Restricting the money supply will help contain inflation.

In the classic crime drama film Scarface, Elvira’s character gives Tony Montana a useful piece of advice: “don’t get high on your own supply.” The maxim has roots in the narcotics trade, but it can apply to the addiction that an economy can develop to its own money supply.

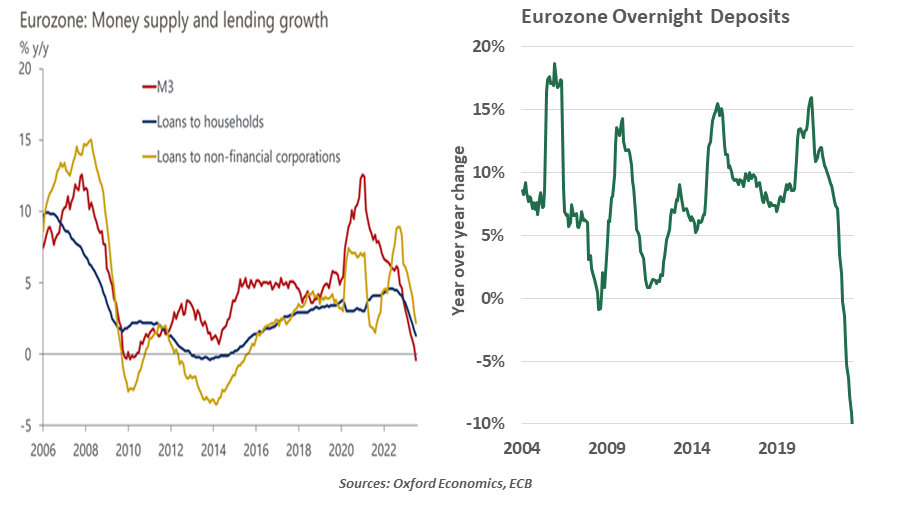

Since the 2008 global financial crisis, the European Central Bank (ECB) has allowed the money supply to increase twice as fast as the growth rate of economic output. Initially, the expansion failed to boost inflation, casting doubt on the monetarist conventional wisdom that inflation is always and everywhere a monetary phenomenon. But during the COVID recovery, excess liquidity set the stage for today’s elevated eurozone inflation.

In recent research, the Bank for International Settlements found a statistically significant relation between money growth and inflation in the eurozone. Easing monetary conditions preceded the rise in prices across the bloc, and economies with stronger money supply growth witnessed noticeably higher inflation.

The money supply is one of the main metrics being monitored by the ECB to check the impact of recent policy tightening. Trends in this data have raised hopes for continued disinflation.

The eurozone broad money supply (M3) posted its first decline in more than a decade on the back of higher interest rates and ongoing balance sheet reduction. Private sector lending growth dropped to its slowest rate since 2016, and bank deposits declined in July. Credit standards have tightened further, with the banks indicating that they would continue along this path during the third quarter. As lending dries up and short-term deposits shrink, economic activity is likely to slow and inflation to moderate.

Monetary policy works with long and variable lags. Past research suggests that the real economy feels the impact of tightening after nine to 12 months. The ECB’s tightening cycle is already into its 13th month, and weaker business surveys are pointing to a fresh downturn. This could trigger a debate within the Governing Council whether another hike is necessary in September.

The ECB might just be able to justify a pause this month. But a lack of substantial progress in curbing underlying price pressures amid tight labor market conditions could force their hand. Withdrawal from the era of easy money will not be painless, but it will be necessary.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions. © 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust