Persistent economic uncertainty has been the overwhelming theme of the past 12 months. While the US is not currently in a recession, many economists believe one could be on the horizon. In the meantime, the dual whammy of high interest rates and persistently high inflation is beginning to take its toll on the commercial real estate sector.

Yet, despite headwinds, appetite for real estate remains high. As investors seek alternative real estate assets that can offer preservation of capital and downside protection, the farmland market is increasingly attractive. Below, I break down the factors driving the continued shift among investors toward this asset, and the avenues now available to participate in this market.

Commercial real estate is under pressure

The high interest rate environment has taken its toll on CRE valuations. Interest rates are at their highest level in decades after a series of aggressive rate hikes from the Fed – no fewer than 10 consecutive times between March 2022 and May 2023. These rising rates, combined with general economic uncertainty and the high-profile collapses of SVB, Signature Bank and First Republic Bank have contributed to a tightening credit market for CRE loans. Given the high levels of leverage on commercial real estate, this puts downward pressure on valuations.

Other longer-term trends, like the shift to remote work, also bode ill for segments of CRE such as office. According to Franklin Templeton, office is one of the sectors in greatest danger from these demographic shifts. Office vacancy rates in New York City were at 16.1% in the first quarter of 2023, a record high. Defaults on commercial real estate loans are on the rise, and not even major investors like Brookfield Asset Management are immune.

As traditional real estate sectors underperform, investors are adapting. This has presented an opportunity for alternative real estate options, like farmland, that have outperformed the overall market in recent years.

Why Farmland?

US Farmland represents a $2.9 trillion real estate market. It can offer many of the benefits of other real estate asset classes, including inflation-linked returns and passive income, but with historically lower volatility.

Historical resilience

Farmland has historically performed well throughout economic cycles. The drivers of farmland values are largely uncorrelated with GDP – at the end of the day, the population continues to grow, and people need to eat. On top of that, farmland is a scarce resource, with arable land shrinking year over year.

During the Great Financial Crisis, for example, farmland posted consistently positive returns each quarter. From the fourth quarter 2007 to the fourth quarter of 2009, farmland returns were up nearly 30%, compared to double-digit drops in equity and real estate.

Like all investments, farmland is not risk-free. The value of farmland can fluctuate with changes in commodity prices, weather conditions, and government policies, as experienced in the first two years of the Covid-19 pandemic. In 2020, farmland witnessed more muted returns, with the only negative quarter of growth (-0.1%) in 30 years. However, farmland has rebounded quickly and consistently outperformed other indices in 2022, cementing the asset’s resilience in the face of adverse conditions.

Competitive risk-adjusted returns

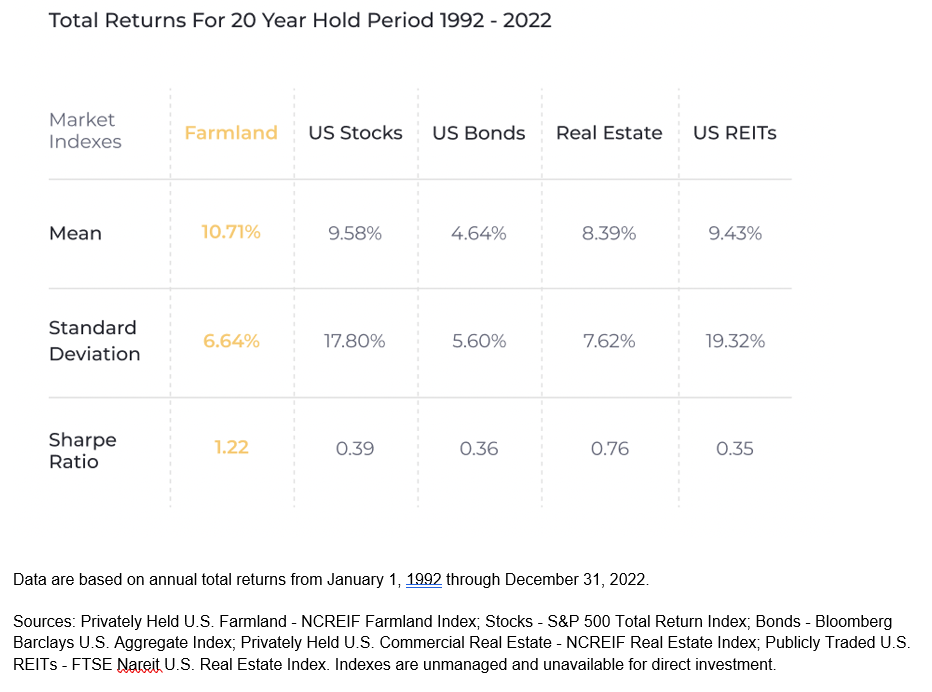

Looking back over thirty years of data, farmland has delivered average annual returns of 10.71% beating out both commercial real estate (8.4%) and the S&P 500 (9.6%), demonstrated in the figure below. This is attractive in its own right, but farmland looks even better on a risk-adjusted basis. The standard deviation of US farmland between January 1992 and December 2022 was only 6.6%, compared to 17.8% in the stock market and 7.6% for commercial real estate.

What this means is that farmland investing has historically offered stronger preservation of capital than both risky assets like equities and more traditional real estate investments. A $1,000 investment in farmland in 1992 would be worth nearly $23,000 in December 2022, compared to only around $15,000 in the stock market.

Low correlation with other assets

A third benefit of farmland, particularly from a portfolio construction perspective, is the fact that the historical performance of farmland is largely uncorrelated with the historical performance of other major asset classes, including stocks, bonds and gold. The benefit of including farmland in a portfolio is that it can help reduce overall portfolio volatility, as well as the downside risk in uncertain economic environments.

Farmland returns are also historically uncorrelated with the returns of commercial real estate, meaning the headwinds currently faced by many segments of the CRE market have not impacted farmland values or performance. Over the past 12 months, farmland has returned 8.9% through Q1 2023. In contrast, real estate has returned -1.2%.

Reliable cash flow and inflation protection

Another benefit of farmland investing is that it can offer investors a reliable source of passive income. The income streams associated with farmland investing are very similar to those of traditional real estate investments: farmland investors can get income from two sources: periodic passive rental income from the operator and appreciation when the underlying asset is sold. A landlord-tenant model is very common for farmland in the US, with close to 40% of farmland currently leased. Like commercial real estate, farmland rental payments are linked to inflation, which can offer investors protection from the runaway inflation in today’s market. From 2020-2022, farmland’s correlation to the Consumer Price Index (CPI) was 0.97, according to research by my firm.

An Untapped Market

Farmland funds have become increasingly popular among institutional investors over the last few decades, with assets under management representing 30% of the total AUM of all food and agriculture funds, second only to private equity at 37%. Today, there are more than 200 farmland funds globally, with an aggregated AUM of $42 billion.

Despite this interest among institutions, investors still own a relatively small percentage of the total farmland market; in the US, investors own just 2% of the country's 900 million acres of farmland, which is estimated to be worth $2.9 trillion. The remaining 98% of the land is owned by family farms, though it's estimated that almost 70% of US farmland will change hands in the next 20 years.

This has created an opportunity for firms looking to capitalize on this real estate sector, while opening the door for individual investors seeking new avenues for portfolio stability. There are now two publicly-traded farmland REITs and a handful of agriculture REITs available to investors. Additionally, there are now a host of farmland investment managers that handle the sourcing, due diligence and operations of institutional-quality farmland offerings, which can be accessed through a variety of products. These products range from crowdfunded offerings (low minimums ranging from $15,000 to $25,000) to funds, which enable access to diversified portfolios of farmland for minimums starting at $100,000.

Despite today’s persistent economic uncertainty, farmland has proven to be a low-volatility, safe haven investment that has historically performed well throughout turbulent economic times.

A message from Advisor Perspectives and VettaFi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Read more commentaries by FarmTogether