European policymakers face a dilemma: continue to hike interest rates to combat inflation or ease off to stimulate growth. Across Europe, headline inflation has started to fall while the growth outlook remains weak. That combination would typically limit the scope for future rate rises and favor increased exposure to interest-rate risk (duration). We believe investors should prepare to back the beneficiaries of lower euro rates—but hold off taking big interest-rate risk positions for now.

We expect rates to stabilize in the second half of this year and fall later in 2023 or early 2024. Bond market prices will likely anticipate the changes, rewarding investors who have positioned their portfolios appropriately. But in the short term, there are several factors that urge caution before taking aggressive rate positions.

ECB Remains Under Pressure to Stay Hawkish

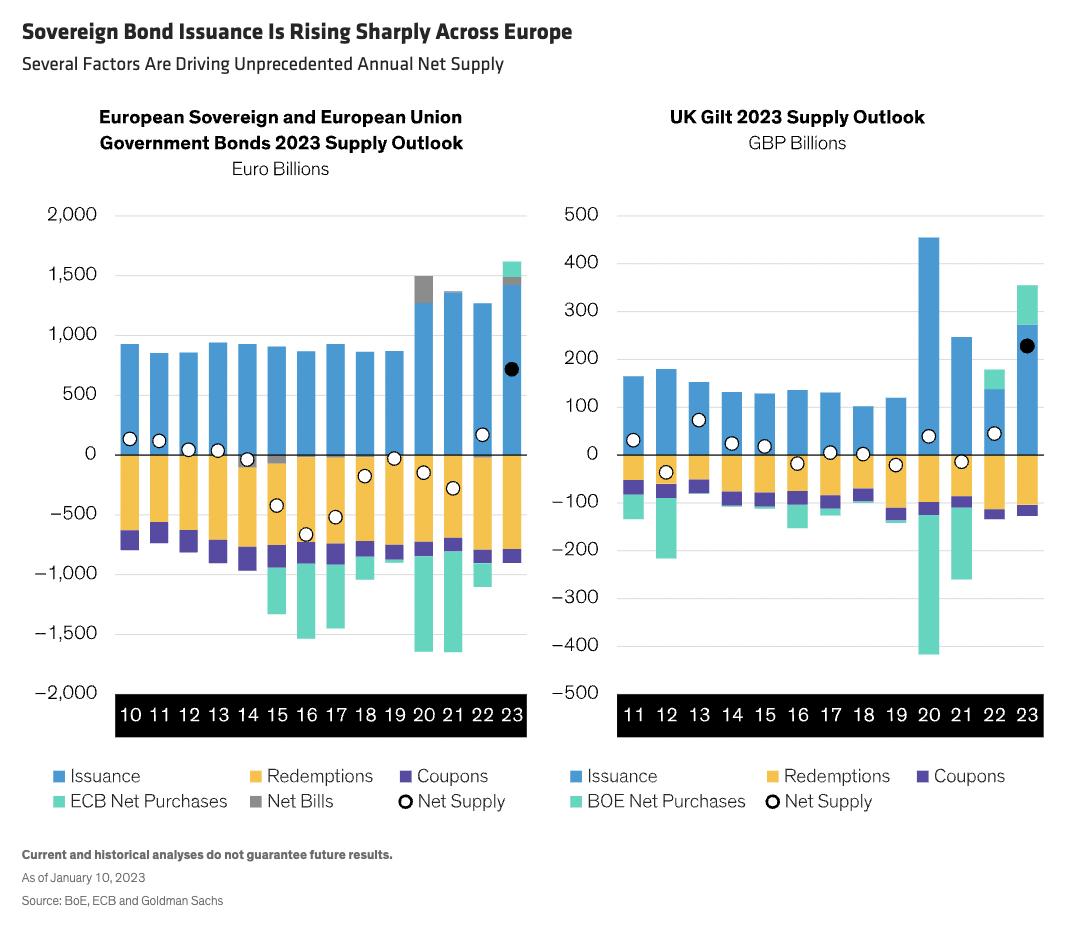

Despite falling headline numbers, core inflation in the euro area remains high, which will likely keep the European Central Bank (ECB) hawkish. And from a technical perspective, both UK and euro-area governments’ funding needs are rising, resulting in much higher sovereign-bond issuance (Display).

This coincides with the end of quantitative easing (QE) and the start of quantitative tightening (QT), increasing the publicly available supply of bonds to unprecedented levels and creating uncertainty about how markets will digest the elevated volume, particularly in the 20- to 30-year part of the curve.

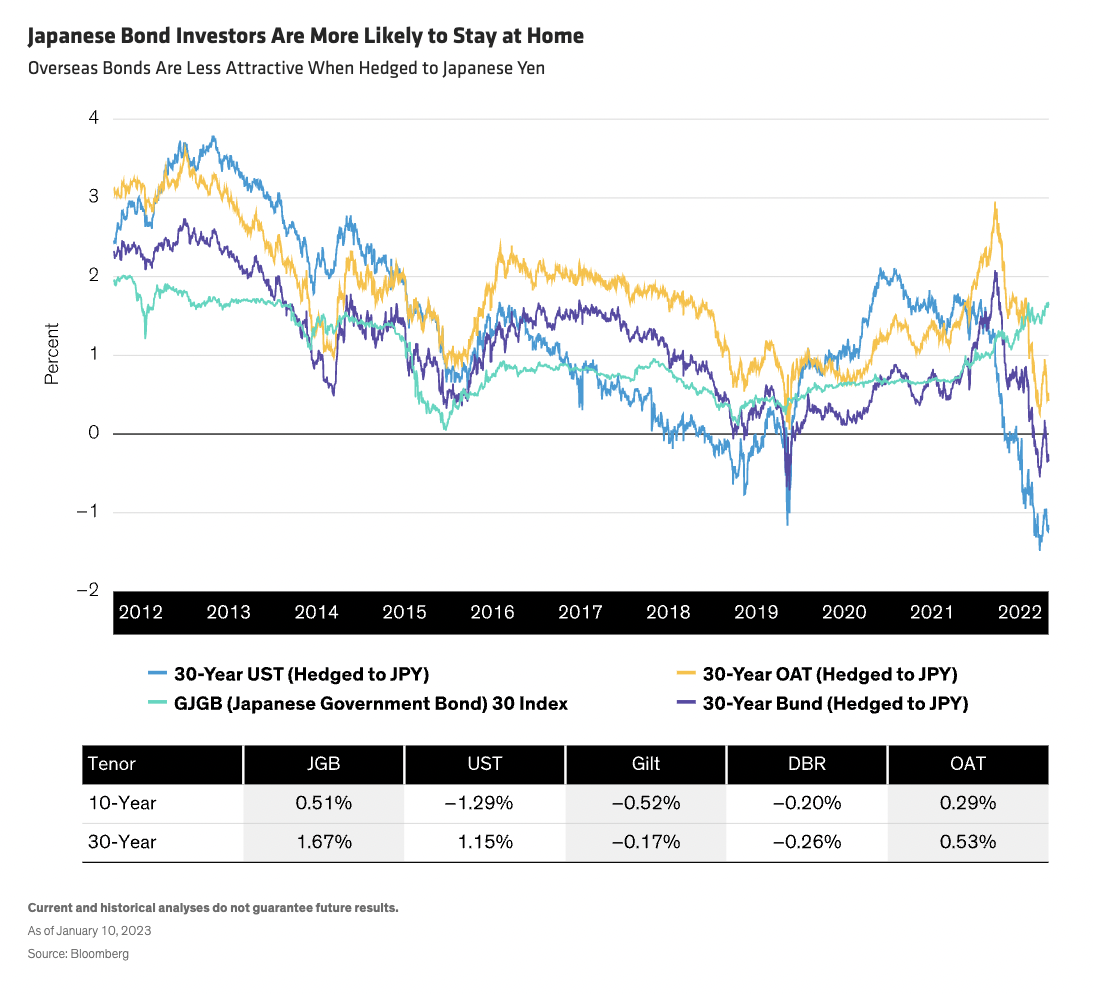

Overseas buyers’ reduced appetite for euro sovereign issues is a further potential concern. Notably, the Bank of Japan’s recent adjustment to their yield-curve control (YCC) policy has increased the yields of Japanese government bonds (JGBs) and reduced the attractiveness of overseas bond markets to Japanese investors—particularly on a currency-hedged basis (Display). It would take higher yields to make euro sovereign bonds attractive for Japanese investors. Thus, although European sovereign-bond yields have already risen meaningfully, we think there are still grounds for caution in the short term.

However, we do think that as the year progresses—and probably not too far into the year—it may be an attractive time to lengthen duration in Europe, as the battle between growth and inflation will likely tilt to make the growth slowdown the dominant factor.

Sovereign-Bond Sensitivity to Rate Hikes Varies

Sovereign-bond valuations across the European periphery have realigned, with several countries now perceived as stronger issuers than in recent years. Spain and Ireland’s status has improved, and their bonds are now trading more in line with French government bonds (OATS). Portugal is slightly more highly rated than Italy, while Greece, after demotion in 2010, is set to return to investment-grade status and is already trading at a lower yield level than Italy. That leaves Italian government bonds (BTPs) as the standout potential beneficiary from policy easing.

And while, in our analysis, BTPs have the most price upside potential, their potential downside has also been moderated by the ECB’s recently-introduced transmission protection instrument (TPI), a program that may help prevent peripheral countries’ spreads widening too far from German Bunds.

Recently, we have seen BTP spreads over Bunds ranging between 100 and 200 basis points, depending on the extent of TPI intervention. But our research suggests that BTP spreads may widen as Bund yields rise and narrow as Bund yields fall. This makes BTPs more sensitive to rate changes than their German counterparts, and so potentially attractive to shorter-term investors with a higher risk tolerance.

In the lower-risk part of the market, 10-year Bund yields rose to around 2.6% in October 2022 and then retraced to a little below 2.2% this year. We see a 2.5%–3% yield range as an attractive Bund level for longer-term lower-risk investors.

We think investors can consider a duration game-plan in terms of time frame: shorter term, be more cautious, but over the coming quarters, look to increase interest-rate risk. And be mindful of which sovereign bonds will be most sensitive to euro rate changes and most appropriate for their particular risk tolerance.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein