Hong Kong’s currency and financial stability are not under immediate threat.

Hong Kong has earned some unenviable headlines in the last four years, from unrest triggered by the National Security Law to the city’s stringent COVID control measures. The bad news continues to pile on for the city, most recently in currency markets.

Pegged in a band of HK$7.75–7.85 per U.S. dollar, the Hong Kong dollar (HK$) is generally a stable currency. But ever since the U.S. Federal Reserve started hiking rates in March 2022 to tame inflation, the local currency has been trading at the weak end of its target band. This has raised renewed concerns over the dollar peg and its economic implications.

A stable currency is considered an anchor for financial stability in an open economy like Hong Kong, where trade and logistics are key drivers. The Hong Kong dollar has a predictable value and is easily convertible, contributing to the city’s dominance as a global financial hub.

Hong Kong’s monetary policy has been run in lockstep with the Fed for four decades. This requires the Hong Kong Monetary Authority (HKMA), the city’s central bank, to intervene in the currency markets by selling or buying every time the domestic currency falls or rises beyond the band.

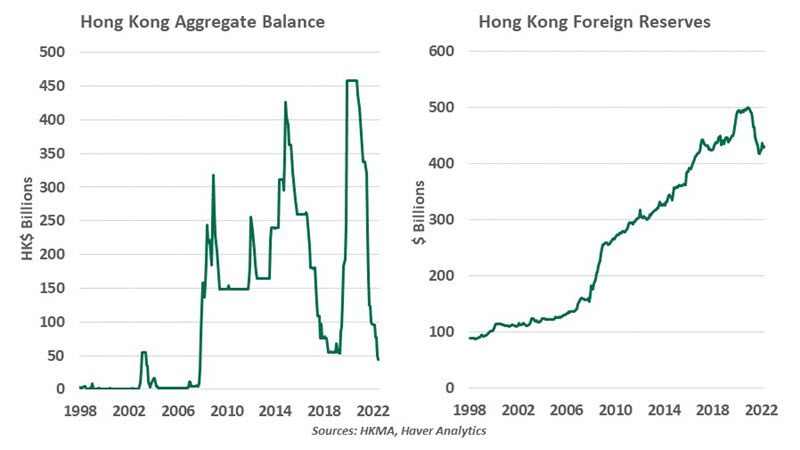

The HKMA has bought about HK$47 billion to support the local currency this year, after having deployed over HK$240 billion in 2022. In total, over 40 interventions have been required to keep the currency at its peak. The aggregate balance (a measure of liquidity in the banking system) has tumbled from HK$320 billion to below HK$50 billion in the past year, the lowest level since the 2008 financial crisis.

Despite the use of so much liquidity, HKMA’s move didn’t drive up local borrowing costs amid weak loan demand. As a result, the gap between the overnight rates in the U.S. and Hong Kong widened to 200 basis points earlier this year, from near parity last November. The deep discount invited carry trade strategies, where investors borrow at lower rates to invest in more lucrative markets, which added pressure on the HK$.

A drought of initial public offerings (IPO) activity last year on Hong Kong’s exchange further dampened demand for Hong Kong dollars. The number of new stock listings fell off a cliff, witnessing a 74% year-on-year decline to HK$73.2 billion in the first nine months of 2022.

Consistent with global trends, IPO proceeds in Hong Kong declined by 50% year to date compared to the first quarter of 2022.

Macroeconomic and geopolitical factors have also been at play. Hong Kong’s economy has struggled under stringent COVID controls in recent years, while its alignment with China has deepened. This has prompted concerns that Hong Kong will lose some of its standing as a global financial center, contributing to an outflow of talent and investments.

Hong Kong’s dollar peg is under stress, but not under threat.

Removal of COVID-related restrictions has led to visible improvements in activity and cross-border travel this year. This should help ease pressure on the HK$. The number of public offerings has increased slightly, signifying the city’s resilience in challenging times. A further rebound is in store. Hong Kong continues to have a healthy IPO pipeline, with over 90 active applicants at the end of the quarter. Even if the aggregate balance were to drop to zero, the city’s central bank can mobilize its second line of defense: $430 billion in foreign exchange reserves to support the peg.

Over the course of the past few weeks, Hong Kong’s overnight funding costs have surged to their highest since 2007 as the HKMA continues to purchase local dollars to dry up liquidity. This has led to a strengthening of the HK$.

Evolving global circumstances are presenting a new set of challenges for Hong Kong. But neither the city’s financial stability nor the stability of its peg is under immediate threat. Hong Kong is likely to remain the city that connects the East and the West.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and Vetta Fi: To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust