We favor high yield bonds and natural resource stocks as inflation still shows persistence, earnings expectations deteriorate and worries mount over a stalling U.S. economy.

OUTLOOK

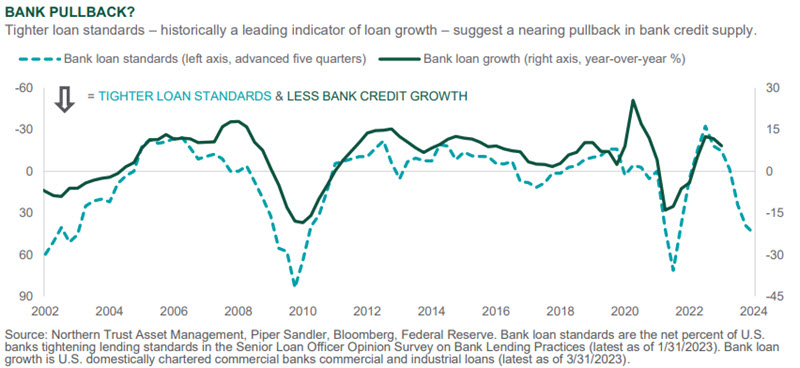

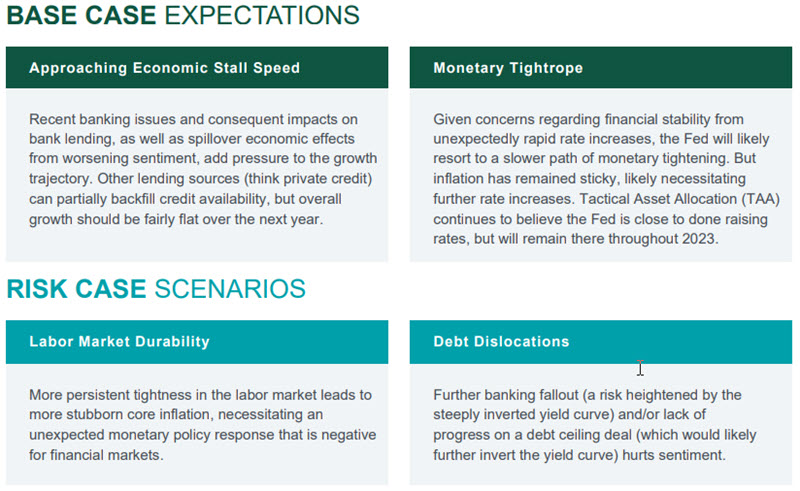

Banking system concerns of a month ago have largely faded following liquidity support from the Federal Reserve and the passage of time without further failures – though not without consequence. The extension of credit from smaller regional banks is likely to decline (see chart below), and while brief, the period of instability adds to preexisting angst among businesses and consumers regarding the likelihood of recession. Despite this backdrop of softening growth expectations, the abating of systemic concerns drove gains in equity markets to levels approaching the prior highs for the year.

Inflation readings in March continued to moderate with headline Consumer Price Index (CPI) declining to 5.1% from 6.0%, but core inflation measures followed most closely by the Fed have failed to show the same degree of improvement. The core CPI reading for March (5.6%) actually inched up slightly from February as we await the expected upcoming turn lower in the data from areas like housing. The Fed and European Central Bank (ECB) both moved rates higher in the past month, with the markets pricing in just one more move for the Fed, while the ECB is expected to continue hiking until mid-year. Increasing risk of a mild recession in the U.S. is likely to limit the magnitude of the Fed’s rate hike cycle to perhaps one or two more moves, though we expect a longer plateau at the terminal rate than current market expectations (which show the Fed cutting rates before the end of the year).

Gains in equities this year against a backdrop of falling earnings expectations have led to valuations that provide limited upside in the base case. With our view that any possible recession in the U.S. will be shallow and short-lived, we see better risk/reward in high yield bonds than in U.S. equities at current pricing levels.

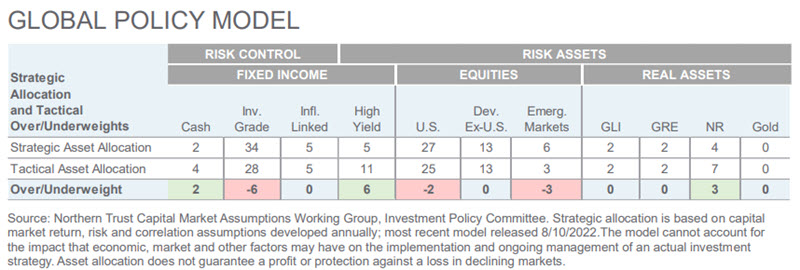

As a result, we increased our overweight to high yield bonds in our Global Policy Model (GPM) this month, funded by moving U.S. equities to a modest underweight. In addition, we went further underweight emerging market equities on a more sluggish economic reopening in China, as well as continued geopolitical issues limiting valuations. The proceeds went to global natural resources, where we see attractive valuations and supply-side discipline supporting prices. Looking forward, market volatility should be expected to remain elevated as the trajectory of growth and inflation remain uneven.

INTEREST RATES

- Investors have flocked to money market funds for income as central banks have lifted short-end rates.

- With yields at 4.5%+ and elevated financial market volatility, the front end of the yield curve is attractive.

- We are modestly overweight cash and underweight IG fixed income as we await opportunities to deploy risk.

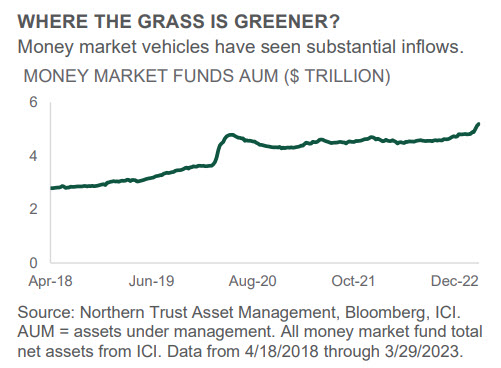

While the entire Treasury yield curve has experienced continued volatility over the past month, nominal yields on U.S. Treasuries maturing in one year or less remain the highest on the entire yield curve. This dynamic has presented front-end investors with yield opportunities not seen for well over a decade, and money market mutual funds (MMFs) have risen to the occasion. The combination of yields over 4.5% and ability to purchase or redeem shares the same day have drawn investors into these products recently. As investors reallocated their assets and portfolios in the wake of stress in the banking system, MMFs saw substantial inflows. In the first three weeks (March 8-29) following the escalation of the Silicon Valley Bank situation, MMF assets under management grew by over $300 billion to a record $5.2 trillion.

We continue to prefer the front end of the yield curve, with a small overweight to cash and a notable underweight to the longer-duration investment grade (IG) fixed income. We expect the Fed to raise rates at least one more time before going on an extended hold. The aforementioned 4.5%+ yields make for an attractive “parking spot” for assets in a diversified portfolio as we await opportunities to deploy risk – either out the yield curve or into risk assets.

CREDIT MARKETS

- Secured bond exposure in the single-B cohort has nearly doubled over the past few years.

- This is one of several factors that suggest high yield is of higher quality versus prior episodes of credit stress.

- We increased our overweight to high yield where we see strong risk/reward at current valuations (8% yield).

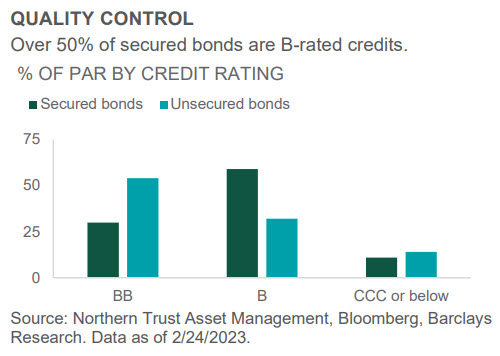

With elevated concerns around growth and added uncertainties from banking turmoil, investor skepticism on credit quality has been on the rise. Moreover, bank lending conditions have tightened to levels historically related to higher forward default rates and spread widening. With that said, the increased quality of high yield – across several factors – keeps us constructive. Measured by credit rating, ~50% of the index is comprised of BBs and only 11% CCCs (versus long-term averages of 43% and 15%, respectively). Another aspect of increased quality is an increase in the proportion of secured bonds, which now make up ~30% of high yield versus 20% a few years ago.

The secured bond cohort is focused in the single-B credit rating bucket (see chart), where secured bond exposure has nearly doubled from a few years ago. This implies that asset coverage within the single-B cohort is stronger than historical standards, which should support valuations compared to previous examples of credit stress. Other factors of stronger credit quality include long maturity runways and higher earnings with more diversified revenue streams. We increased our overweight to high yield given its attractive income yield (~8%) and our view that fundamentals will help limit the extent of any defaults.

EQUITIES

- Earnings expectations are bleak due to pressures from stall-speed economic growth and sticky inflation.

- In this slow-to-no-growth environment we expect earnings growth will contribute little to equity returns.

- Given diminished upside we went underweight U.S. equities (richly priced after a strong start to the year) and further pressed our EM equity underweight.

Global equities bounced back from the banking stress-induced decline in February, rising roughly 5% over the past month. It now seems increasingly likely that the failures of Silicon Valley Bank and Credit Suisse were mostly idiosyncratic events as far as the risk of a wider banking crisis is concerned. However, that doesn’t mean there won’t be an impact on the broader economy through lower demand and supply of credit. In fact, as the Fed downshifted to a 25-bp interest rate hike, it acknowledged that tighter financial conditions might be doing some of the inflation-fighting work for them and some caution is warranted in the face of this new source of uncertainty. Growth stocks again outperformed value as interest rates moved even lower. In terms of regional performance, the U.S. led, followed by emerging markets (EM) and Europe.

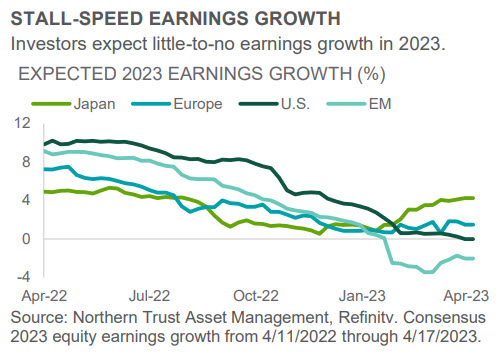

Looking ahead toward the upcoming earnings season, it is clear that the market expects a continued decline in corporate earnings due to margin compression and revenue headwinds (see chart). The magnitude of those headwinds will be important to watch and we are somewhat cautious in our own assessment. As a result, we decided to lower our U.S. and EM equity positions in favor of high yield corporate bonds and natural resources.

REAL ASSETS

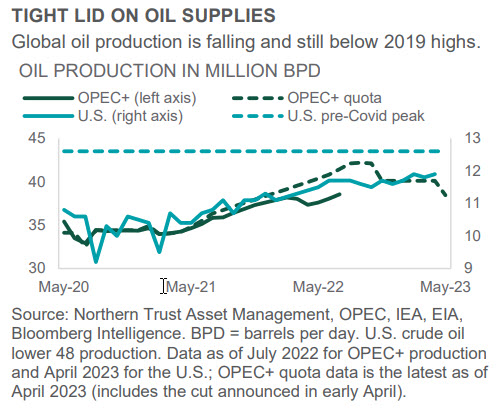

- OPEC+ production cuts have defended oil prices amid stalling economic growth that’s lowering demand.

- We see upside risk to oil prices on the basis that tight supply dynamics will more than offset weaker demand.

- We increased our natural resources overweight with EM equities as the funding source given supply and valuation supports we expect will offset slower growth.

Despite slowing economic growth and (slowly) falling inflation, we increased the natural resources allocation in our Global Policy Model. Behind this (seemingly counter-intuitive decision) is our expectation that oil demand may be capped, but oil supply will likely be capped even more. In a strategic move, OPEC+ recently cut quotas to protect price over market share partly based on a belief that the U.S. – the swing producer for much of the past decade – won’t make up the difference. It’s a good bet. All but the best U.S. wells are seeing production slip as they age, just as logistical challenges and less-friendly regulators have led to fewer new wells being drilled to offset the losses.

The nearby chart shows OPEC+ production in relation to current OPEC+ quotas as well as U.S. production versus the U.S. pre-pandemic high. The net result is an oil price around $80/barrel with a floor underneath it (in the case of shallow recession) and upside above it (should central bankers achieve a soft landing). Thus, the natural resource asset class looks attractive – especially given still-cheap valuations (current price-to-earnings of 6.7x versus a median of 14.7x the past decade). And a better investment than our funding source, emerging market (EM) equities, which are also cheap but without the same asymmetry.

- Chris Shipley, Chief Investment Strategist – North America

IN EMEA AND APAC, THIS PUBLICATION IS NOT INTENDED FOR RETAIL CLIENTS

© 2023 Northern Trust Corporation.

The information contained herein is intended for use with current or prospective clients of Northern Trust Investments, Inc. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Forward-looking statements and assumptions are Northern Trust's current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information. Investments can go down as well as up.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited.

© Northern Trust

Read more commentaries by Northern Trust