in the trajectory of labor's share of GDP relative to corporate profits' share of GDP, as shown below.

The switch was initially flipped due to the severity of the profits recession as the tech bust was unfolding. Profits took a hit again during the financial crisis, but since then have been in a range near record highs as a share of GDP. Conversely, even with the brief spike during the pandemic, labor's share of GDP hasn't picked up to where it was a few decades ago. Yet, another convergence has begun, and this is key to watch to get a sense of whether we are transitioning into an era that might look more "temperamental."

Demographics

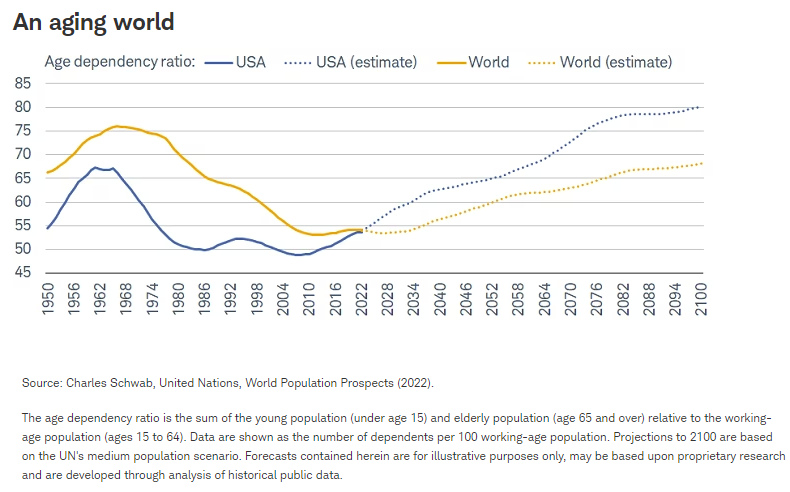

The United States and the world in general faced a demographic tailwind starting in the early 1960s. This has changed measurably. As shown below, the "age-dependency ratio" (the sum of the under-15 and over-64 population relative to the working-age population) has turned higher for the United States and the world, with the United Nations expecting a continued and steady rise for both. Admittedly, the projections do not take into consideration what have already been improvements in labor participation, including older people remaining in the workforce longer than in the past.

The elevating age-dependency ratio could have significant implications for the global economy—with influences on not just growth, but employment, interest rates, productivity, healthcare, and the relationship between investment and consumption. It's impossible to pinpoint the macro impacts, especially with additional—and possibly very beneficial—inputs to the "equation," like artificial intelligence (AI). For sure, there may be investment opportunities—they just might look quite different.

Bye bye, neoliberalism?

Just as the Great Moderation era has varying start points depending on metric being analyzed, there are other ways to think about possible tectonic secular shifts in the world order. One that is gaining adherents among the intelligentsia is about the retreat of "neoliberalism." Britannica defines the ideology as a policy model that emphasizes the value of free market competition, often associated with laissez-faire economics. Its emphasis is on minimal state intervention in economic and social affairs, and its commitment to the freedom of trade and capital.

In a recent report, the brilliant macro folks at TS Lombard took on the subject, titling the missive with "A Big Shift Everyone Would Rather Ignore." In it, they posit that "all the basic tenets of neoliberalism are under attack. Governments everywhere are running massive deficits (even at full employment), globalization is retreating, and public officials have even tried their hand at 'price controls' in a desperate attempt to contain the cost-of-living crisis. Yet it is the sudden popularity of industrial policy that takes the attack on a new neoliberalism to new extremes. What this means is deliberate attempts by governments to reshape the economy according to their own strategic ideas. Twenty years ago, such interventions were unthinkable. Today they are becoming the new normal."

There is no question we are seeing profound geopolitical shifts internationally, with the re-emergence of big geostrategic power rivalries (e.g., China vs. the United States and NATO vs. Russia). Perhaps it's wishful thinking, but we find ourselves—at least at this stage in the possible shift—in agreement with TS Lombard's less-pessimistic perspective. The more optimistic view is that "this new era won't be as bad as most assume, especially after a decade in which most economies seriously underperformed." The exclamation point on this view is that "you would have to be extremely myopic to think interest rates at 800-year lows were a 'good' thing, especially given the increasingly toxic political environment they were producing."

Investment landscape considerations

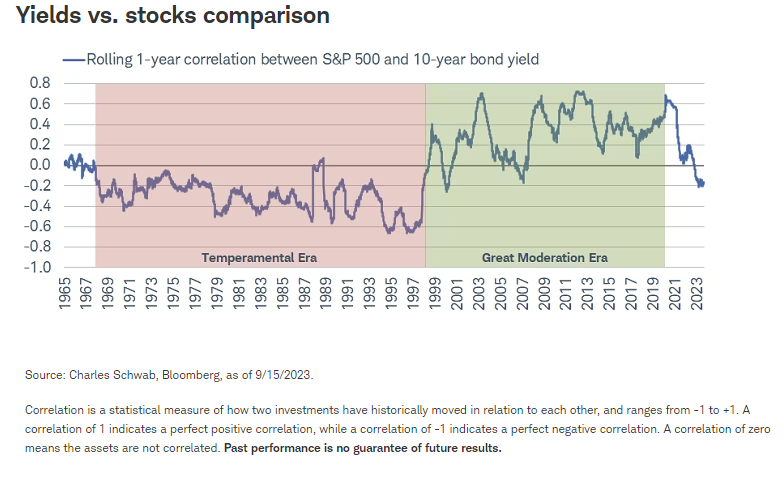

Key to the investment backdrop associated with a possible era transition is the relationship between the stock and bond markets; specifically, the correlation between moves in the 10-year Treasury yield and moves in the S&P 500®. As shown below, during the 30+ year period starting in the mid-1960s, the correlation was in negative territory for nearly the entire span. The explanation for this was, for the most part, inflation volatility. When yields were rising during this span, it was often because inflation was rearing its ugly head—a tough environment for stocks. The opposite was the case when yields were falling.

That was followed by a choppy transition around the bursting of the tech bubble; but from that point until the pandemic, the correlation was mostly positive other than during the height of the financial crisis. The explanation for this was, for the most part, disinflation. When yields were rising during this era, it was typically reflective of improving economic growth without an attendant inflation problem—a great environment for stocks. The opposite was the case when yields were falling.

In sum

If we're correct that the Great Moderation era is firmly in the rearview mirror, what are the implications—especially for this audience of investors? Many investors' full history has been solely defined by the Great Moderation backdrop. Assuming a transition to a more temperamental era, the investing landscape is likely to be changed—not necessarily worse or without opportunities, just different. We do believe we are likely to experience more volatility among inflation, economic growth, and geopolitics. We also believe we will see greater dispersion in equities' returns and reinforce what has been our focus for the past couple of years, which is on factor (or characteristic)-based investing. Finally, the combination of higher economic and inflation volatility, the lessons learned from the zero-interest-rate-policy "experiments," and surging government debt and its costs likely mean policymakers—both monetary and fiscal—have less flexibility than they did during the Great Moderation.

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third-party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

Past performance is no guarantee of future results and the opinions presented cannot be viewed as an indicator of future performance.

Investing involves risk including loss of principal.

The policy analysis provided by the Charles Schwab & Co., Inc., does not constitute and should not be interpreted as an endorsement of any political party.

Performance may be affected by risks associated with non-diversification, including investments in specific countries or sectors. Additional risks may also include, but are not limited to, investments in foreign securities, especially emerging markets, real estate investment trusts (REITs), fixed income and small capitalization securities. Each individual investor should consider these risks carefully before investing in a particular security or strategy.

All corporate names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security. Supporting documentation for any claims or statistical.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks including changes in credit quality, market valuations, liquidity, prepayments, early redemption, corporate events, tax ramifications, and other factors.

Lower rated securities are subject to greater credit risk, default risk, and liquidity risk.

Diversification strategies do not ensure a profit and do not protect against losses in declining markets.

Indexes are unmanaged, do not incur management fees, costs, and expenses, and cannot be invested in directly. For additional information, please see schwab.com/indexdefinitions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Charles Schwab

Read more commentaries by Charles Schwab