Capital Markets Outlook offers perspective on the global economy and asset classes with insight into market history.

Jason Vaillancourt is a Global Macro Strategist on the Capital Market Strategies team. He provides in-depth global macroeconomic research to Putnam clients and the broader financial community.

While we agree with the enthusiasm for AI that has helped the market rally, investors may be better served by patience than by chasing recent risk-on sentiment.

- Beyond the Magnificent Seven stocks driven by AI enthusiasm, the rest of the stock market has been flat.

- Multiple macro indicators are pointing to a weaker economic environment in the second half of 2023.

- With central bankers focused on inflation, the risk of a policy error increases.

It is easy to lose track of how many mini-bubbles have popped over the past few years. SPACs, crypto, cannabis, memes, and WFH stocks all come to mind. The strong NASDAQ FOMO rally of the past few months has largely been driven by the usual suspects of what we at Putnam have recently been referring to as The Magnificent Seven.1 This group of companies has been responsible for generating the bulk of returns in U.S. large-cap equities; without them, the Russell 1000 Index would be close to flat in the first half of 2023. Before the AI frenzy, these seven stocks had trended lower in sync with rising Treasury yields in 2022. Perhaps unsurprisingly, the last time leadership in the domestic equity indexes was this concentrated was in late 1999.

The Magnificent Seven AI stocks outperformed in a mostly flat 2023 market

The relative performance of seven AI stocks versus the remaining stocks of the Russell 1000 Index (values indexed to 1.00 as of 1/2/22, left axis) and the 10-year Treasury yield (right axis).

Source: Putnam. Past performance is not a guarantee of future results. References to specific securities should not be taken as a recommendation to buy or sell those securities but are included for the purposes of illustration and/or information only. It should not be assumed that investment in the securities mentioned was or will be profitable. The Russell 1000® Index is a stock market index measuring the performance of the largest 1,000 public companies in the U.S. by market capitalization. Frank Russell Company is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Frank Russell Company.

A party like it's 1999

The parallels of the current market environment to 1999 are numerous. At that time, excitement over the possibility of widespread commercial adoption of the internet2 was palpable. The Federal Reserve was sending mixed messages, simultaneously increasing the policy rate while adding liquidity in anticipation of possible banking and payments-systems issues surrounding Y2K. All the while, Fed Chair Alan Greenspan had been touting a surge in productivity arising from technology-driven investment in the late 90s as a potential growth tailwind (which ultimately underwhelmed3). All of that certainly rhymes with the potential for generative AI as a productivity enhancer and margin booster for the corporate sector. As does a central bank now tightening policy while maintaining an astronomically large (at least by historical standards) balance sheet. Even in the context of QT, the Fed has added more lending facilities to help struggling regional banks.

No part of this stroll down memory lane is intended to suggest an imminent collapse of tech stocks on par with the dot-com bubble. (Recall that the Nasdaq fell ~83% from its peak in March 2000 to the ultimate low in 2002.) Importantly, the vast majority of those bubble stocks in that earlier era mostly went away, as they had no earnings and high cash-burn rates. In fact, it seems reasonable to expect that the main beneficiaries of the explosive growth of AI will be mostly sourced from members of the already-entrenched Magnificent Seven. This is due to a combination of direct exposure, network effects, and near-monopolistic pricing power for the "picks and shovels" of the underlying technology.

Beyond the seven AI stocks, it's less rosy

Despite all the good news creating enthusiasm for these AI plays, the same cannot be said of the rest of the publicly traded equity market, which continues to exhibit lackluster forward-earnings-revision characteristics. The impressive breakouts of the S&P 500 Index and Nasdaq appear much less impressive if we look at equal-weighted indexes or look further down in the capitalization spectrum. And there's more. The message from commodity markets is painting a rather unflattering picture of the global economy. The recent guidance from FedEx's June 21 earnings announcement points to a weaker growth outlook in the second half of the year. Similarly, the recent struggles of bellwether European luxury goods companies such as LVMH, Hermes, and Christian Dior suggest the global high-end consumer may not be in strong shape.

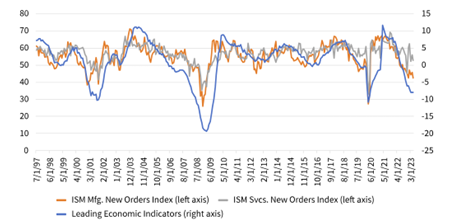

We continue to expect the economy will slow and perhaps stall near the end of the year as the lagged effects of an inverted yield curve and tightening lending conditions make their way through the system. The message from the Conference Board's Index of Leading Economic Indicators, driven in part by a dramatic decline in new manufacturing orders, has rarely been this weak in the period since The Great Inflation ended in the 1980s and The Great Moderation began. The accumulated household savings cushion is being spent down and should be nearly exhausted just as student loan payments are set to restart.

Forward economic indicators drop to rarely visited levels

New orders for manufacturing and services (left axis) and U.S. leading economic indicators (right axis).

Sources: Institute for Supply Management and The Conference Board.

Central bankers ignore the shift in the labor market

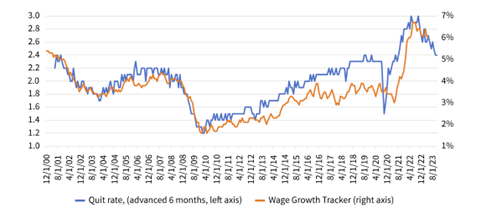

Globally, monetary policymakers in the major developed markets continue to see inflation as their biggest worry. In June, both the Reserve Bank of Australia and the Bank of England increased their policy rates, when most economists had expected a pause. The Bank of Canada restarted hiking after having already paused. In Congressional testimony recently, Chair Powell hinted that the Fed may still need two more hikes to get to "sufficiently restrictive." The key worry for financial markets, as we see it, is that the major central banks are running policy while looking in the rearview mirror. While it is of course true that core inflation has been and continues to be frustratingly sticky above 4%, the Fed — which has declared it is no longer in the forward-guidance business — is ignoring ample evidence that the labor market is weakening. Two key leading indicators of wage inflation — the four-week moving average of new weekly claims for unemployment insurance and the quit rate from the JOLTS data — are both back to pre-pandemic levels. The Fed may not have the luxury of operating as a "single mandate" central bank for much longer. If the monthly payroll data begin to show cracks, then risk assets will be quick to price in the possibility of a policy mistake.

Key labor market indicators are rolling over

The quit rate from JOLTS survey is at pre-pandemic levels, and wage growth is declining.

Sources: U.S. Department of Labor (JOLTS Quit Rate) and Federal Reserve Bank of Atlanta (Wage Growth Tracker).

The cost of missing out on brief spurts of risk-on market sentiment like we saw in May and June is lowered in the current environment, where returns on cash in short-dated duration instruments are at their best levels in almost two decades. It wasn’t necessarily true in a world of zero-interest-rate policy, but today, patience is a virtue.

1. A great movie, to be sure, but also shorthand for Apple, Microsoft, Alphabet, Amazon, NVIDIA, Tesla, and Meta Platforms, which collectively represent a whopping 25% of the Russell 1000 Index (and which were originally nicknamed FANGMAN, then FANG+).

2. Remember the terms "B2B" and "B2C"? Did you keep notes on your PalmPilot?

3. nytimes.com, "Notions of New Economy Hinge on Pace of Productivity Growth," September 3, 2001; economist.com, "A Spanner in the Productivity Miracle," August 9, 2001.

This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon as research or investment advice regarding any strategy or security in particular.

This material is prepared for use by institutional investors and investment professionals and is provided for limited purposes. This material is a general communication being provided for informational and educational purposes only. It is not designed to be investment advice or a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. The opinions expressed in this material represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the material. Predictions, opinions, and other information contained in this material are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

This material or any portion thereof may not be reprinted, sold, or redistributed in whole or in part without the express written consent of Putnam Investments. The information provided relates to Putnam Investments and its affiliates, which include The Putnam Advisory Company, LLC and Putnam Investments Limited®.

For informational purposes only. Not an investment recommendation.

This material is provided for limited purposes. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument, or any Putnam product or strategy. References to specific asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations or investment advice. The opinions expressed in this article represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the article. Predictions, opinions, and other information contained in this article are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

Diversification does not guarantee a profit or ensure against loss. It is possible to lose money in a diversified portfolio.

Consider these risks before investing: International investing involves certain risks, such as currency fluctuations, economic instability, and political developments. Investments in small and/or midsize companies increase the risk of greater price fluctuations. Bond investments are subject to interest-rate risk, which means the prices of the fund's bond investments are likely to fall if interest rates rise.

Bond investments also are subject to credit risk, which is the risk that the issuer of the bond may default on payment of interest or principal. Interest-rate risk is generally greater for longer-term bonds, and credit risk is generally greater for below-investment-grade bonds, which may be considered speculative. Unlike bonds, funds that invest in bonds have ongoing fees and expenses. Lower-rated bonds may offer higher yields in return for more risk. Funds that invest in government securities are not guaranteed. Mortgage-backed securities are subject to prepayment risk. Commodities involve the risks of changes in market, political, regulatory, and natural conditions.

Our investment techniques, analyses, and judgments may not produce the outcome we intend. The investments we select for the fund may not perform as well as other securities that we do not select for the fund. We, or the fund's other service providers, may experience disruptions or operating errors that could have a negative effect on the fund. You can lose money by investing in a mutual fund.

In the United States, mutual funds are distributed by Putnam Retail Management.

Putnam Retail Management

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Putnam

Read more commentaries by Putnam