Up until recently, crude oil inventories saw continued build after build, suggesting the real time supply and demand dynamics in the market have been tilted toward the bearish side of the ledger. Unsurprisingly, oil prices and energy related equities have suffered, continuing their drawdown and consolidation from the early 2022 peak. As it stands, oil prices have corrected roughly 40%, and although energy stocks as a group have also come off a little, it has been to a far lesser extent, with the XLE ETF currently priced around 13% below its highs. Either way, these outcomes have been far from ideal for investors.

Given the efforts of the Biden administration to bring down energy prices by opening the SPR floodgates and the constant lockdowns of the worlds largest manufacturing economy in China for much of the past couple of years, such a correction should hardly be surprising. However, the tides may now be changing. Indeed, the energy markets look to have taken a bullish turn over the past couple of weeks. While the ultimate bottom for oil prices may not yet be in for this cycle, it is seemingly drawing near. Let’s dig in.

Physical Market

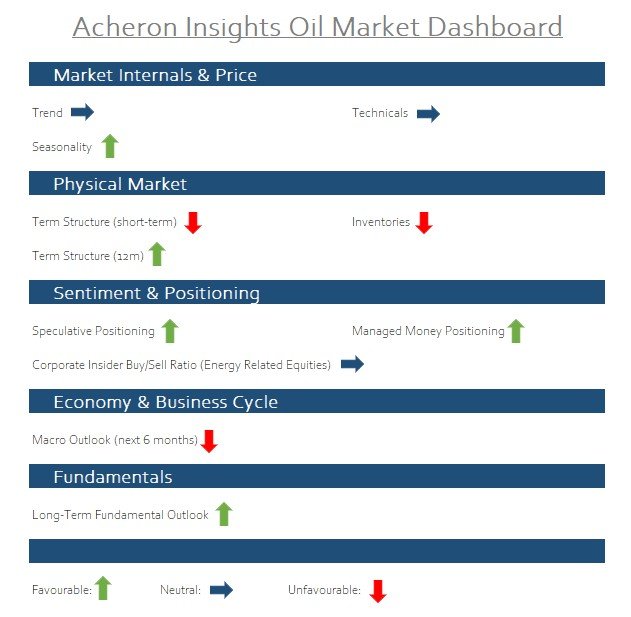

As ever, I will assess the outlook for the oil market through the lens of the physical market, the supply and demand dynamics, positioning and sentiment, as well as the macro-outlook and market technicals.

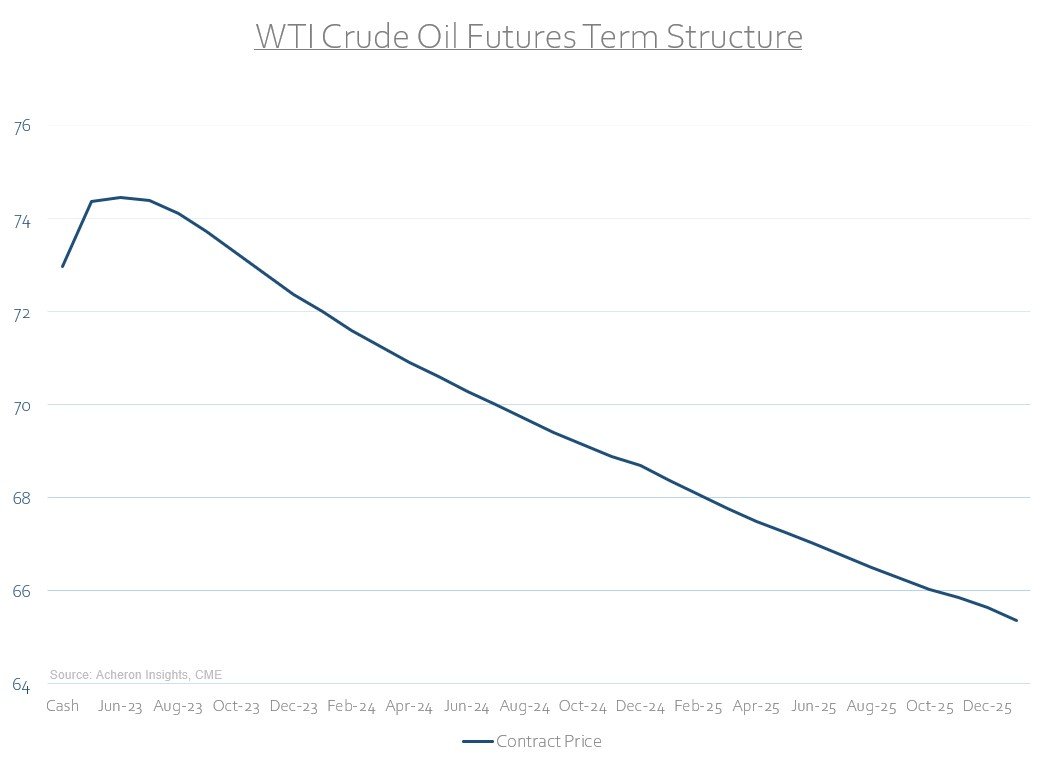

Beginning with the former, a very useful indicator that provides a view into the dynamics within the physical market - which is integral to a commodity that is priced via the marginal barrel, such as oil - is the shape of the futures term structure.

Generally, when the further dated contract prices are trading at a discount to the spot and short-dated contracts, and the market in thus in backwardation, this implies there is a supply deficit as market participants are willing to pay a premium for instant delivery. As a result, any deficit will need to be met via drawing down inventories. Though backwardation incentivises drawdowns of oil inventories, it does not incentivise producers to increase production and capacity, as they would be forced to sell forward new production at a lower cost than today.

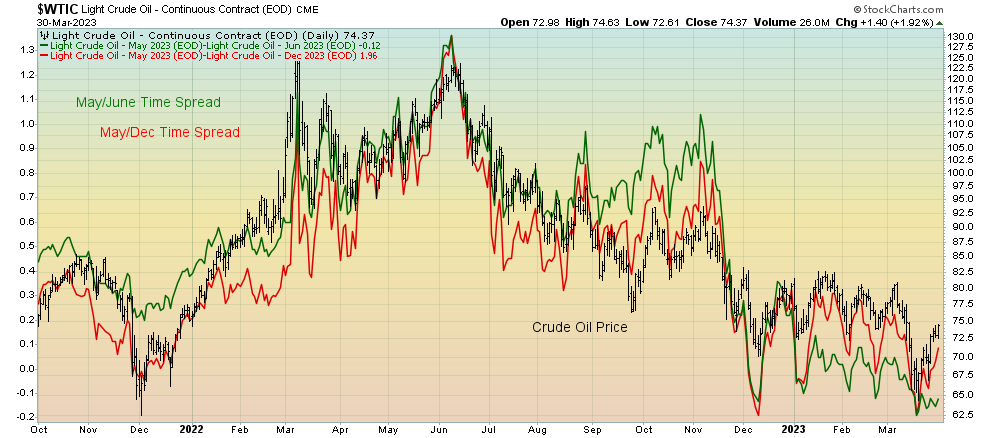

As we can see below, the short-dated time spreads (i.e. the first month futures contract relative to the second and third month contracts) are now in contango, while the longer-dated spreads remain in backwardation, as they have done for much of the past couple of years.

Ideally, we would like to see backwardation across the entire curve, with the short-dated time spreads confirming the recent highs in spot prices in the manner that the longer-dated spreads have done so, as we can see below. As such, we can infer that the structural tightness in the market remains, but there may still be some potential for further short-term downside.

Inventories

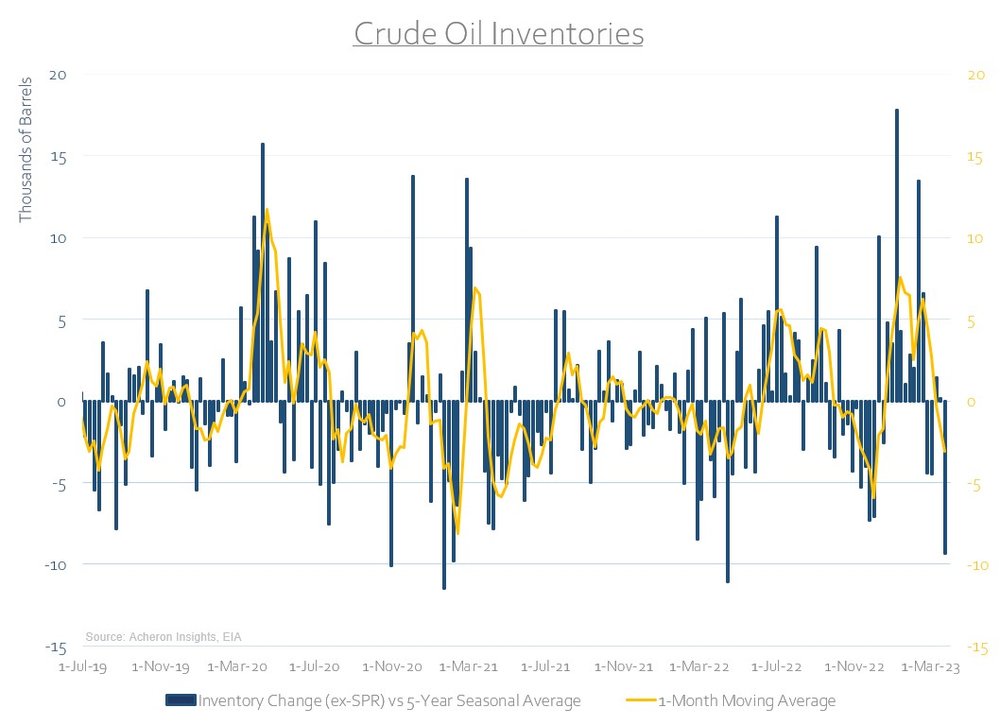

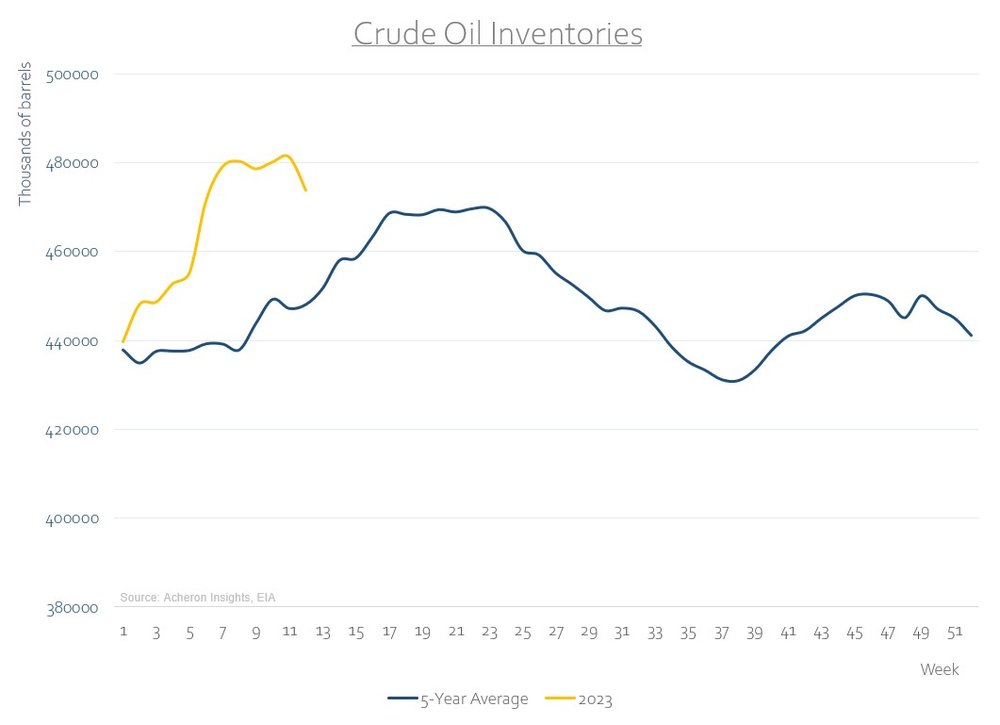

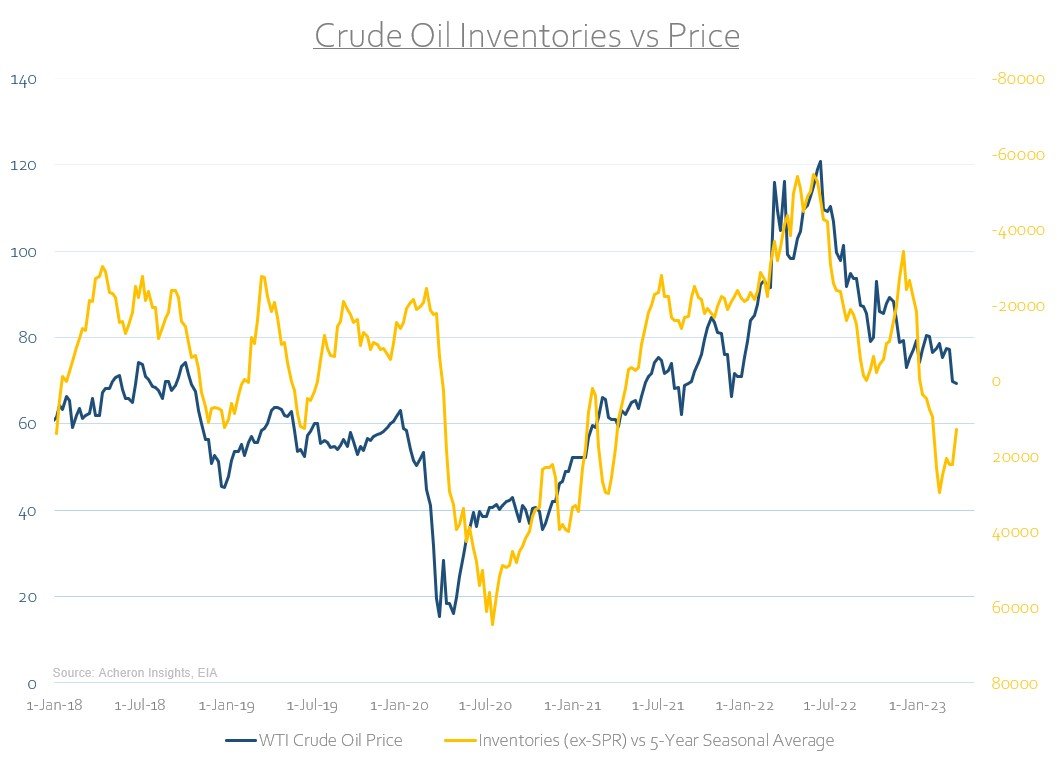

As I mentioned, the crude oil inventory dynamics have been significantly bearish in recent months. This may now be changing however. Indeed, the past couple of EIA inventory reports have seen material drawdowns. For bulls, this is good. As assessing the inventories changes and inventory levels provides a decent real time proxy for the supply and demand dynamics within the market, this shift from inventory builds and absolute inventory levels well above their historical averages to drawdowns is certainly a bullish development.

However, it is important to remember that a couple of weeks of positive data does not change the overall trend. Until we see inventory levels move below their seasonal averages, the supply and demand dynamics are probably bearish to neutral at best for now, but, positive signs are there.

Positioning

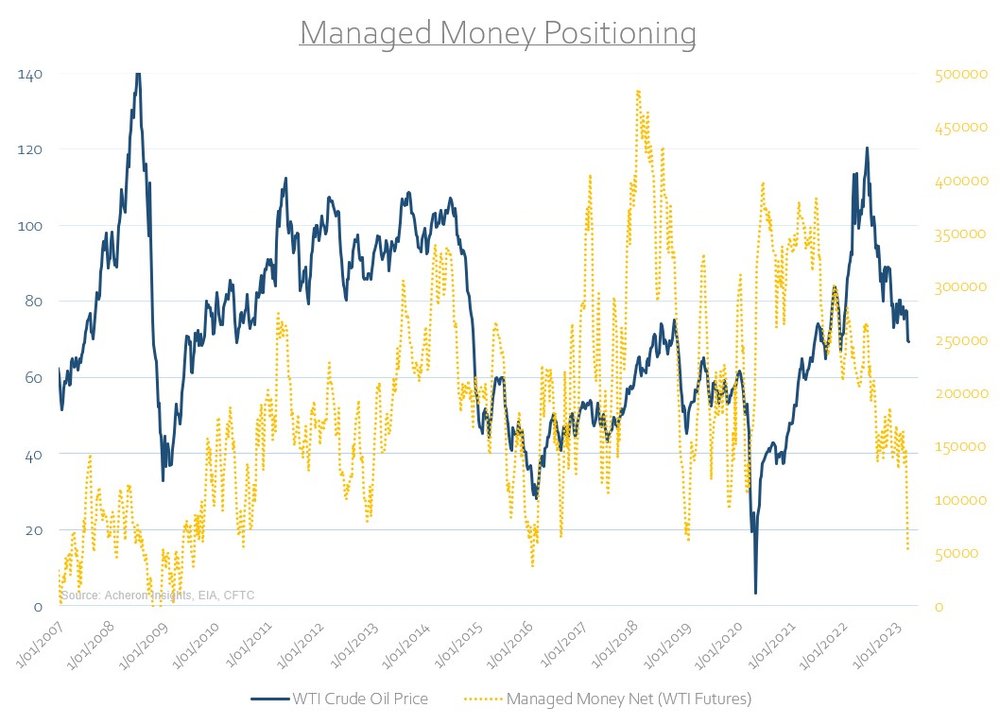

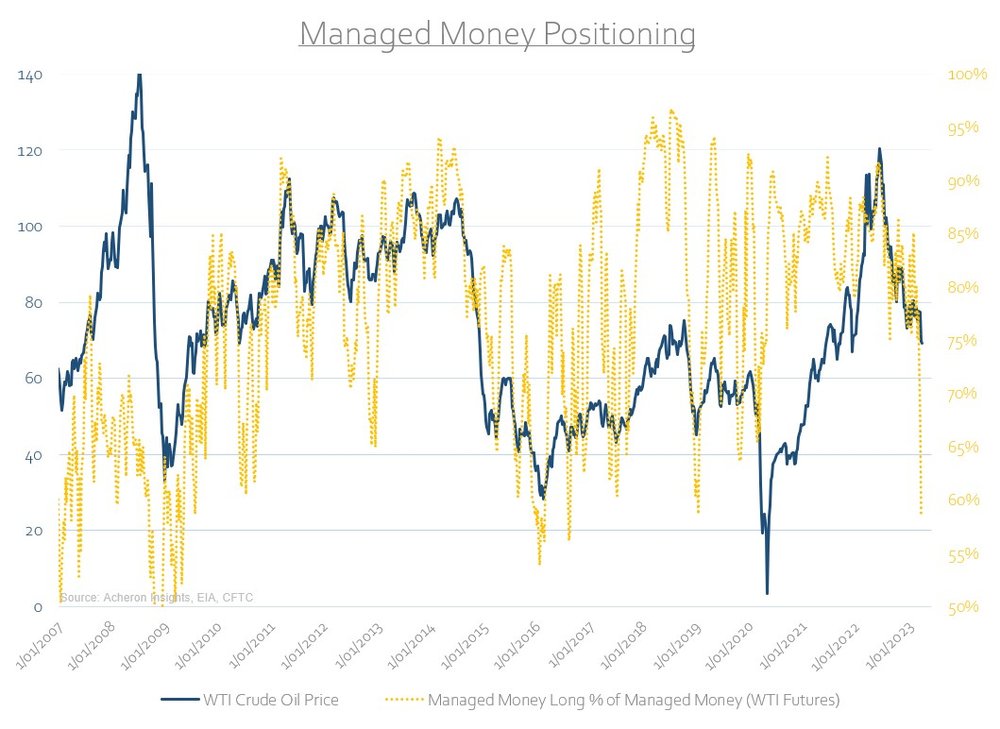

Where things are looking increasingly positive is within the spectrum of positioning. Everyone and their dog is currently bearish oil prices.

Nowhere is this more prevalent - and perhaps more important - than in the managed money category of futures market participants. Consisting of hedge funds and CTA’s, these market players are generally responsible for driving much of the trend in price, be it to the upside or downside. Hedge funds and CTA’s have de-risked their positions to a material degree in recent weeks (most likely to meet margin calls and the like), and as it stands, net positioning is as light as it has been in nearly a decade. As we can see below, such bearishness in recent times has tended to mark long-term buying opportunities for investors in energy markets.

Should we see continued drawdowns of inventories and tightening in the short-dated term structure, such positive fundamental developments could be the catalyst for the next leg higher, and if prices do appreciate, given the positioning dynamics of hedge funds, there is plenty of scope for them again re-enter the market and thus drive prices higher.

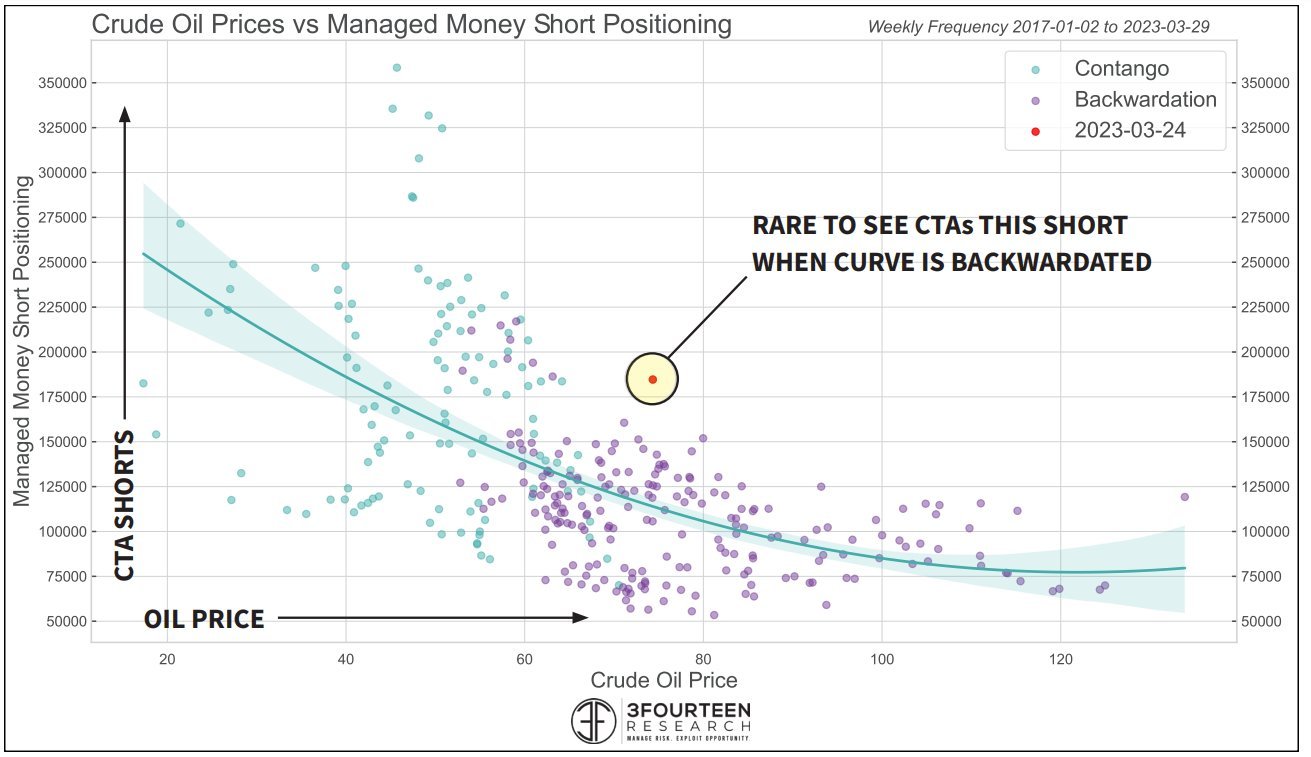

In fact, what could also exacerbate a potential short-squeeze is the fact that it is much more costly for hedge funds and the like to be short during periods of a backwardation. Why? because a downward sloping futures curve means you are paying a roll yield for the courtesy of being be short, effectively making it more costly to sell futures. Per the work of 3Fourteen Research below, we can see this combination of a backwardated term structure and level of short-positioning is rare. Given the negative roll yield associated with short futures positions at present, the incentive for those positioned as such to unwind the shorts and buy back their positions is greatly increased.

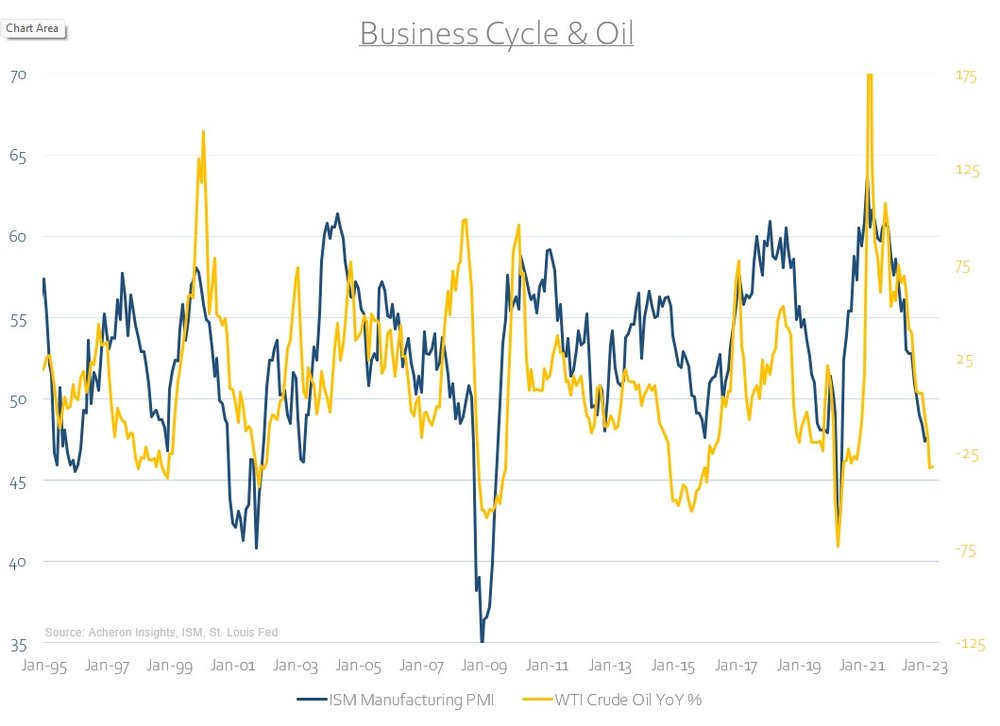

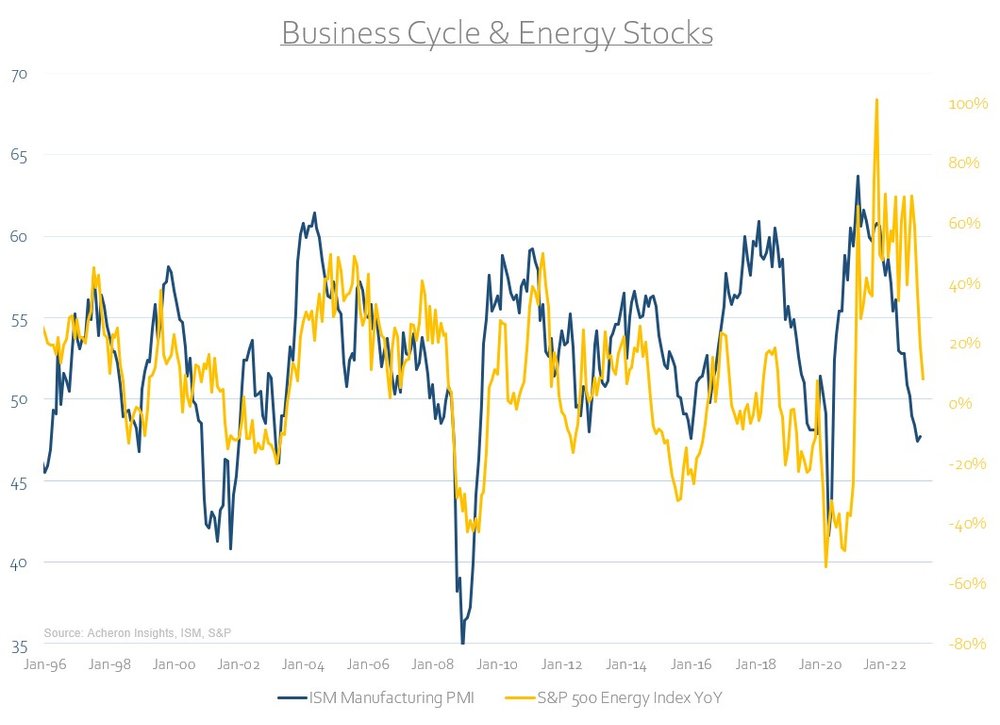

From a macro and economic growth perspective, not much has changed since my last deep-dive into the energy sector.

So far, energy markets have done a fairly solid job of pricing in the growth slowdown (which I believe continues to be bearish for the next quarter or two). Should we indeed experience a material slowdown in growth in the coming months, it remains to be seen how high a floor the structural supply constrains will provide for the oil price, meaning there is some potential further downside ahead for oil price and energy stocks via demand destruction that would likely result from a slowing business cycle. This dynamic certainly poses downside risk to the market.

Technicals

From a technical perspective, things are looking constructive. The long-term chart for crude oil recently flushed down to the $65 area to test an important support level which also coincides with the 200-week moving average. Again, whether this is the final flush-out required to form a sustainable bottom remains to be seen, but given how prices bounced so easily from this level, it does appear constructive from a long-term perspective.

Shorter-term, things are again a little less clear. The daily chart remains in a clear downtrend, but, the recent break-down below the $70 level was met with swift buying, suggesting a clear level of demand below these levels. For now however, we have just triggered a daily 9 DeMark sequential sell signal, and, with the 50-day moving average just above we may see one final move lower, or at the very least, a period of consolidation ahead in the short-term.

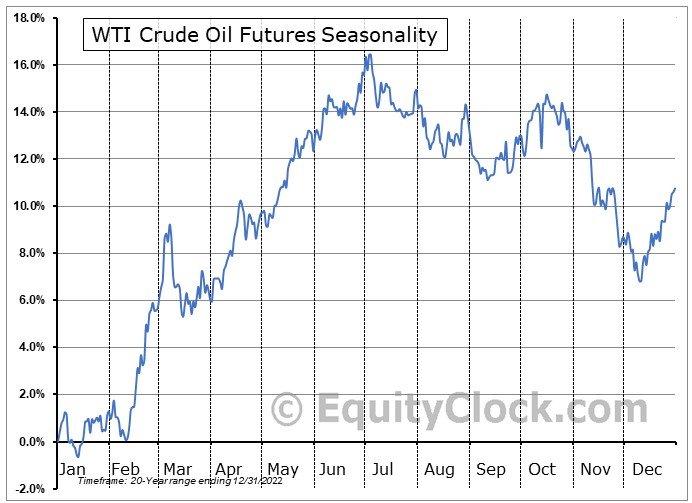

On a positive note, we are about to enter the most bullish time of year for oil prices from April through July as the northern hemisphere enters its spring and summer driving season. This dynamic could again alter the fundamentals in favour of the bulls, and is certainly an importantly consideration.

Conclusion and key takeaways

On the whole, while there are bearish dynamics still at play that ought to act as headwinds for higher oil prices and thus higher energy stocks, we are beginning to see signs of a shift toward a more bullish state within the oil and energy markets. Should inventories continue their trend of drawdowns and the short-term futures term structure revert to backwardation, we could very well be entering the next leg of the energy bull market. As such, it appears an opportune time for long-term bulls to consider adding exposure to the sector, whether this is via the oil price itself or the (still incredibly cheap) energy related equities.