We continue to watch the fascinating developments in Russia. While the coup has failed and Yevgeny Prigozhin is either in exile or meeting a worse fate, the reality of the situation is that Russia is on a path to internal strife. These events were eminently predictable. In fact, my team and I have been predicting them since day one of the Russian invasion in Ukraine. Here is what we said in a February 24, 2022 analysis:

Russian history is replete with examples of how aggression does not pay dividends for the country. The same advantages that have afforded Russia a near perfect record when playing defense – a vast expanse into which it can withdraw almost endlessly – make it difficult to project power over a long period of time. Ukraine itself is a large country. Although it neighbors Russia, supporting troops that far into hostile territory will be challenging.

Over the past 200 years, almost every Russian war of aggression has therefore ended in a bungled, embarrassing, tragedy that then bore fruits for a revolution.

Policymakers are not always aware of their material constraints. They may misjudge them. Or they may completely ignore them, irrationally. As such, the constraint-based framework is not always right, initially. However, if our assessment of the material constraints facing Russia in Ukraine is correct, then there will be consequences for President Putin for having misjudged them.

We reiterated this forecast in a recent commodity analysis as well, positing that internal strife in Russia would be one of the critical geopolitical risks that provide a tailwind for commodities:

Russian destabilization: The war in Ukraine has been a disaster for Russia militarily, geopolitically, and potentially – in the near future – politically. Domestic political insecurity could create an environment unconducive to capital investment – to put it mildly. Regime change could create complete chaos in the world’s largest exporter of commodities. This could lead to a severe decline in production. Russia has already announced oil production cuts amounting to 6.7% of its exports. While these cuts are flagged as retaliation for Western sanctions, that may simply be rhetorical cover for problems with maintaining production given a lack of Western technology and knowhow.

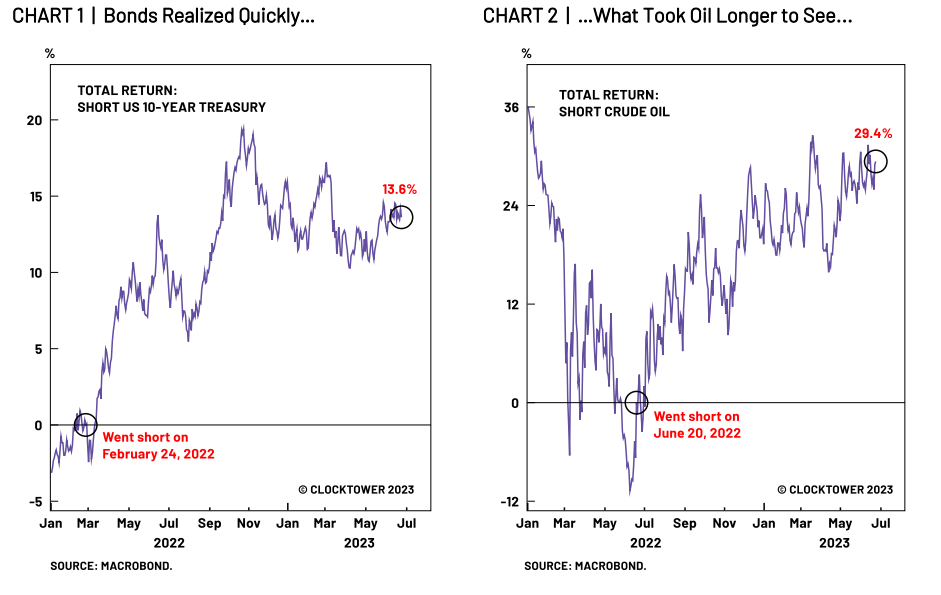

One thing investors should learn from the ongoing conflict is that second and third order effects are difficult to predict, but are critical for markets. Lots of people predicted Russia’s invasion into Ukraine correctly. We didn’t. But, once the invasion happened, we shorted bonds immediately – a controversial, to put it mildly, trade recommendation given their supposed safe haven status (Chart 1) – shorted oil in June 2022 – also a controversial recommendation given the long oil consensus at the time (Chart 2) – and then went long EUR and European industrials in September 2022 – ditto on the controversy given the massive, and really idiotic, consensus that Europe would de-industrialize as result of the war (Chart 3).

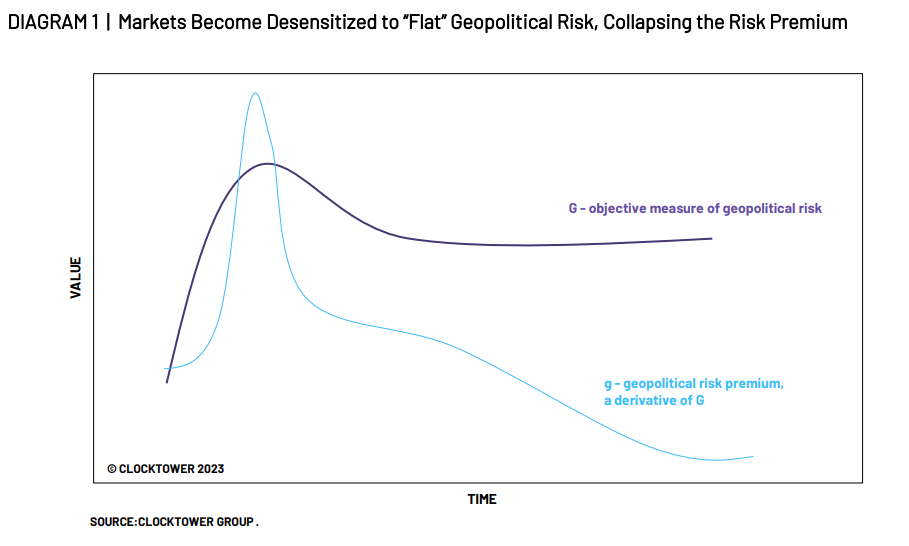

Each of these calls relied on our instinct to fade first order effects – whose effect on markets is known by experienced investors to be fleeting (Diagram 1) – and focus on the second and third order effect.

Missing a first-order effect is like missing a shot in basketball. Even the best shooters will only hit around 55% of their shots. The question is what you do after you miss the shot. To be able to forecast second and third order effects, you must have a framework. We do. It is elucidated in Geopolitical Alpha and it works.

President Putin ignored his material constraints and has been paying the price for it ever since the day one of the invasion. It’s why the bond market ignored the silly nuclear threats, why oil prices collapsed when investors realized there was no risk to supply, and why European assets skyrocketed as the paucity of Putin’s gamble was revealed. Every step of the way, material constraints were right, and Putin was wrong for ignoring them. He is now reaping what he sowed and what we predicted would happen in a Bloomberg interview at the onset of the war. His regime is on shaky ground, with the Kremlin no longer satisfying the basic tenet of sovereignty: monopoly over the legitimate use of force in a given territory.

Where do investors go from here? Markets are unlikely to open on Monday with any perceptible reaction to the coup attempt. Oil may rally, but we believe that the imminent Chinese stimulus and the ongoing strength of US economy – despite all the doom and gloom recession calls – are far more relevant to oil prices and commodities than short term political machinations within Russia.

While we remain sanguine on the issue of the war in Ukraine and believe that both sides are exhausted and unlikely to make headway, the geopolitical alpha is no longer available to be harvested. The “easy wins” are gone. Geopolitical risk premium does not appear to be embedded anywhere. As such, the risk skew is to the downside – particularly for European assets – even if we are sanguine on geopolitics. With nary a geopolitical risk premium anywhere in the market, it is difficult to find ways to fade the hysteria. We are therefore cautious in this eminently unpredictable moment. While we believe that the odds of Putin declaring victory in Ukraine are rising so that he can consolidate his regime at home, he may disagree with us. As such, we need to watch carefully for three data points:

-

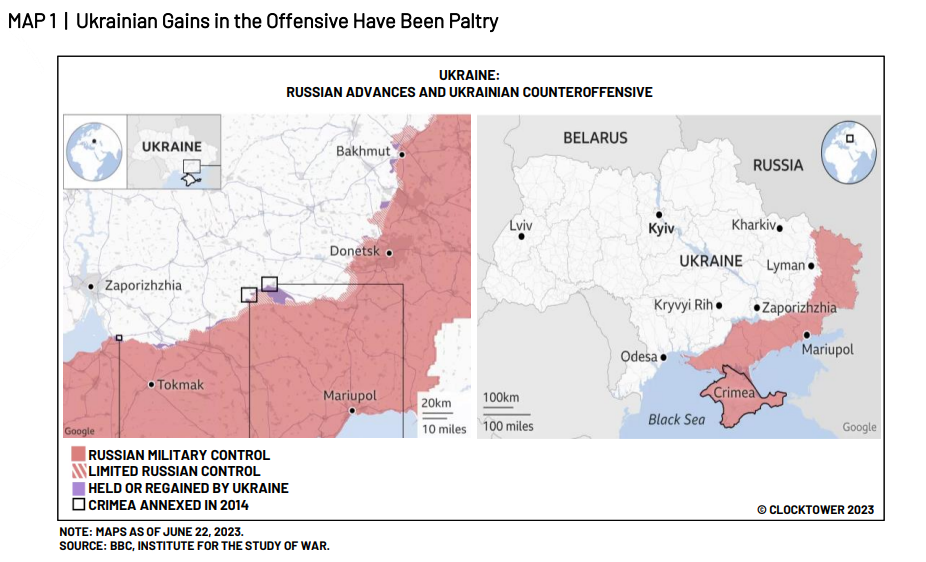

Russian esprit de corps: Far more important than any “order of battle” analysis that lists tanks and guns quantitatively is the psychological state of Russian troops. Our readers should remember the speed with which Taliban overwhelmed US-trained Afghanistan military, or the speed with which ISIS did the same in Iraq. It is now June 26, 2023. The gains of Ukrainian offensive are paltry (Map 1). If the Wagner mutiny has impacted Russian moral negatively, the Ukrainian gains over the next four weeks will be non-linear and dramatic.

-

Domestic narrative: Prigozhin accused the Kremlin of subverting Russian national interests by bungling an invasion into Ukraine. More than that, he accused Russian elites of pursuing a war for domestic political reasons. This is an extraordinary line of attack, but one committed by a nationalist mercenary with a brutal reputation. Prigozhin cannot be dismissed as some liberal, NGO, leader sitting in a comfortable St. Petersburg office and feasting on Western handouts. Investors should watch whether more “patriots” (read: hawks and nationalists) flock to his thesis. This will force Putin to reconsider the war, lest he gets outmaneuvered on the right.

-

China’s response: Beijing policymakers have already spoken to Kremlin elites, as reported by the media. Regime change in Russia is not in China’s interest. Russian regime change has, in the past, led to 180-degree foreign policy turns. Who can forget Lenin leaving France and the UK in a lurch by abandoning the Eastern Front. Or Gorbachev, and later Yeltsin, simply ending the Cold War. We expect China to put pressure on Russia to end the war, not double down on supporting the failed offensive in Ukraine.

As our readers can tell, we continue to lean towards the war in Ukraine being a non-market event, a view we have now held for an entire year. We fear that our view is fully in the price. As such, risk is that we are wrong.

Over the long term, the political crisis inside Russia will be a much bigger macro event for investors than the war in Ukraine. The obvious implication, for long term investors, is to position for a commodity super cycle. But the level of risk will vary greatly. Russian regime change could take the civilized, gentlemanly, route, with President Putin being replaced the way his predecessor Yeltsin was. With multiple guarantees to himself and his family. Or, Russia could devolve into a Mad Max: The Road Warrior route of instability. The permutations of those two options are so wide that it is difficult, at this point, to see clearly which route the future will take.

Disclaimer

This Report is proprietary and confidential and may not be copied, quoted, referenced, or distributed in any format without the express written approval of Clocktower Group (“Clocktower”). Any violation of the foregoing may result in material harm to Clocktower. The views expressed reflect the personal views of the members of Clocktower’s Strategy Team and do not necessarily reflect the views of Clocktower. Views expressed are as of the date hereof and Clocktower does not undertake to advise you of any changes in the views expressed herein. Opinions or statements regarding financial market trends are based on current market conditions and are subject to change without notice. References to a target portfolio and allocations of such a portfolio refer to a hypothetical allocation of assets and not an actual portfolio.

The views expressed herein and discussion of any target portfolio or allocations may not be reflected in the strategies and products that Clocktower offers or invests. It should not be assumed that Clocktower has made or will make investment recommendations in the future that are consistent with the views expressed herein or use any or all of the techniques or methods of analysis described herein in managing client or proprietary accounts.

Clocktower does make any representation or warranty, express or implied, as to the accuracy or completeness of the information contained in this Report and nothing contained herein shall be relied upon as a promise or representation whether as to the past or future performance. The information contained herein should not be relied solely upon by any party in connection with any investment in any fund or investment vehicle managed by Clocktower. Certain factual information contained herein has been obtained from third-party sources. It has not been independently verified by Clocktower and although Clocktower believes it to be reliable, Clocktower makes no representation as to its accuracy or completeness.

This Report is intended solely for informational purposes. It is not investment advice and should not be considered to be a recommendation to buy or sell any types of securities or investments or as an indication that any security listed in this Report is suitable for a particular person. Any such offering would be made only to accredited investors and only by a term sheet, confidential private placement memorandum or similar offering document (“Offering Documents”). Before making an investment decision with respect to any private fund, potential investors need to carefully read the Offering Documents, and also consult with their tax, legal and financial advisors.

The investments described herein involve a high degree of risk, including the loss of principal investment. There can be no assurance that investment objectives will be achieved or that investors will receive a return of their capital. In addition, investment results may vary substantially on a monthly, quarterly or annual basis. Clocktower and its affiliates also may have potential conflicts of interest, including that some of Clocktower’s officers, directors and/or employees may be investors in the securities directly or indirectly. No assurance can be given that any risk management framework described herein will achieve its objective.

This Report contains statements and information that is not purely historical in nature. These include, among other things, assumptions, expectations, intentions and beliefs about future events. All of these statements and information are intended as “forward-looking statements”. These forward-looking statements are identified by their use of the terms and phrases, such as “believe,” “may,” “should,” “intend,” “expect,” “anticipate,” “project,” “estimate,” “predict,” “scheduled,” and similar expressions and phrases. Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause actual results to be materially different from those described. Clocktower Group is an SEC-registered investment adviser and information regarding the services provided and fees charged, along with other important disclosures is contained in our Form ADV, which can be obtained upon request at 1-310-458-2003 or found at www.adviserinfo.sec.gov

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Read more commentaries by Clocktower Group