We have, for some time, cautiously issued forecasts of slow and steady growth for the U.S. economy. Outlooks have come with one crucial caveat: they assume that nothing else goes wrong. Recent financial events have us questioning whether that condition has been breached. The failures of Silicon Valley Bank (SVB) and Signature Bank, and forced merger of Credit Suisse, have unnerved financial markets and increased recession risk.

The Federal Open Market Committee has a dual mandate of maximizing employment stabilizing prices. Those important policy goals assume the foundation of a stable financial system. While the battle against inflation is not over, the Fed must ensure it maintains the safety and soundness of—and ultimately, confidence in—the banking system. Ideally, this will be handled outside of the monetary policy process.

We expect recent banking troubles to curb credit extension, impairing growth. But the incremental deceleration will probably not be enough to place the Fed on hold. One more quarter-point hike is expected in May, followed by a long pause. Needless to say, projections are critically dependent on financial stability. Sustained activity can keep the economy out of recession, but we will closely track the accumulating risks to the outlook.

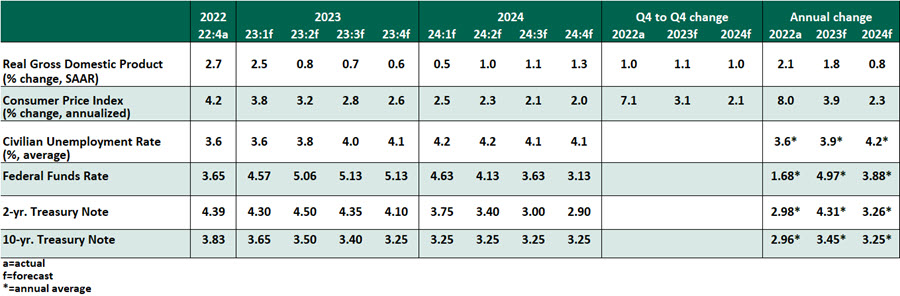

Key Economic Indicators

Influences on the Forecast

- Labor markets offered yet another pleasant surprise in February, with 311,000 jobs created. The unemployment rate rose by two-tenths to 3.6%, driven by encouraging growth in the labor force. Wages increased only 0.2% on the month, offering more hope that a wage-price spiral has been avoided. We continue to monitor weekly jobless claims, which are holding low despite reports of layoffs.

- Inflation is still not under control. The February consumer price index (CPI) weighed in at 6.0% year over year. Excluding food and energy, the CPI grew 5.5% over the same period, unchanged from the prior month. A slowdown in house prices has not yet prompted an easing of shelter cost escalation, but we still expect this to be a key element of reduced inflation over the remainder of the year. Prices are still rising briskly for core services (excluding energy and housing services).

- Retail sales cooled slightly in February, declining 0.4% from the month before after an outsized increase of 3.2% in January. Over the past year, nominal retail spending grew 6.8%, exceeding the rate of inflation and pushing up the estimate of overall growth for the first quarter. Consumers are not yet deterred.