"How errors of human judgment can infect even the smartest people, thanks to overconfidence, lack of attention to details, and excessive trust in the judgments of others, stemming from a failure to understand that others are not making independent judgments but are themselves following still others – the blind leading the blind" -Robert J. Shiller

Foreword

I chose the topic for this month’s Absolute Return Letter during the Christmas break. I sat at home, looking at a pretty bleak world unfolding in front of my eyes and, consequently, asked myself the question – is this it? Has wealth-to-GDP finally begun to mean revert? Some of you will probably argue that wealth-to-GDP has mean reverted for about a year now (which is true), but things definitely took a turn for the worse towards the end of last year with inflation out of control in many countries. Suddenly, it wasn’t only equity markets that struggled. Property prices also started to decline, and property is the biggest driver of household wealth in most countries.

Anyway, to cut a long story short, the first few weeks of 2023 have defied all odds. Equity markets have performed very well, and one is therefore entitled to ask whether the dark thoughts that popped up in my head over Christmas can be justified. Was it all a storm in a teacup? In this month’s Absolute Return Letter, I will look at the arguments for and against.

The latest on wealth-to-GDP

As long-term readers of the Absolute Return Letter will be aware, I follow the ratio of wealth-to-GDP quite closely and have argued for years that (i) wealth cannot continue to grow faster than GDP, and (ii) the ratio must, sooner or later, revert to its long-term mean value. I have always focused on US wealth-to-GDP – not because the underlying theory doesn’t apply in the rest of the world, but because the ratio is more extreme in the US than it is elsewhere. Adding to that, the US has provided trustworthy wealth data since 1951. Other countries don’t even come close to that, meaning that establishing a long-term mean value is somewhat unreliable in many countries.

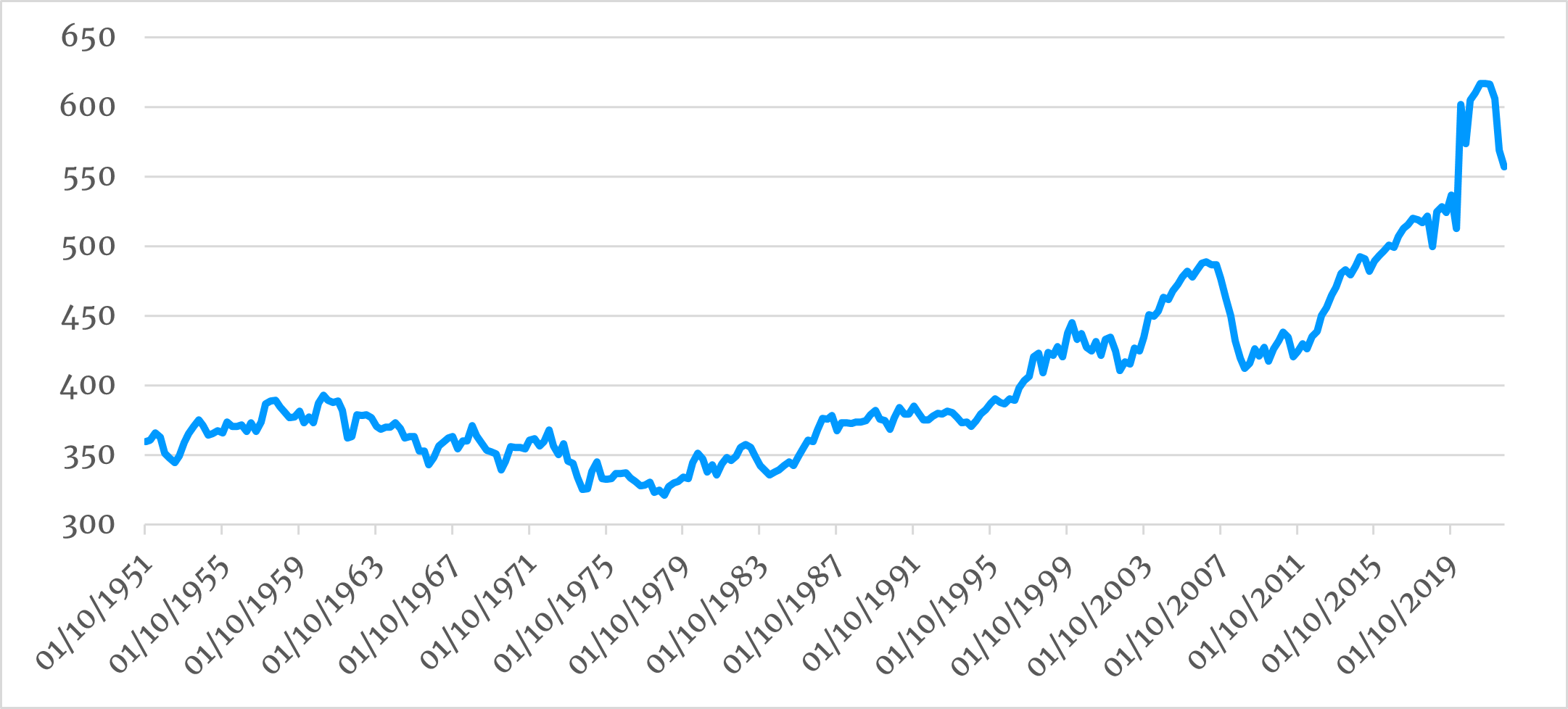

Now, look at Exhibit 1 below, which has been updated through September 2022 – the December wealth data will be published in March. As you can see, US wealth-to-GDP is off the levels reached in 2021. Since the third quarter of that year, when wealth-to-GDP peaked at 6.17 times, it has fallen quite sharply. As of the latest count (3Q22), the ratio now stands at 5.57 times, i.e. it has declined approx. 10%. However, as I have repeatedly pointed out, the long-term mean value stands at about 3.8 times, i.e. there is still plenty of downside – about 30% to be precise.

Exhibit 1: US wealth-to-GDP

Source: Absolute Return Partners

Going back to the opening question, it is virtually impossible to answer it with a reasonable degree of certainty. However, the early signs suggest that, despite the recent strength in global equity markets, the journey towards mean reversion of wealth-to-GDP has indeed begun. Before I go there, though, I need to make a point or two.

Wealth-to-GDP does not move in a straight line, just like asset prices never move in straight lines. If they did, life as an investor would be delightfully simple but, as you all know, it isn’t. January’s powerful equity rally should probably be seen in that light, although it could also be, as you will see later, the real thing. My money is on the former.

As I pointed out earlier, property is the biggest driver of household wealth in most countries, but it is far from the only one. Pension savings account for a large share of private wealth, and behind those savings one will find a broad mix of asset classes. Neither should one ignore the value of family-owned businesses. They are typically valued in line with public equities but with some delay. In other words, the big fall in public equity markets in 2022 is only now about to find its way into the valuation of private equity.

Last but not least, rising interest rates also affect wealth, both directly and indirectly. The direct impact is from the drop in bond values when yields rise. Direct bond ownership in the US is not meaningful, but it certainly is in Europe. Furthermore, all over the world, pension funds are significant holders of bonds, i.e. the recent rise in interest rates has had a rather dramatic impact on the value of many people’s retirement savings. The biggest indirect effect from rising interest rates is via the property market, where prices decline as mortgages become less affordable. That journey has only just commenced, i.e. we expect 2023 to be a tough year for property all over the world.

Why you need to take the recent equity rally with a pinch of salt

The performance of US equities will, to a large degree, dictate the performance of global equities in 2023, I believe. The UK is probably already in a recession, but that is more or less fully discounted already. Continental Europe is on the edge of one, although the very latest numbers coming out of the EU suggest that a recession there may just be avoided. Most investors have already discounted a recession, though, so EU equities could quite possibly perform better than many expect in 2023.

Going into 2023, the Far East – Japan in particular – looks the most robust region within the OECD from a GDP growth point-of-view, but one could argue that is already reflected in valuations out there.

The only remaining major market is the US market. A growing number of macroeconomic data points towards a US recession in the second half of 2023, but US earnings estimates do not yet reflect that; neither do US equity valuations. Most investors still take a rather sanguine view of the US economy and US equity markets in 2023, but the first clouds have started to appear.

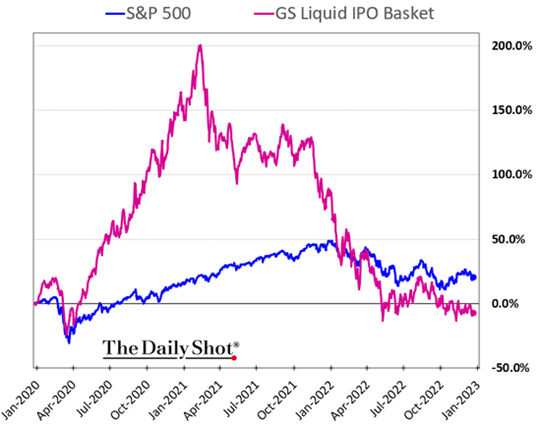

Let me give you one example. Over the years, I have learned that the performance of IPOs is a pretty good indicator of investor sentiment. When sentiment is upbeat, the IPO market often outperforms the broader market; when investors turn more pessimistic, IPOs begin to underperform. Now, look at Exhibit 2 below. As you can see, 2021 and 2022 have been two dreadful years for US IPOs, which tells me that investors are not as optimistic as the 2021 returns suggest.

Exhibit 2: Performance of US IPOs vs. S&P 500

Source: The Daily Shot

I am fully aware that the underperformance of US IPOs over the past couple of years has a lot to do with the changing appetite for technology but, even adjusted for that, Exhibit 2 tells me pessimism is building.

The counterargument

Now, let’s assume that the US economy escapes a recession in 2023, and that the corporate sector delivers earnings broadly in line with expectations. In that case, the January rally could be for real. This is not only wishful thinking on my behalf. As you can see below (Exhibit 3), the consensus forecast for US GDP growth this year is on the up again.

Exhibit 3: US 2023 GDP growth, consensus forecast

Sources: Bloomberg, The Daily Shot

There is a caveat, though, and that is inflation. Only if inflation continues to come down, will the Fed cool off, and that is a big ask for the US economy, where much of the inflation today is core inflation, unlike the EU, where much of the current inflation is non-core (i.e. mostly food and energy). In short, it makes a huge difference to central bankers, as to how much medicine needs to be applied, whether the inflation is core or noncore.

However, let’s assume the recent data is indicative of a more benign 2023, both growth-wise and inflation-wise. In that case, there could be plenty of upside in US equities this year, particularly in long-duration stocks, which had such a dreadful 2022.

Summing it all up

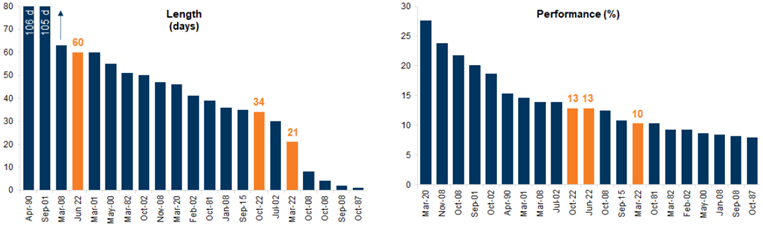

Although I won’t categorically state that the January rally is definitely ‘fake news’ (how would I know?), the odds are that it is just another bear market rally, adding to the growing list of bear market rallies we have enjoyed in recent years (Exhibit 4). As you can see, bear market rallies may last only a few days, but they can also last a few months. There is no set rule for the longevity of bear market rallies. You can only tell ex-post.

Exhibit 4: MSCI AC World equity index since 1981

Sources: Goldman Sachs Global Investment Research

That said, if things develop approximately as I think they will, we are not years away from the real thing. I see a year in front of me, where central bankers will struggle to push inflation much below 5%. This will most likely instigate another round of rate hikes, particularly in the US, and that will keep the bear market going for a while longer. Later this year, though, investors will begin to see through that and start to focus on the opportunity set on the other side. Last but not least, don’t forget that two consecutive years with negative returns in US equity markets almost never happen!