Signs of falling inflation have helped risk assets recently, but the relief is likely temporary. Volatility may continue in fixed income markets, as high-interest rates continue to weigh on balance sheets and the market digests the probability of a potential recession.

- Inflation data was lower recently, but we believe it is likely to stabilize above 2%.

- The probability of recession remains 45%, and the likely timing remains mid-2024.

- Rates could cause a major risk-off event in the fall of 2023.

Inflation will remain sticky

In the U.S. and other major developed market countries, inflation will be coming down further in the months ahead. This is partly due to monetary tightening and partly due to the normalization of supply chains, labor markets, and the global economy as pandemic effects fade. The underlying inflation in the new steady state will emerge once one-offs fully wane.

Falling global inflation might deceive many, but in a new world where households have a greater willingness to consume while liquidity is relatively high, inflation is likely to stay above pre-Covid levels.

When inflation is high but falling, central banks can pause and wait but cannot cut the policy rate quickly. At the same time, liquidity is still abundant, albeit falling, and, hence, the willingness of investors to buy anything, including Treasuries, remains high.

Core inflation is likely not going back to 2%. The summer months are the peak season for base effects of annual comparisons to a year ago. The annual comparisons won't make inflation look like it's improving in the months ahead. Wage inflation is not coming down, and this is likely to keep core inflation sticky at around 3.0%–3.5%.

More rate hikes are likely

In the near term, the Federal Reserve's view on inflation matters quite a bit. Recent releases of Fed meeting minutes showed that members were concerned about the outlook for a couple of measures that have shown few signs of recent slowing — inflation in housing services and core non-housing services. Given this viewpoint, we consider that after the July hike, another is likely, probably in November.

The Fed's efforts against inflation so far have not caused rising unemployment or financial instability but, sooner or later, we believe a trade-off will arrive.

The potential for a recession

Markets seem to be pricing out a recession. Risk assets have tolerated the move to higher rates in recent months. Although smaller payroll gains are unavoidable at this stage of the economy, the labor market is strong. Layoffs may increase but not become widespread. There are also signs of bottoming in the U.S. housing market and signs of stabilization in global manufacturing.

In our view, the probability of a recession remains significant as monetary policy works with lags. Over time, companies will have to reissue maturing debt at higher interest rates, and consumer spending will face further headwinds as student loan payments resume later this year. Weaker sales along with declining profitability can start widespread layoffs, resulting in a recession.

However, the more the recession is delayed, the more central banks come into play. For a U.S. recession to occur, it will require that the Fed continue to hike rates above current levels and/or keep rates high for longer.

Why a risk-off event could happen

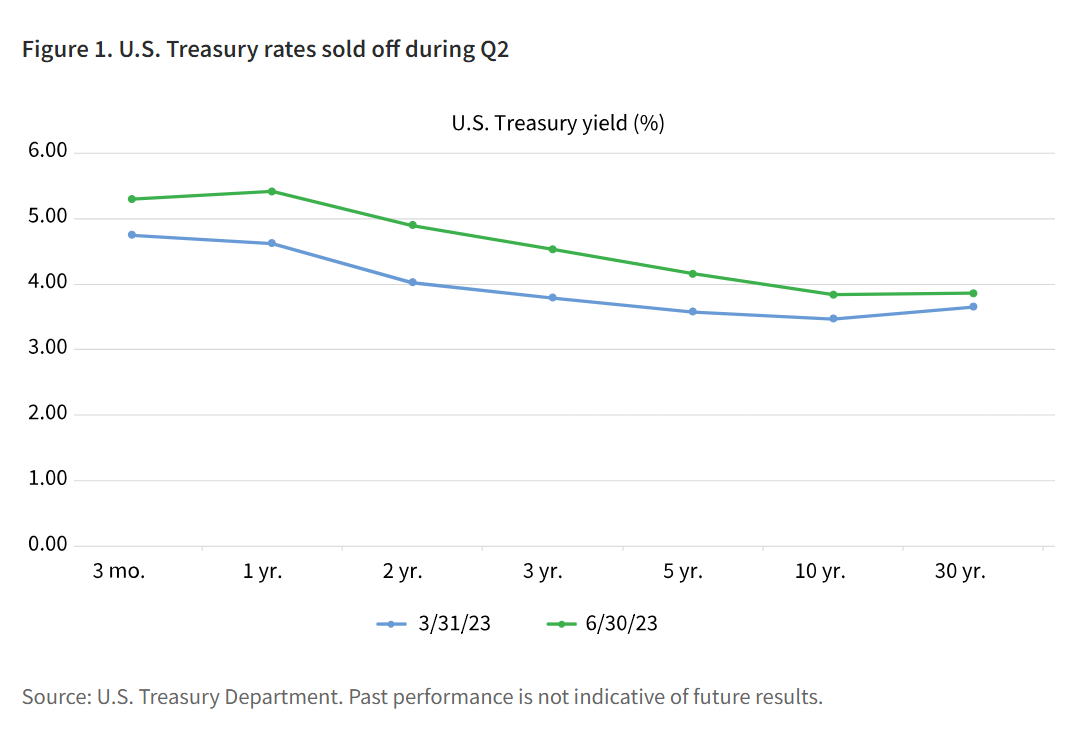

Liquidity is still abundant but declining. Since the debt ceiling issue is resolved, the Treasury will be increasing its coupon supply. Increasing Treasury supply while liquidity is falling can raise Treasury yields. The financial markets have been pricing out recession risks, as the economy remains resilient, but are not prepared for a spike in rates. The risk rally in 2023 has been mostly thanks to falling rate expectations. Risk assets are due for a correction if rates rise.

Stagflation might be ahead

A scenario of sticky inflation is as likely as a recession in the next year, we believe, and in the long run, we see an elevated probability for stagflation.

It might soon be time to consider investments for this scenario. In an inflationary environment, assets whose prices can rise along with consumer prices maintain their real value. Commodities and real assets like property are well-known examples.

In fixed income, TIPS, despite trading in a less-liquid market, can potentially do better than nominal Treasuries if inflation stays. Future inflation currently priced by the Treasury market is likely to be less than the actual inflation that will be realized over time.

Toward the end of the 1970s — a painful decade for investors — a broad consensus was reached that inflation was the main problem. Only after then, a hawk-like Paul Volcker became the chair of the Federal Reserve. Today, the discussion about persistent inflation is just starting. Many still believe that inflation will fall naturally without necessitating a recession and are willing to invest in assets that do not perform well in inflationary environments. While there are still hopes for genuine disinflation, neither society nor the Fed is ready to take the most painful medicine.

This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon as research or investment advice regarding any strategy or security in particular.

This material is prepared for use by institutional investors and investment professionals and is provided for limited purposes. This material is a general communication being provided for informational and educational purposes only. It is not designed to be investment advice or a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. The opinions expressed in this material represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the material. Predictions, opinions, and other information contained in this material are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

This material or any portion thereof may not be reprinted, sold, or redistributed in whole or in part without the express written consent of Putnam Investments. The information provided relates to Putnam Investments and its affiliates, which include The Putnam Advisory Company, LLC and Putnam Investments Limited®.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Putnam

Read more commentaries by Putnam