David Dali, Head of Portfolio Strategy, provides his 12-month outlook for global equity markets.

Outperformance Beckons in an Easing Environment

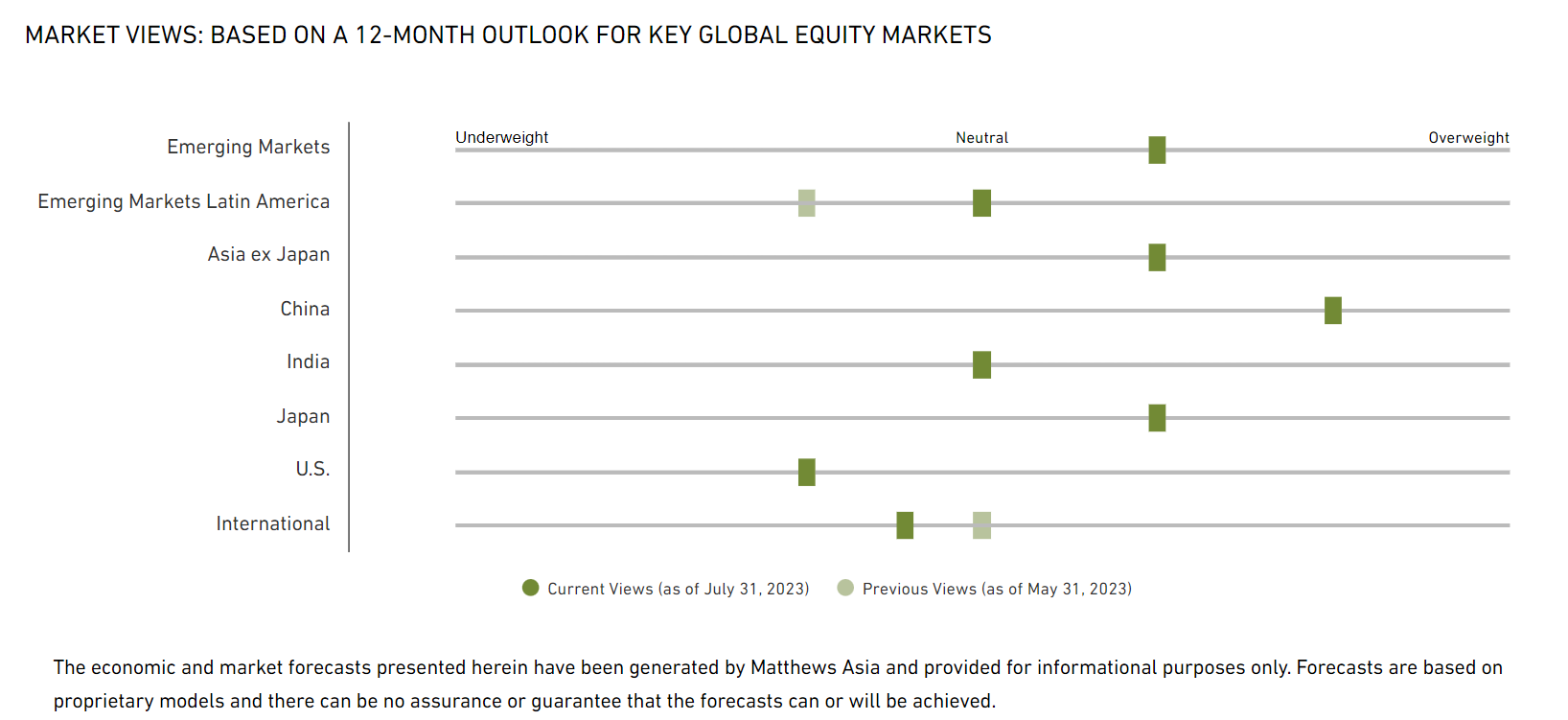

Persistent tightening of U.S. and European monetary policy is contrasting with early-stage loosening in emerging markets (EM). This easing, combined with positive policy actions in China, has strengthened my conviction that Asian and EM equity allocations may outperform in the coming quarters.

Emerging Markets

- Emerging markets (EM) have been held back as China’s weak post-COVID recovery has weighed on sentiment. I expect this to change, however, as China begins to make policy moves to address its economic challenges. In addition, returns from EM excluding China have kept up with developed international markets this year and going forward, their diverse characteristics could buffer their economies against constrained liquidity conditions in developed markets.

- Regionally, I’ve upgraded my view of Latin America from underweight to neutral as tight monetary policy has helped strengthen currencies and created room for policy easing.

- I’m more positive about Asia ex Japan where I remain overweight. China’s challenges are fading and recovering domestic demand should support imports from Korea, Taiwan and the Association of Southeast Asian Nations (ASEAN) countries, helping offset a policy-induced slowing in the global economy.

- Among single countries, China remains overweight as the government has finally begun to make policy moves to address the current crisis of confidence. Recent policy announcements include support of platform companies (which should have a positive impact on employment, especially for college graduates), more tax incentives and easing household credit, property developer loan relief, and relaxing of overseas borrowing restrictions to stabilize the Chinese currency. Lastly, although geopolitical tensions will remain, recent visits to China by Antony Blinken, Janet Yellen and John Kerry show a willingness from both sides to engage.

- In India, economic growth remains solid and early tightening of monetary policy has tempered inflation to create an almost Goldilocks scenario. While India seems poised to perform well against regional peers I’m keeping my neutral view. Inflationary risks remain which could force the central bank into another round of rate increases not priced into already elevated valuations.

Developed Markets

- Japan’s market is enjoying a trifecta of support including a return to reflationary GDP growth, government and activist-induced pressure on undervalued companies to increase their payout and buy-back ratios, and a surprise widening of the 10-year yield curve control (YCC) band which keeps monetary policy very accommodative while adding support to the Japanese yen.

- The U.S. is showing incredible resiliency to rising rates and tighter credit. However, economic strength can lead to uncertainty around Federal Reserve policy and may bring additional rate hikes into play. I expect a more difficult earnings environment in the next 12 months amid lofty valuations.

- I’ve downgraded my view on developed international investments, with the exception of Japan, to underweight from neutral, due to tightening financial conditions and lower earnings-growth consensus. Additional headwinds include continued volatility in energy prices and the impact of the war in Ukraine.

David Dali is Head of Portfolio Strategy at Matthews. David serves as a macro thought leader and as a proxy for portfolio managers, providing insights and analytics to clients. He has spent much of his career allocating and investing in equities, fixed income, currencies and derivatives.

Notes:

Emerging Markets is based on the MSCI Emerging Markets Index, which captures large and mid-cap representation across 24 Emerging Markets countries. Constituents include Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

Emerging Markets Latin America is based on the MSCI Emerging Markets Latin America Index, which captures large and mid-cap representation across five Emerging Markets countries in Latin America, including Brazil, Chile, Colombia, Mexico, and Peru.

Asia ex Japan is based on the MSCI AC Asia ex Japan Index, which captures large and mid-cap representation across two of three Developed Markets (DM) countries, excluding Japan, and eight Emerging Markets (EM) countries in Asia. DM countries include Hong Kong and Singapore. EM countries include China, India, Indonesia, Korea, Malaysia, the Philippines, Taiwan and Thailand.

China is based on the MSCI China Index, which captures large and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs).

India is based on the MSCI India index, which is designed to measure the performance of the large and mid-cap segments of the Indian market.

Japan is based on the MSCI Japan index, which is designed to measure the performance of the large and mid-cap segments of the Japanese market.

U.S. is based on the MSCI USA index, which is designed to measure the performance of the large and mid-cap segments of the U.S. market.

International is based on the MSCI World ex USA index, which captures large and mid-cap representation across 22 of 23 Developed Markets (DM) countries-- excluding the U.S. DM countries include Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the U.K.

You should carefully consider the investment objectives, risks, charges and expenses of the Matthews Asia Funds before making an investment decision. A prospectus or summary prospectus with this and other information about the Funds may be obtained by visiting matthewsasia.com. Please read the prospectus carefully before investing.

Investments involve risks, including possible loss of principal. Investments in international, emerging and frontier markets involve risks such as economic, social and political instability, market illiquidity, currency fluctuations, high levels of volatility, and limited regulation, which may adversely affect the value of the Fund's assets. Additionally, investing in emerging and frontier securities involves greater risks than investing in securities of developed markets, as issuers in these countries generally disclose less financial and other information publicly or restrict access to certain information from review by non-domestic authorities. Emerging and frontier markets tend to have less stringent and less uniform accounting, auditing, and financial reporting standards, limited regulatory or governmental oversight, and limited investor protection or rights to take action against issuers, resulting in potential material risks to investors.

Investing in small- and mid-size companies is more risky than investing in larger companies as they may be more volatile and less liquid than large companies. In addition, single-country funds may be subject to a higher degree of market risk than diversified funds because of concentration in a specific industry, sector, or geographic location. Pandemics and other public health emergencies can result in market volatility and disruption.

Fund holdings are subject to change and risk. For current holdings, please visit each Fund’s individual overview page.

ETFs may trade at a premium or discount to NAV. Shares of any ETF are bought and sold at market prices (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns.

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific investment vehicles.

The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information. Matthews International Capital Management, LLC is the advisor to the Matthews Asia Funds.

Matthews Asia Funds are distributed in the United States by Foreside Funds Distributors LLC

Matthews Asia Funds are distributed in Latin America by Picton S.A.

A message from Advisor Perspectives and VettaFi: Just as artificial intelligence (AI) is helping advisors create videos, write blogs, construct portfolios and coach clients, companies throughout the world are using it to deliver more value to their clients. Learn about the future of AI and the investment opportunities it is creating at our next symposium, on August 30 at 11 am ET. Click here to register.

© Matthews Asia

Read more commentaries by Matthews Asia