Equity Insights offers research and perspectives from Putnam’s equity team on market trends and opportunities.

Many of the features that make small-cap stocks compelling also point to the value of an active manager. A wide range of possible outcomes, a multitude of negative earners, and significantly less Wall Street coverage are just a few of the reasons investors in the small-cap universe should consider active managers who could steer them toward better results.

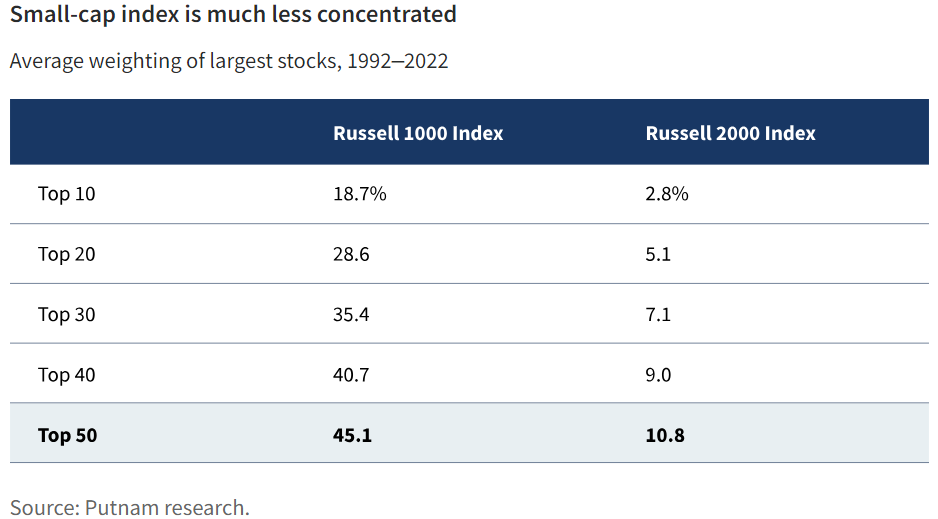

Small-cap indexes are less subject to concentration

The small-cap space is more egalitarian than a large-cap alternative. As we’ve witnessed this year with the “magnificent seven,” large-cap index performance is often dominated by a small number of companies. Concentration is considerably lower for the small-cap index. Over the past 30 years, on average, the Russell 1000 Index had nearly half of its weight in the 50 largest companies. By contrast, the Russell 2000 Index had only 11% of its weight in the equivalent top 50. When a few large names dominate an investment space, a portfolio manager will need to spend time trying to find an edge in that small set. A less concentrated investment space gives an active manager more range to prospect for better opportunities.

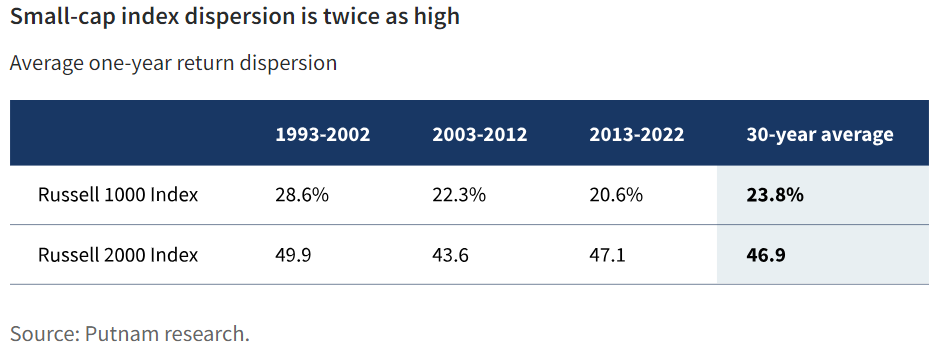

Small-cap stocks offer a higher dispersion of returns

One person’s risk is another’s opportunity. While it can bring more risk, a wider range of potential outcomes can also mean greater reward for being right. Managers with skill in selecting individual companies are likely to prefer a stock universe with greater dispersion. Just like index concentration, dispersion is an important measure for active managers. In each of the past 30 years, the small-cap Russell 2000 Index offered higher return dispersion than its large-cap Russell 1000 counterpart.

Moreover, in terms of sector allocation, small-cap active managers have a wider and more balanced range of opportunities. The S&P 500 Index, for example, has a 28% weight in technology stocks, while in the Russell 2000 Index, technology is only about 15%. The weightings for health care, industrials, and financials are also about 15% in the small-cap index.

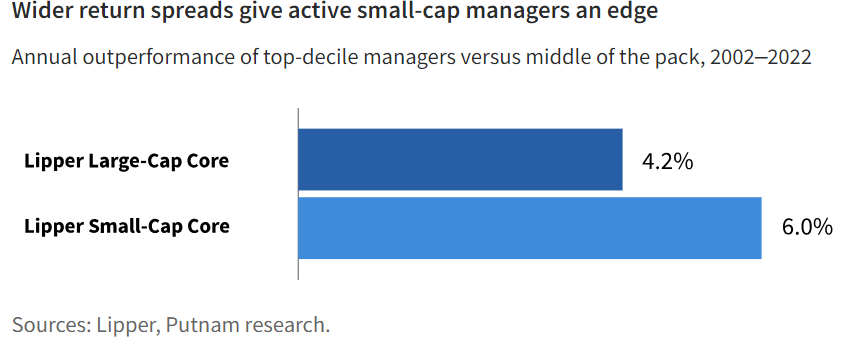

To illustrate the advantage of wider return spreads, we looked at the annual performance of top-decile managers in the Lipper small-cap and large-cap universes over the past 20 years. While many of these managers may be skilled stock pickers, small-cap managers benefit from the higher dispersion of returns.

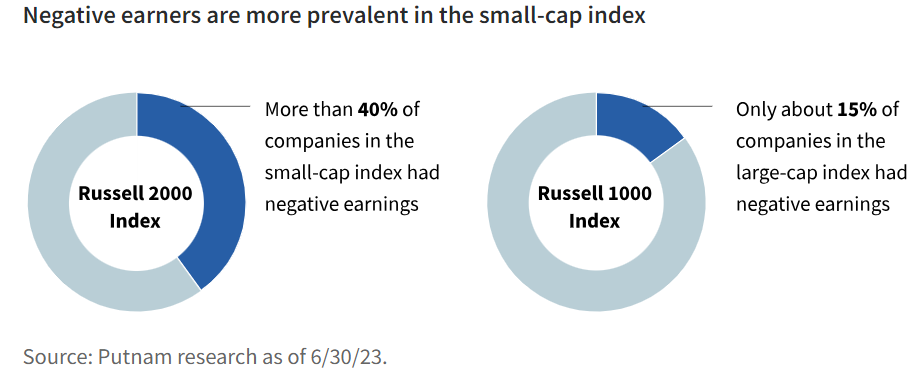

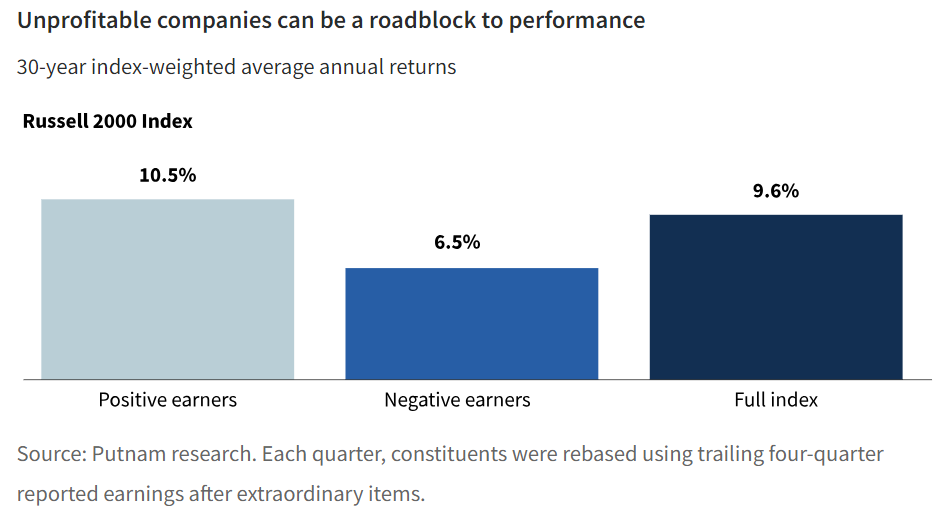

Small-cap investors risk high exposure to unprofitable companies

The small-cap universe is awash in negative-earnings businesses — a combination of shrinking has-beens and incubating might-be companies. High exposure to illiquid names or struggling companies and entire industries can weigh down a passive approach. An active manager can steer away from this group and occasionally identify a budding green shoot from within the lot of crabgrass.

Active managers have flexibility to avoid negative earners

Looking more closely at these unprofitable businesses over the past 30 years, we imagined splitting each index into two parts — negative earners and positive earners. For the 30-year period, on average, non-earning companies made up 21% of the small-cap index and 6% of the large-cap index. In both the large-cap and small-cap indexes, negative earners were underperformers. Negative earners tend to be either struggling prior earners or early-stage growers. For small caps especially, these stocks represented a roadblock to the overall performance of the index. Investors with a passive allocation to the Russell 2000 are essentially funding those negative earners. An active small-cap manager has the flexibility to selectively avoid this group, prospect carefully for growing names, or focus on proven earners.

Small-cap stocks are less efficiently priced due to scant coverage

An unobserved company may offer more opportunity, while a highly watched business might have no new angles to discover. Small-cap stocks have significantly less coverage by investment research analysts. More than half of the stocks in the Russell 2000 Index have fewer than five firms covering them with published earnings estimates. In addition to providing active managers with a lot of unexplored territory, this scant Wall Street coverage can result in inefficient pricing. The large-cap Russell 1000 index by contrast has 91% of its names covered by five or more analysts. Active managers have more flexibility to identify and capitalize on lightly covered small-cap stocks.

It is also worth noting that performance of small-cap stocks has lagged considerably over the past five years. The Russell 2000 Growth Index and Russell 2000 Value Index were “bottom dwellers” in their respective Lipper competitive spaces for the five years ended June 30, 2023. The Russell 2000 Value is ranked at the 69th percentile, and the Russell 2000 Growth is found way down in the 84th percentile. This may provide fertile ground for active portfolio managers to identify inefficiently priced stocks. When investing in small caps, we believe active is the way to go.

The views and opinions expressed are those of the author, are subject to change with market conditions, and are not meant as investment advice.

The S&P 500® Index is an unmanaged index of common stock performance. The Russell 1000® Index is an unmanaged index composed of approximately 1,000 of the largest companies in the Russell 3000® Index as measured by their market capitalization. The Russell 2000® Index is an unmanaged index composed of approximately 2,000 of the smallest companies in the Russell 3000® Index as measured by their market capitalization. The Russell 2000® Growth Index is an unmanaged index of those companies in the small-cap Russell 2000 Index chosen for their growth orientation. The Russell 2000® Value Index is an unmanaged index of those companies in the small-cap Russell 2000 Index chosen for their value orientation. You cannot invest directly in an index.

Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Putnam

Read more commentaries by Putnam