The collapse of Silicon Valley Bank and Signature Bank heightens the Federal Reserve's policy dilemma over fighting inflation while maintaining financial stability. We analyze what the crisis means for the banking system and the economy.

- The Federal Reserve's quarterly Senior Loan Officer Opinion Survey (SLOOS) shows credit conditions have continued to tighten and are much tighter than a year ago.

- Cracks in the foundation of small and medium-sized business finances have already begun to appear likely due to credit tightening.

- Companies with lower credit quality, particularly ones that finance themselves predominantly with loans, may continue to see a sharp rise in interest expense, and historical patterns suggest high-yield credit spreads are likely to widen.

We have been longtime fans of the value of the data in the Fed's SLOOS. While it only comes out quarterly, and with a non-trivial lag, it has exhibited solid forward-looking information about credit growth. Also, the data has a long history that is not subject to revisions. The release has historically flown under the radar and tends to not get much attention from the press. However, it is fair to say the May 8 release of the April survey data was the most anticipated publication in the survey's long history.

Lending standards keep tightening

The headline is that while credit conditions continue to show tightness, the deterioration from the prior quarter was less than we would have anticipated. The net percentage of bank loan officers saying they were tightening lending standards for consumer and industrials loans in April was 46%, which compares with 45% in January. But that de minimis quarter-over-quarter change belies the fact that just a year ago, banks were actually easing lending standards.

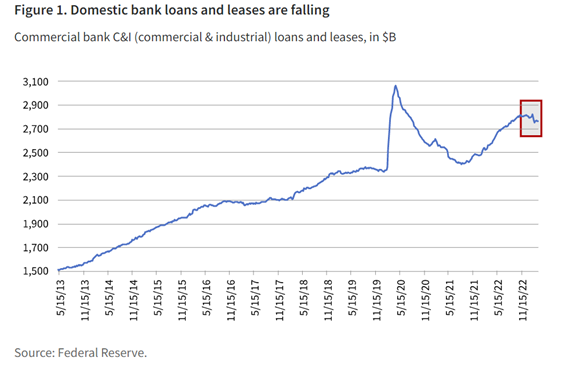

The lending activity starts to slow

As highlighted in the Q2 2023 Capital Markets Outlook, tighter lending standards slow actual loan growth with a lead time of about a year. We would have expected to start seeing credit conditions tighten sometime in the third quarter of 2023, even without a banking crisis. If we add to these conditions the turmoil from a handful of bank failures and continued deposit flight from other banks, it would seem reasonable to expect that contraction in the flow of credit would begin to rear its ugly head. In fact, some signs of these cracks in the foundation of small and medium-sized business finance have already begun to appear. In the Fed's weekly H.8 release (Assets and Liabilities of Commercial Banks in the United States), we can see that it is rare (outside of a public health emergency) for the aggregate nominal dollar level of domestic bank loans and leases to decrease, but that is exactly what has been happening since the end of January.

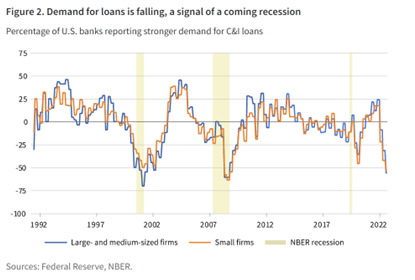

Demand for credit is declining

Potentially more concerning than the deterioration in banks' propensity to lend to a broad swath of borrowers is the fact that demand for credit is also in free fall, coincident with tightening lending standards. While this demand data is not as robust as the headline SLOOS because it goes back only to the early 1990s, it is fairly easy to see in Figure 2 why we should be concerned: The link between falling credit demand and recessions is strong.

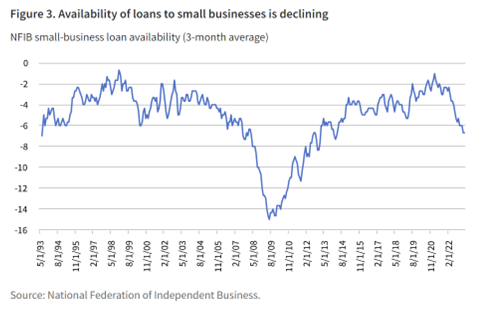

Another example of deteriorating credit conditions can be seen in the National Federation of Independent Business's (NFIB) monthly Small Business Economic Trends survey. This sample survey of 800 companies asks respondents about the availability of loans. It reveals a deterioration in availability since mid-2022.

Signs of a credit squeeze

While it is certainly true that large corporations continue to have access to credit via public capital markets or private credit sources (sometimes called shadow banks), that tends to not be the case for smaller businesses. Those small companies are inconveniently where a large swath of jobs are located. Private business and small and midsize enterprise bankruptcy filings in the U.S. have been steadily rising since late-2022, in stark contrast to the picture painted by credit spreads in public markets. We are closely watching both the Fed's commercial bank lending data and weekly new claims for unemployment insurance for signs of an acceleration in what appears to be a slowly developing credit crunch, or perhaps a slow credit squeeze.

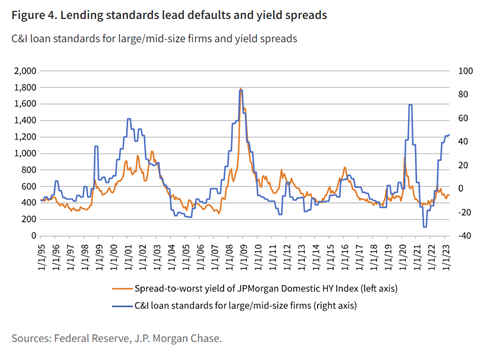

High yield at risk as spreads have remained low

Historically, default rates and then credit spreads follow the SLOOS with a lag (see Figure 4). Companies with lower credit quality, particularly ones that finance themselves predominantly with loans (rather than bonds), will likely continue to see a sharp rise in interest expense because the Fed has hiked the policy rate relentlessly over the past year. That burden on free cash flow will likely continue to pressure the income statement.

Adding to our concern about high-yield bonds, the compensation for credit default risk relative to the available yield on cash is in the bottom decile (in fact, the 6th percentile) of its range when measured all the way back to 1995. Given these conditions, credit spreads need to widen, and investors should prefer to favor higher-quality credit.

This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon as research or investment advice regarding any strategy or security in particular.

This material is prepared for use by institutional investors and investment professionals and is provided for limited purposes. This material is a general communication being provided for informational and educational purposes only. It is not designed to be investment advice or a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. The opinions expressed in this material represent the current, good-faith views of the author(s) at the time of publication. The views are provided for informational purposes only and are subject to change. This material does not take into account any investor's particular investment objectives, strategies, tax status, or investment horizon. Investors should consult a financial advisor for advice suited to their individual financial needs. Putnam Investments cannot guarantee the accuracy or completeness of any statements or data contained in the material. Predictions, opinions, and other information contained in this material are subject to change. Any forward-looking statements speak only as of the date they are made, and Putnam assumes no duty to update them. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties. Actual results could differ materially from those anticipated. Past performance is not a guarantee of future results. As with any investment, there is a potential for profit as well as the possibility of loss.

This material or any portion thereof may not be reprinted, sold, or redistributed in whole or in part without the express written consent of Putnam Investments. The information provided relates to Putnam Investments and its affiliates, which include The Putnam Advisory Company, LLC and Putnam Investments Limited®.

A message from Advisor Perspectives and VettaFi: To learn more about this or other topics, please check out our most recent white papers.

© Putnam

Read more commentaries by Putnam