NewsLetter - December 2022

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDEAR READER:

SORRY, YOU’RE NOW POCKET CHANGE

Wells to Move Clients with Less than $5M Out of Private Bank: Reports

“Advisors have been given scripts to use when explaining the move to affected clients, who may incur greater fees, according to Business Insider…”

“Wells Fargo is trying to retain clients by having its financial advisors use a ‘carefully crafted script’ to explain the transition, in addition to promising to waive fees until the end of next year, according to the web publication”

"Periodically we review ... accounts to ensure they have the products and services that are appropriate for them," Wells told advisors to say when asked about the move, according to Insider. "In our recent review, we saw that there was another deposit account, mentioned in the letter, which was a better match with the financial activity that you are currently conducting with Wells Fargo."

Kind of reminds me of Newspeak in Orwell’s 1984.

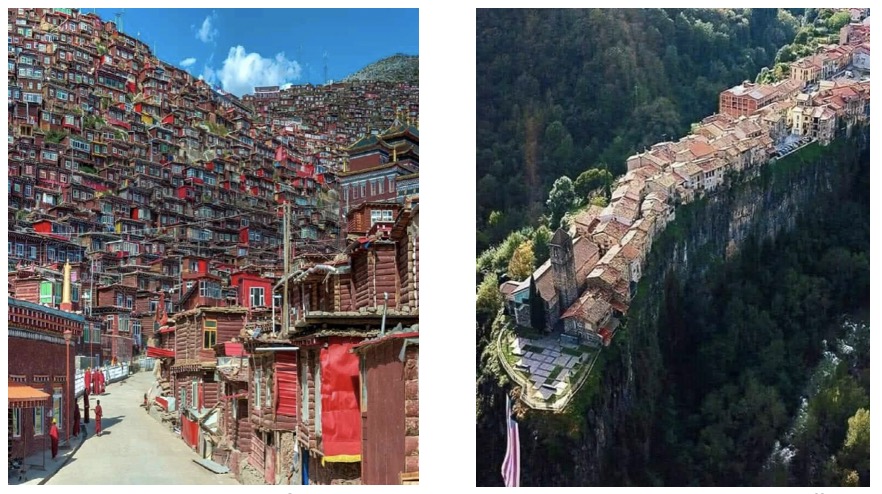

I WONDER WHAT THE RENT IS?

A mountain village in Tibet, China. And another village built off a basaltic cliff more than 50m high and covers an area of about 1 kilometre. (Castellfollit de La Roca, Spain)

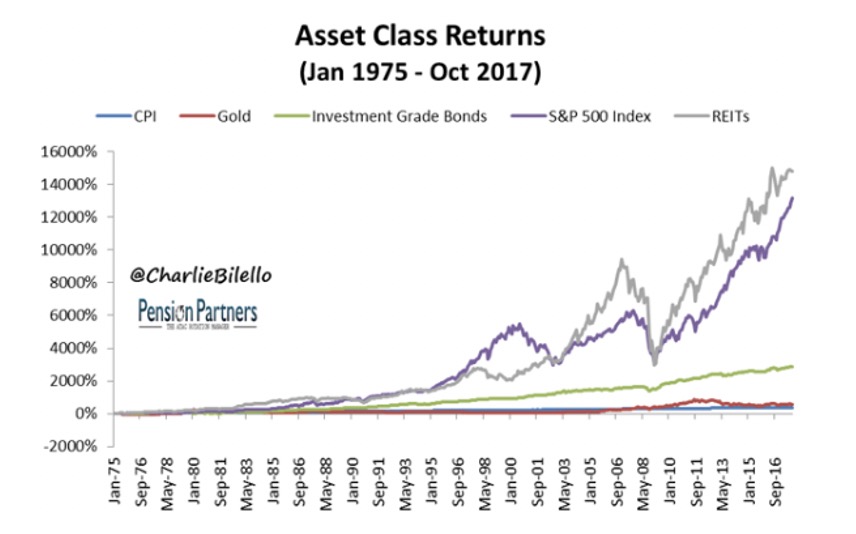

WHY YOU SHOULD INVEST IN GOLD NOW

Gold IRAs help you protect your financial assets with stability.

If you’re searching for a hedge against inflation, start buying gold coins, bars, and/or bullions.

This seems to be a recurring story flogged by firms looking to sell investments in gold. Don’t fall for it. The following chart is the most recent I can find, but I believe it clearly shows the fallacy. I guess no return is stable, but it’s not quite what an investor is looking for.

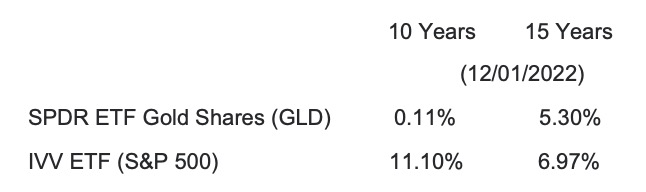

As for more recent annualized returns….

Why you should invest in gold now - CBS News

LOOKIN’ GOOD

Poor Michael labeled as the “guest” under the image. Michael is not only a partner at Evensky & Katz/ Foldes he’s also Chair Elect of the Coral Gables Community Foundation

IN THE LONG RUN WE’RE ALL DEAD

Catherine Woods and Jim Cramer’s investments may ultimately look good, but I wouldn’t bet on it.

For those who want to bet against them, Tuttle Capital Management has an exchange-traded fund (SARK) that bets against Cathie Wood’s stock picks (from inception in 11/30/2021 through to 11/28/2022, Wood’s ARKK is down 67% and SARK is up 79%), and they’re adding one that bets against Jim Cramer’s investment recommendations.

In case you don’t know, Cramer is the host of Mad Money and is known for his ardent (and noisy) endorsements of various stocks, with mixed results. In 2021, he praised Ark Investment Management’s Wood just before her flagship fund plummeted, and he also famously tweeted to buy AMC Entertainment Holdings Inc. just prior to a 30% plunge.

Least you’re in doubt about where I stand, although I’m not a fan of either Woods or Cramer, investing with them or against them is gambling. I just thought this was a great story.

WHO KNEW?

Ever wonder where some common sayings came from? From my friend Alex.

Close but No Cigar - During carnivals in the 1800s, cigars were rewarded as prizes for winning carnival games.

At the Drop of a Hat - Instead of a gunshot to indicate the race had started, in the 1800s it was customary to drop a hat to signal the start.

Best Foot Forward - When bowing to nobility, a gentleman would literally put his best foot forward, extending his best foot to take the bow.

In the Nick of Time - Through the 18th century, businessmen often kept track of debts owed by Carmen Nicks on a ‘tally stick’. When someone arrived to pay off their debt before the next was carved, they would save that day’s worth of interest – hence ‘nick of time’.

Jump on the Bandwagon – In the mid-1800s, circuses would parade around town for setting up. With bandwagons leading the parade, they drew large crowds, and politicians started renting space on the bandwagons to get facetime with an audience.

Get off Your High Horse - Before the advent of cars, owning a horse was a sign of prominence, since nobility and high-ranking military officials were primarily the ones who owned them. Getting off your horse meant to humble yourself.

Burning the Midnight Oil - In a time before electricity, candlelight or lamp oil was used for lighting. When you stayed up late to work, you literally burned the lamp oil at midnight.

Dressed to the Nines - Dressed to the nines meant that you were rich enough to literally purchase the entire 9 yards it took to create a tailor-made outfit (including a vast jacket, etc.).

HANG IN THERE

MORE HELPFUL SIGNS

YIKES!

“U.S. banks and financial institutions processed roughly $1.2 billion in likely ransomware payments in 2021, a new record and almost triple the amount of the previous year, according to a federal financial crimes watchdog.”

A WHOLE NEW MEANING TO FREE

Fidelity to Offer 'Free' Retail Crypto Trades but with 1% Fee ???

“Fidelity Investments is planning to soon offer retail investors commission-free trading in the cryptocurrencies Bitcoin and Ether, but it will still charge a substantial fee, according to news reports.”

The company’s website says that while the trades will carry no commissions, they will carry a 1% fee…”

Of course, that’s likely to be cheap compared to the “return” on the crypto investment.

I JUST LOVE HINDSIGHT

“All told, had you invested $10,000 in January and reinvested your money into the top stock currently in the S&P 500 each month this year, you'd have $190,479 now, says an Investor's Business Daily analysis of data from S&P Global Market Intelligence…”

TURNS OUT WE WERE PIONEERS

Hard to believe. The industry hit a milestone in September with more than 3,000 ETFs – a 30% increase since December 2020, according to Morningstar.

The first American ETF (S&P 500 SPDR) was in 1998. By 2002, there were 102 funds in the ETF market. That’s about the time we started using them.

EVER WONDER WHY THEY CALL THEM “LONGHORNS”?

“YESTERDAY’S GREATEST INVESTORS”

Speaking of hindsight …

In going through some old articles, I came across this story in an August 2011 Smart Money magazine (a Wall Street Journal publication). Probably should have been titled “Yesterday’s Greatest Investors”.

Below is a comparison of their performance compared to appropriate index investments from August 31, 2011 to November 29, 2022.

JUST ANOTHER REMINDER

Just another reminder how many firms represent they have "advisors" when in reality they're salespeople and there's no advising actually happening.

“CEG Worldwide & Spectrem Group research finds only 57% of clients with at least $1M in investable assets think they are getting investment management from their advisor and only 45% think they are getting financial planning.”

DON’T WORRY

A story in the Financial Times – a daily newspaper that focuses on business and economic current affairs. Based in London, England, the paper was founded in January 1888.

“One of the most persistent stories that money managers have whispered to themselves before going to bed every night over the past decade is that passive funds will definitely be found out in next big bear market. Sure, they murmured, their active funds were underperforming right now, but only because stupid central banks and their stupid ultra-easy monetary policy were “distorting” financial markets. And those evil passive funds were also distorting markets! After all, why else would record-smashing cash machine Apple and the rest of the quasi-oligopolistic technology industry dominate equity market returns over the past decade? Right? Surely — SURELY — when central banks finally wised up, markets would puke, investors would flee the siren-like allure of cheap beta and the value of active management would shine through once more? This narrative has periodically seduced financial journalists as well,. Lo and behold, the reality in 2022.”

“Morningstar’s latest Active Passive Barometer found that only 40 per cent of the almost 4,000 active funds it tracked survived and outperformed their passive peers in the 12 months through June. Only 29 per cent of active bond funds managed to do so. For what it’s worth, hedge funds aren’t doing much better, with the average fund down 6.66 per cent year to date, according to HFR (number of the beast!). In other words, the annus horribilis of 2022 is actually burnishing the case for passive investing rather than destroying it — and reinforcing the trend of the past five years.”

I think that the main reason is simply investor psychology: we don’t like to feel duped. If you tell someone that an S&P 500 index fund will be down 20% if the S&P 500 falls 20%, they’re not going to be happy when this comes to pass, but they can mostly accept it. But if you tell someone that you’re going to be nimble and protect them in a downturn, you’re going to have a difficult conversation if you suddenly find yourself down 30%.

SMILES FOR THE DAY

OPINION: RON BARON EXPLAINS HIS INVESTING PHILOSOPHY WITH GOAL OF DOUBLING HIS MONEY EVERY 5 TO 6 YEARS

Ron Baron is unquestionably one of the most respected money managers on Wall Street and the Op-ed on CNBC is a thoughtful discussion of the thought process behind active investing. Unfortunately, it may have been successful a decade or so ago, but not today. Here’s some data from Morningstar.

Op-ed: Investor Ron Baron on investing during periods of entropy (cnbc.com)

TIPS AND OBSERVATIONS

· Ring your own doorbell on your way to bed. This will clear the dogs off the bed.

· My brother went to an Alcoholics Anonymous Meeting. Anonymous my ass. He knew everyone there!!

· I just asked myself whether I’m crazy, and ‘We all said No’.

· Being a ‘little older’, I am very fortunate to have someone call and check on me every day. He is from India and he is very concerned about my car warranty and my home warranty as well as someone scamming me and hacking into my computer/banking details. He is always helpful and asks for my password to fix my problem and my bank account number to fix it too.

WANT TO FEEL OLD?

Mena points out it’s even worse than the list suggests as it is itself old. Elvis died in 1977 – 45 years ago – and Lennon in 1980 – 42 years ago.

HOT TODAY – TOMORROW?

Here Are the Few Stock-Fund Managers Who Managed to Post Gains over the Past Year

(12 months through September 2022)

From the Wall Street Journal – “Of those elite few funds that did post gains, several pursued niche strategies. The No. 1 fund, Kinetics Small Cap Opportunities Fund (KSCOX), which gained 17.8%”

Of course, it might be important to know that the fund accomplished this by maintaining huge positions in the same single stock: Texas Pacific Land Corp … a real-estate enterprise whose shares soared nearly 47% in the quarter. Some 57% of the Small Cap Opportunities portfolio was in Texas Pacific Land…

Can’t argue with success but might want to temper optimism with the risk involved in such a concentrated bet. While it may occasionally pay off, it doesn’t necessarily work in the long run. Remember, if you play black on the roulette wheel and it lands on black, your return is 100%, but if you keep playing, you’re guaranteed to lose.

From inception in July of 2001 until October 2019, the fund’s performance just about matched the iShares Russell Mid Cap Growth ETF (IWR). The big bet in late May of 2020 paid off with a 10-month return (3/19/2021) of almost 120% (i.e. all of the 2021 return came from the first few months). Subsequent to that, through September of 2022 the return has been flat.

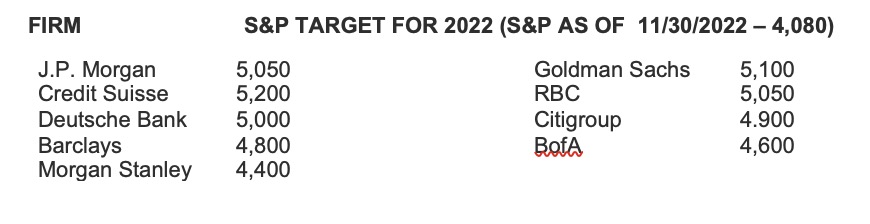

MAYBE A TAD OPTIMISTIC

“The U.S. stock market will probably deliver more modest gains ‘accompanied by higher volatility” next year’ – Jeffrey Kleintop, chief global investment strategist at Charles Schwab

“Meanwhile, JPMorgan analysts predicted in a research report at the end of November that the S&P 500 will rise next year to 5,050, partly on ‘robust earnings growth’ and easing supply chain woes. RBC Capital Markets has forecast the same price target as JPMorgan, while Deutsche Bank predicts the S&P 500 will end next year at 5,000, according to a slide presentation from its chief investment office.”

For those who projected at year end, they still have a month for the market to catch up with their projection. Fingers crossed but not holding my breath.

I HOPE THEIR LONG-TERM PROJECTION ARE MORE ON TARGET

My, what a difference a year makes. Although I’m sympathetic with the uncertainty of long-term projects, J.P. Morgan’s change from 2022 to 2023 seems just a tad bit extreme. Still, I’m rooting for them to be right. “Our forecast annual return for a USD 60/40 stock-bond portfolio over the next 10-15 years leaps from 4.30% last year to 7.20%.”

WE’VE COME A LONG WAY – BOTH TECHNOLOGY-WISE AND SOCIALLY

A photo of an engineer wiring an early IBM computer, 1958

As one of the commentators noted, they needed a woman as she read the directions….

MIGHTY PROUD

From Mark Trowbridge, President and CEO of the Coral Gables Chamber of Commerce:

“I also know that professional service firms of all types – CPAs, law firms and wealth managers – are the best of the best in our region and dot the business landscape of our city, having long added an incredible presence to our corporate community.

It is even more impressive when you think about a city of 50,000 residents that more than doubles its population Monday through Friday having a business profile such as ours, led by our banking, real estate and professional service businesses.

These entities are not only incredibly generous corporate citizens, they are also terrific role models for their fellow Gables-based companies when it comes to environment, social, and governance. This is most notably embraced by Evensky and Katz/Foldes Financial Wealth Management and how they support their individual managers and encourage them to sit on many of our city’s most prominent Board of Directors.”

THE BIG SECRET WALL STREET WILL NEVER TELL YOU ABOUT INVESTING

Gains are only part of the equation.

Risk management is essential.

Suitability is essential for investment planning.

Unfortunately, it’s true. Wall Street tends to avoid these issues. That’s where firms like ours come into play. We don’t keep secrets. In fact, those ‘secrets” are at the core of our investing philosophy and issues I’ve written books about and taught my students. As financial planners and fee-only advisors, our job is to help you invest for your future, not sell product.

If you’re interested in more ‘secrets’, check out my little book, Hello Harold – free electronically on Amazon – or send a note to Natalie Painter if you’d prefer a hard copy.

FOR NEXT HALLOWEEN

DIDN’T HELP

Making the Titanic's anchor chain at Hingley & Sons, c. 1909

REPRICED

While I generally agree with the sentiment, I loved the euphemism of “repriced”. Sure sounds better than “tanked”. Got to hand it to Wall Street for making lemons taste like lemonade.

“Pre-September, the 60/40 portfolio lost 20%, and the significance of this year is that both stocks and bonds are down. But that means both halves of the portfolio are less expensive,” he said. “This year we’ve repriced both assets to such a degree that the 60/40 mix is looking like its normal self. So if you’ve owned a 60/40 portfolio in the last year and it was doing poorly, don’t worry. It’s been repriced.”

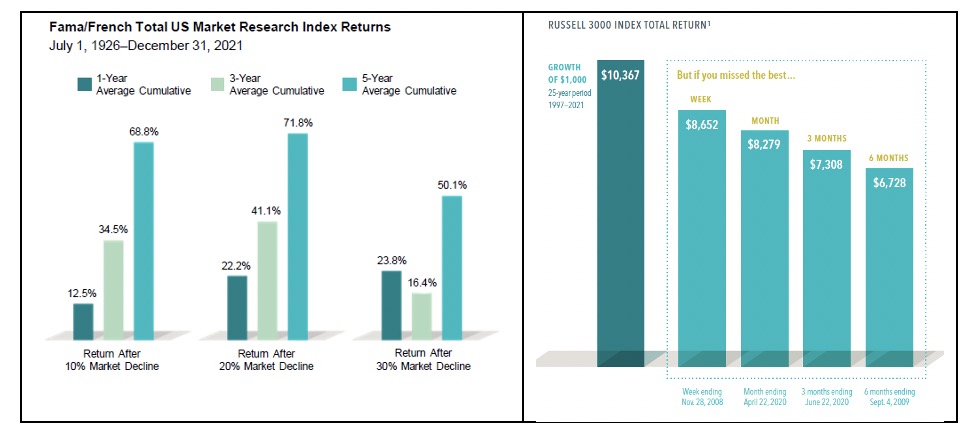

IGNORE THE NOISE

I know I often pick on the Motley Fool, but occasionally it really does provide good advice.

“Since 1950, there have been 39 separate instances when the 500 declined by a double-digit percentage, according to data from sell-side consultancy firm Yardeni Research. Excluding the current drawdown, every single double-digit decline was eventually fully recouped by a bull-market rally.

Furthermore, market analytics company Crestmont Research has demonstrated for years how powerful buy-and-hold investing can be. Crestmont published data earlier this year that examined the 20-year rolling total returns, including dividends paid, of the S&P 500 for the past 103 end years (1919-2021). In other words, it looked at how investors would have performed (including dividend payouts) if they'd purchased an S&P 500 tracking index at any point since 1900 and held for 20 years.

The results showed that investors would have generated a positive annual average total return over all 103 rolling 20-year periods. Only a handful of 20-year rolling periods yielded an average annual total return of 3% to 5%, while approximately 40% of all end years produced average annual total returns of 10.9% to 17.1%. Trusting great businesses – and indexes comprising high-quality companies – to grow over time has been a surefire strategy to build wealth.

Now is as good a time as any to put your money to work on Wall Street. Even if the stock market is weeks, months, or even over a year away from finding a bottom, history suggests that if you're a long-term-minded investor, you're wise to seek out bargains now.”

SAY IT ISN’T SO

Woman sues Kraft Heinz for $5M, says mac and cheese preparation isn’t as advertised

“A Florida woman is suing the Kraft Heinz Company for $5 million, claiming they misled the public about the time it takes to prepare its Velveeta microwavable mac and cheese cups.”

“Ready in 3½ minutes” is printed on the box, which is allegedly the amount of time the product takes to cook in a microwave. However, the suit says it takes more time to complete the other required steps.

- “First, consumers must ‘REMOVE lid and cheese sauce pouch.’

- Next, they must ‘ADD water to fill line in cup. STIR.’

- Third, ‘MICROWAVE, uncovered, on HIGH 3½ min. DO NOT DRAIN.’

- Finally, they should ‘STIR IN contents of cheese sauce pouch.’

- Defendant then notes that ‘CHEESE SAUCE WILL THICKEN UPON STANDING’.”

“Consumers seeing ‘ready in 3½ minutes’ will believe it represents the total amount of time it takes to prepare the Product,” the suit states. “Meaning from the moment it is unopened to the moment it is ready for consumption.”

BUYER BEWARE

Be Wary of ‘Fee-Based’ Vs. ‘Fee-Only’ Financial Planners

Certain financial advisors may not have your best interest at heart.

“First off, not every financial advisor can call themselves a Certified Financial Planner® (CFP). A qualified CFP is a professional who’s certified by the Certified Financial Planner Board of Standards, Inc. CFPs have a fiduciary duty, meaning they’re legally required to act in your best interest—and this is where the difference between “fee-only” and “fee-based” comes in.

What’s the difference between ‘fee-only’ and ‘fee-based’ advisors?

Fee-only planners act as a fiduciary and are compensated only by their client (you). They cannot accept third party commissions.

Fee-based advisors, however, are paid not only by you but via other sources, such as commissions from investment products. They’re incentivized by investments that pay them more, and therefore have conflicts of interest. If you see someone advertising their services as ‘fee-based,’ they’re hoping you confuse them with fee-only planners.”

Here’s a simple way to protect yourself. Ask your advisor to sign the Committee for the Fiduciary Standard Oath.

Be Wary of ‘Fee-Based’ Vs. ‘Fee-Only’ Financial Planners (lifehacker.com)

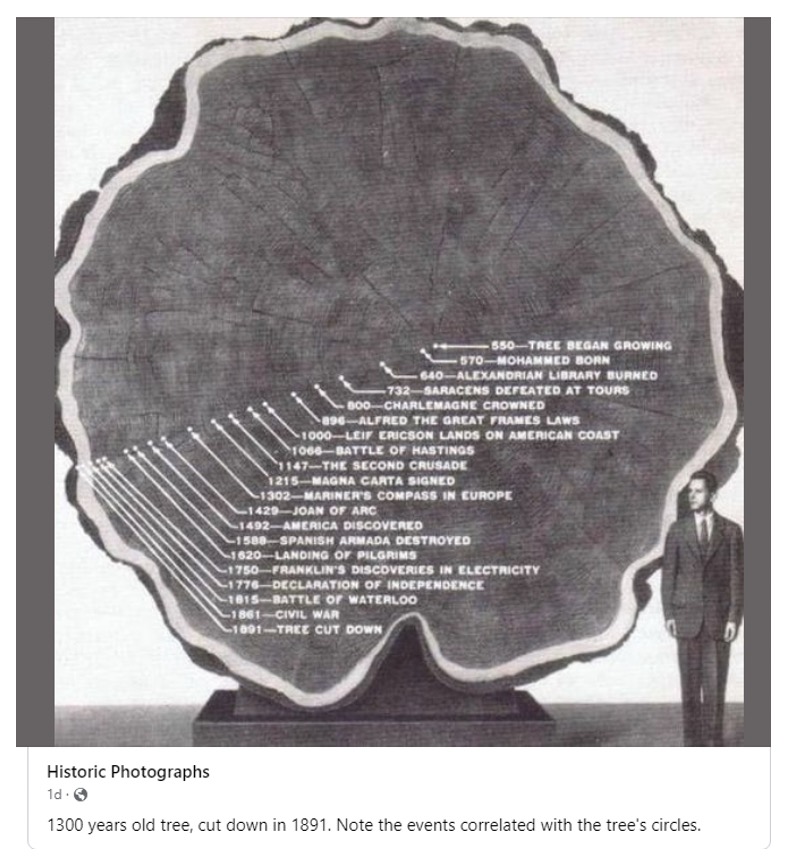

TIME FLIES

CRYPTO

BITCOIN AS OF 11/30/2022 IS TRADING AT 17,051

MORE WHOOPS

Or, a fool and their money is easily parted – especially if he follows the investment advice of an actor.

Remember that Crypto.com commercial titled “Fortune Favors The Brave”, which featured movie star Matt Damon?

In case you don’t, here’s a refresher. Damon did a now-infamous commercial for the cryptocurrency platform that got roasted on social media when it came out [I wonder why], and feelings towards it haven’t improved much in the year since the commercial originally debuted, on Oct. 28, 2021. At the time, the crypto good times were rolling. Closing price for bitcoin as of 10/28/2021 was $60,622.14

“And in these moments of truth, these men and women, these mere mortals — just like you and me — as they peer over the edge, they calm their minds and steel their nerves with four simple words that have been whispered by the intrepid since the time of the Romans: Fortune favors the brave,” Damon says in the ad.

Unfortunately, if you had followed Damon’s advice and purchased bitcoin when the commercial debuted, your crypto value would be $16,460 (11/28/2022), less than a third of what it was when you started.

LOOKS LIKE I HAVE COMPANY

Minneapolis Fed president Neel Kashkari continued his sharp criticism against cryptocurrencies.

“It’s kind of the wild wild West and chaos all rolled into one,” he said of the virtual asset during an event at South Dakota State University.

He added the ‘fatal flaw’ in the asset is that anyone can create those coins, making them ‘hard to distinguish’.

“It might be 99% noise, hype and confusion based on what’s going on right now.”

GLAD I’M NOT HOLDING MY BREATH

Bitcoin: The Next Bull Market Will Likely Start Soon (June 28, 2022)

- Bitcoin's decline has been epic, but the bear market is probably not over yet.

- Bitcoin doesn't need to produce anything. The digital asset is the closest thing to a global currency.

- The tightening monetary atmosphere creates a challenging environment for Bitcoin, however, as the Fed begins easing again Bitcoin should surge.

- Don't give up on Bitcoin. The next bull cycle should be massive, and Bitcoin will likely hit a new all-time high much higher than $70,000.

I don’t know when “soon” is but it’s obviously not now.

TO PARAPHRASE MARK TWAIN

The “recovery” of bitcoin has been significantly exaggerated.

6/15 Bitcoin eases from its 18-month low as the crypto market stabilizes. Bitcoin recovered on Wednesday [$22,573] after diving to an 18-month low [$22,207], buoyed by the U.S. Federal Reserve's tough stance on inflation….

FROM THE YAHOO CRYPTO CHAT SITE

8/11

24.6k is a new high since 14 of June ... in no time this thing will hit 30k

8/12

Next comes $26K resistance breakthrough, then rapidly to $30K plus

11/8

Can only scratch my head … [that would have been my response]

Have you heard about the ongoing trading platform which gives you access to monitor your trading account and recover your lost money if you have in any way traded with a wrong broker?

Okay, I will message her right away and I'm starting with $15,000... I can't wait to receive my gain like you all.

Hard to believe some of these entries

$30,000 BY THE END OF AUGUST

“After a difficult week for the cryptocurrency sector, during which Bitcoin (BTC) dropped below the $21,000 level due to fears of an impending interest-rate hike by the Federal Reserve, the flagship token is back above that mark, leading investors to wonder whether its price could reach the coveted $30,000 by the end of August.

As it happens, the community at CoinMarketCap has made predictions that the BTC token will not only reach the key psychological level but will actually trade at an average price of $32,493 by August 31, 2022 – using the ‘Price Estimate’ feature that allows users to speculate on the future pricing of cryptocurrencies.”

It closed out August at $20,050. Still might have been a good time to sell.

$30,000 BY SEPTEMBER

“Popular crypto trader and YouTuber CryptoYurii thinks the price behavior of Bitcoin might be a part of the Wyckoff setup, which could see BTC rising to $30,000 by September 2022. The setup is a technical indicator that alludes to the possibility of a bullish turnaround following significant downward movements.”

It closed out September at $19,432. Still a bunch better than today.

NOTHING LIKE SEEKING PROFESSIONAL ADVICE

Millennials are pouring cash into crypto – and making money [still looking for documentation of this statement, but so far, haven’t found it].

According to a study by Bank of America’s 2022 Private Bank Study of Wealthy Americans, wealthy millennials are pouring cash into crypto despite the price of crypto dropping 48% in the last six months. [I’m not sure the study quite says this. I believe it would be more accurate to say “they poured” [past tense]. The study was based on May/June data. In May, crypto was trading from $30 to $40 and in June from $20 to $30. Would be interesting to know what their average purchase price was.

Between May and June 2022, 75% of young people with a high net worth agreed that it’s no longer possible to achieve above-average returns in traditional investments like stocks and index funds [Ah! The pot of gold at the end of the rainbow].

And guess where they get their financial advice from? Social media!! The majority of the information comes from platforms like Instagram, TikTok, and Reddit.

AIN’T THAT A SHAME

FTX collapsed this week (11/7) after a three-day run on deposits sparked by the chief executive of its top rival, Binance, which posted tweets over the weekend questioning the stability of its business.

The announcement completed a stunning fall for Mr. Bankman-Fried. Just days ago, he was considered one of the wisest and most powerful figures in the crypto industry – an influential figure in Washington who was lobbying to shape crypto regulations. Now the company he founded is the target of investigations by the Securities and Exchange Commission and federal prosecutors in New York. His fortune – once estimated to be as large as $24 billion – has dwindled to less than a billion. Of course, a billion still goes a long way.

All my best,

Harold Evensky

Important Disclosure Information

Please remember that past performance is no guarantee of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Evensky & Katz/Foldes Wealth Management [“EKF]), or any non-investment related content, made reference to directly or indirectly in this commentary will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this commentary serves as the receipt of, or as a substitute for, personalized investment advice from EKF. EKF is neither a law firm, nor a certified public accounting firm, and no portion of the commentary content should be construed as legal or accounting advice. A copy of the EKF’s current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.evensky.com. Please Remember: If you are a EKF client, please contact EKF, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. Unless, and until, you notify us, in writing, to the contrary, we shall continue to provide services as we do currently. Please Also Remember to advise us if you have not been receiving account statements (at least quarterly) from the account custodian.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your EKF account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your EKF accounts; and, (3) a description of each comparative benchmark/index is available upon request.

Please Note: Limitations: Neither rankings and/or recognitions by unaffiliated rating services, publications, media, or other organizations, nor the achievement of any professional designation, certification, degree, or license, membership in any professional organization, or any amount of prior experience or success, should be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if EKF is engaged, or continues to be engaged, to provide investment advisory services. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers (see link as to participation criteria/methodology, to the extent applicable). Unless expressly indicated to the contrary, EKF did not pay a fee to be included on any such ranking. No ranking or recognition should be construed as a current or past endorsement of EKF by any of its clients. ANY QUESTIONS: EKF’s Chief Compliance Officer remains available to address any questions regarding rankings and/or recognitions, including the criteria used for any reflected ranking.

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits