How serious is the Unfolding Chinese Debt Crisis?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“When the wind of change blows, some build walls while others build windmills.”

Li Keqiang, Former Premier of the People’s Republic of China

The backdrop

Things are not exactly going China’s way these days. It has been one glitch after the other more recently. A few weeks ago, Chinese property giant, Evergrande, filed for bankruptcy in the courts of New York, and when the stock started trading again days ago, after having been suspended for 17 months, the price was off almost 90%. All this has happened only a few weeks after Country Garden, another big Chinese property company, missed $22.5 million of bond payments. And, as I sit here and put this note together, news runs across my screen that the $2.9Tn Chinese investment trust industry may also be in trouble – because of defaulting property investments.

That reminds me of a new research paper from JPMorgan saying that it now expects 10% of all Chinese high-yield corporate debt to default this year – up from a previous estimate of 4%. The situation is getting pretty bad in China – in fact, so bad that Chinese state-owned banks have been asked by the government to support a weakening Renminbi. Furthermore, in parts of China, civil servants are having their pay slashed, bus services are being shut down and, to add insult to injury, there is even a proposal on the table to cut pensioners’ medical benefits which, by the way, has led to civil unrest in a number of cities.

Foreign investors have begun to take their precautions. In the second quarter of 2023, foreign direct investments in China fell 87% year-on-year to $4.9Bn, and the Chinese government appears to be embarrassed. Shortly after the June employment report was published, it vanished again. Could it be because the report showed an all-time high of 21.3% in youth unemployment? Likewise, the recently released report on land sales, which showed a massive 50% decline in 2022 vs. 2021, has also mysteriously disappeared.

In other words, something is not quite right, but what is it? I could probably write a 300-page book on this topic, but I shall try and keep it short and sweet. Although China suffers from many problems, they can essentially be boiled down to two – a mountain of debt and horrendous demographics. The first of those two problems is a function of the government’s desire to turn China into a modern, urban society in record time, which has resulted in plenty of reckless lending, whereas the second is the result of a misguided attempt to control population growth. Let’s begin with the lending problem.

The End of the Chinese debt supercycle?

Long-term readers of my work will be aware that we have identified seven megatrends, and one of them we call Late Stages of the Debt Supercycle. A debt supercycle is very long. Over the past 2-300 years (there is no data pre-industrial revolution), the average supercycle has lasted 60-65 years, and the last one to collapse was the one in Japan in early 1990. The last debt supercycle to collapse in our part of the world was the one that marked the end of the Great Depression in the 1930s, so we are due another collapse.

Now, a bit of background, which will explain why China could quite possibly be at the doorstep of their own debt supercycle collapse. In the early stages of all debt supercycles, GDP and debt grows roughly 1:1; however, as the supercycle matures, it takes more and more debt to grow GDP. When the ratio reaches about 1:4, i.e. it takes $4 of additional debt to grow GDP by $1, the party is effectively over. In the past 2-300 years, every single time ΔGDP-to-ΔDebt has reached 0.25 (+/-), the supercycle has collapsed – every single time, and that is where China is now!

I shall not, in this letter, go into details on the investment implications, as I am not allowed to, but subscribers to ARP+ will be pleased to learn that I will provide much more colour on that, and how investors can benefit from the ongoing slowdown in economic activity in China, in our autumn seminar in a few weeks’ time. In this context, suffice to say that a slowdown can impact the rest of the world in three ways and, the more dramatic the slowdown is, the more dramatic the impact will be. It may:

A. negatively impact exports to China;

B. drive down the price on commodities – particularly on commodities that are critical to the modernization of the Chinese economy;

C. unsettle financial markets worldwide (possibly another Lehman moment).

Let’s go back to the debt supercycle collapse in Japan for a moment. As you can see in Exhibit 1 below, the Nikkei 225 is still almost 20% below the peak it reached in December 1989, and we are now almost 34 years post the debt supercycle collapse in Japan. I can only urge you to take the debt supercycle phenomenon seriously. The implications of a debt supercycle collapse are serious. I probably don’t have to remind you that the last collapse in our part of the world led to World War II.

Ugly demographics

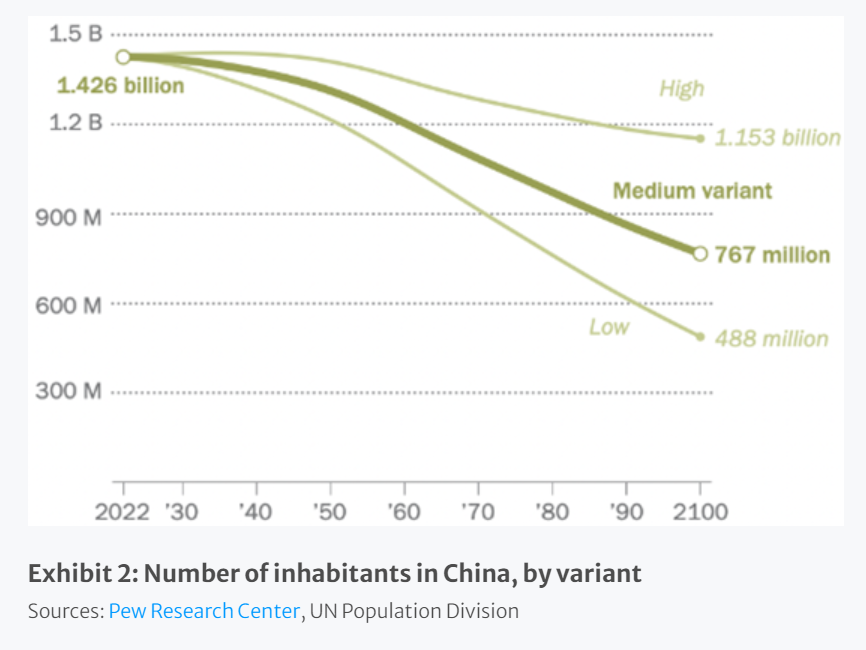

Today, the Chinese population is made up of about 1.4 billion people. According to the UN, by the end of this century, there will most likely be no more than 7-800 million left (the median variant in Exhibit 2 below). As you can see, under more pessimistic assumptions (the low variant), there won’t even be 500 million Chinese by 2100. From an economic momentum point-of-view, that is an unmitigated disaster.

The reasons are many. First and foremost, the Chinese fertility rate is on a sharp decline. Last year, it was only 1.16 vs. a replacement rate of 2.1. If you go back to the years after World War II (the baby-boom years), the fertility rate in China hovered around six. Like in many other EM countries, as living standards have risen, women have chosen to have fewer children, and they have them much later in life nowadays.

Adding to that, a skewed sex ratio has led to a serious shortage of women. The problem peaked some 20 years, when 118 boys were born for every 100 girls. Although the problem has moderated somewhat, the sex ratio continues to be skewed. As of 2021, it was still 112 (source: Pew Research Center). The skewed ratio is driving many men to leave the country, which doesn’t make things any better. Although the numbers vary from year to year, between 200,000 and 400,000 Chinese emigrate every year (on a net basis), and most of them are young men.

The inevitable implication of the unfavorable Chinese demographic outlook is that the Chinese leadership will struggle to deliver economic growth anywhere close to what they have set out, and promised, to deliver, i.e. 5-7% per annum. And the fact that domestic migration (from rural zones to urban zones) seems to have peaked doesn’t help either. The view in financial circles is that this year, China will probably land around 3% in terms of GDP growth.

The problem facing the Chinese leadership is that, in a fast-growing economy like the Chinese, 3% growth feels like a recession. Therefore, under normal circumstances, I would probably have predicted that more public construction projects would be started; however, circumstances in China are far from normal at present and the leadership cannot plainly ignore the mountain of debt the economy is saddled with. Just look at events over the last few months, where a very clear signal has been sent to decision makers. A curb on public spending is a simple must, and that leaves few options unless they can find ways to stimulate consumer spending, which is quite low in China.

How serious is all of this?

Going back to the point I made earlier, i.e. that a slowdown in China can impact the rest of the world in three ways, allow me to finish this letter with a few observations on those points. As far as exports are concerned, an economy like the German could be severely affected, as Germany exports a great deal to China. The US economy, on the other hand, will hardly be affected, as US exports to China are miniscule when compared to the size of the US economy – a $25 trillion monster economy. Last year, ‘only’ about $155 billion worth of goods and services were exported to China. Therefore, even a severe Chinese recession will hardly be noticed on the bottom line in the US.

Having said that, and as stated earlier, a Chinese slowdown can, and probably will, affect the rest of the world in other ways. My biggest concern is the psychological impact a meltdown might have on other financial markets, should things go from bad to worse in China. If investors collectively conclude that China has indeed reached the end of the road in terms of debt accumulation, the fact that the impact on the real economy would be quite modest will probably be ignored.

As I write these lines, I note that the DAX index of German equities is up 14% year-to-date, while the S&P 500 index of US equities is ‘only’ up 12% over the same period. If my logic is correct, the German economy will suffer a great deal more than the US economy, should economic fundamentals deteriorate further in China. Therefore, from a fundamental point-of-view, one should favour US equities over German equities, if one is concerned about China. On the other hand, as we learnt in 2008, once the cat is out of the bag, fundamentals do not necessarily apply, and the collateral damage can be immense.

Niels C. Jensen

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All