A wage-price spiral isn't imminent in Europe, but inflation may take a while to descend.

Inflation readings from the United States have raised hopes that the worst is over and further relief for American households is in the pipeline. For consumers across the Atlantic, however, getting a respite from the high cost of living might take a little longer.

After peaking at 10.6% year over year last October, annual inflation in the 20-member euro currency union decelerated to 7.0% in April. However, a look beneath this encouraging headline figure shows a long journey ahead to bring inflation under better control.

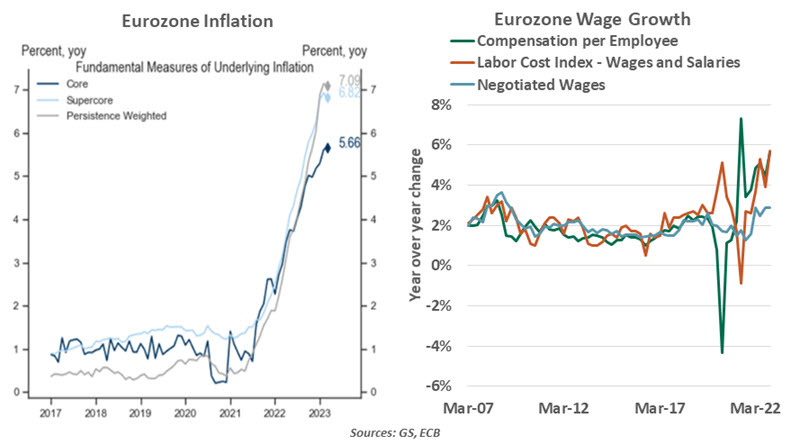

The slump in energy prices has been the primary driver of lower headline inflation readings, as Europe’s natural gas crisis has eased. Core inflation, which strips out energy and food, has steadily ascended to record levels. The super core measure, which consists of items that are sensitive to the business cycle or the output gap, has also risen to a record rate of 6.3% year over year. While there are signs that prices of non-energy industrial goods are falling, services inflation (the single largest component) has reached an all-time high. Inflation is particularly elevated in labor-intensive categories such as hospitality.

Wage growth is increasingly the main driver of underlying inflation in the eurozone amid still-tight labor markets. The contribution of wages to inflation is about twice as large as in 2019-20, a period of stable prices and weak pay gains. Hourly labor costs in the eurozone rose by a record 5.7% in the fourth quarter from a year earlier, exceeding the pace of wage gains in the U.S. The European Central Bank’s (ECB) indicator of negotiated wages has also started to catch up. Recently, German trade union Verdi agreed to a two-year pay deal that would boost the wages for about 2.5 million public sector workers by over 5% in 2023, double the 2.6% increase seen in 2022. In Belgium, many workers received a 10% pay increment.

Europe’s inflation challenge goes beyond wages. Among other factors, the faster pass-through from energy to core inflation is also contributing to higher underlying price pressures.

The sustained strength and breadth of the core component are fanning fears that inflation could become more entrenched and make the task of bringing inflation down to the 2% target a drawn-out process. After hiking its policy rates by 25 basis points at this week’s meeting, the ECB is likely to follow with another hike in June. In addition to raising rates, the ECB is also mopping up some of the €7 trillion worth of liquidity it poured into the financial system over the past eight years.

European inflation may take a while to descend.

European governments have a role in the fight against inflation. With a recession avoided and labor markets still tight, phasing out remaining energy relief measures and other targeted support would be a good starting point to tighten fiscal policy. A more constrained fiscal stance will help the central bank meet its inflation target at lower terminal rates. At the same time, it would lower debt service costs and bolster financial stability among vulnerable member states.

A wage-price spiral isn’t imminent. The ECB’s Persistent and Common Component of Inflation measures has been easing in recent months. The impact of recent aggressive tightening is starting to feed through. Lending conditions have been tightening; the demand for loans contracted sharply for firms in the second quarter, at the second fastest pace since early 2009. Growth momentum has weakened, which will start to cool labor markets and in turn, weigh on overall wage growth.

Negative base effects will have a role in the path of core inflation, too. All else equal, even a steady increase of 0.2% month over month will bring the core annual rate of inflation down to 4.0% by the end of the year.

The sticky nature of price and wage inflation represents a sticky wicket for European policymakers, firms, and households. Hopefully, the pitch will clear soon.

Information is not intended to be and should not be construed as an offer, solicitation, or recommendation with respect to any transaction and should not be treated as legal advice, investment advice, or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulations. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

To learn more on this and other topics, check out our full schedule of upcoming CE-approved virtual events.

© Northern Trust

Read more commentaries by Northern Trust