In September 2021, Silvergate Bank, specializing in digital currency, was performing well. In fact, the bank reported record-breaking growth in deposits and loans in 2020, thanks in part to increased demand for its services from clients in the cryptocurrency industry.

On Wednesday, March 8, 2023, Silvergate Capital announced it ended operations and liquidated its Silvergate Bank.

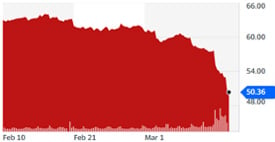

SPDR S&P

Regional Banking ETF (KRE)

This announcement sent its stock price plummeting, following a months-long downward spiral for Silvergate Bank, which was over-exposed to cryptocurrencies.

One day later, Silicon Valley Bank informed some clients that wire transfers could be delayed.

The bank's support phone lines became inaccessible.

In addition, numerous customers stated having difficulty logging in to the company's website to view their account information and make transfers.

Meanwhile, Silicon Valley Bank competitors like JPMorgan sought to convince some SVB customers to move their funds from SVB to JPMorgan.

This Friday morning, trading in Silicon Valley Bank stock has been halted as a classic run on the bank unfolds.

The entire bank stock index is down big as overnight deposits have been walking out the door... or rolling into higher rate options, squeezing bank profit margins.

One of the prevailing themes is that the Fed has been trapped via its mandate to fight inflation and maintain high employment.

Rate hikes had never accelerated so high in such a short duration. Critics of this monetary policy stated, "The Fed will keep hiking until they break something."

Things have been breaking in the past two days:

- First Republic Bank based in San Francisco, saw its shares plummet 16.5% Thursday and 15% Friday to $80 a share, a new 52-week low.

- Phoenix-based Western Alliance Bancorp stock lost nearly 35% and trades at $49 a share.

- New York-based Signature Bank stock fell more than 21% to $82, a 52-week low.

- Salt Lake City-based Zions Bancorp stock fell more than 13% to a 52-week low of $40 a share.

- Pasadena-based East West Bancorp shares were down more than 12% to $64 a share.

- Minneapolis-based U.S. Bancorp stock lost 7% to close at $42.30 a share.

Going back to basics is essential to understand the interplay between banking, gold and silver. Returning to fundamentals is a crucial refresher and could be critical in risk management.

From Investopedia, How Bank Deposits Work

The deposit itself is a liability owed by the bank to the depositor. Bank deposits refer to this liability rather than to the actual funds that have been deposited. For example, when someone opens a bank account and makes a cash deposit, he surrenders the legal title to the cash, and it becomes an asset of the bank. In turn, the account is a liability to the bank. By contrast, gold does not have these counterparty risk problems – and it’s a premier asset class worldwide.

Even last year, when gold stayed flat for the year, it outperformed Tesla by 73%, Facebook by 66%, Paypal by 65%, AMD by 58%, Nividia by 53%, Netflix by 52%, Amazon by 51%, Disney by 45%, Google by 40%, Microsoft by 29% and Apple by 29%.

Silver is not a primary monetary metal because it is also an industrial metal.

However, this is a double-edged sword; silver has been under-performing much like oil, in part because the market believes a recession will diminish demand for silver in consumer products.

This narrative is in question because the pivot to NetZero means an increased demand for renewables, including wind, solar, EVs, and batteries. Fortunately, all of these applications are all using a lot of silver.

Moreover, silver's cost of production puts a floor under its price. The spot price is extremely close to the production price, so silver seems to have limited downside.

Currently, there is an enormous chasm between the price of gold relative to the price of silver. Historically, silver makes significant leaps to close this gap whenever this has occurred.

However, it is essential to remember that silver is volatile. Thus, silver outperforms gold to the upside, just like it has underperformed recently to the downside.

In 2022, the US government spent $6.27 Trillion with total revenues of $4.9 Trillion. This represents a deficit of $1.38 Trillion that had to be borrowed into existence.

But this doesn't count the recently passed $1.7 Trillion dollar omnibus spending spree. This also doesn't count all the so-called emergency Ukraine "aid" spending which are now north of $140 Billion dollars.

Key Takeaways:

- Banks are coming under significant pressure.

- Congress and/or the Fed could be forced to step in, and you may hear these two words: bailouts.

- The Fed may be forced to rev up the money printers again (QE infinity)

- Then interest rates are likely to be reduced to stimulate the economy.

- Gold and silver will shine in this darkness.

© MonetaryMetals

Read more commentaries by MonetaryMetals