India and Greater China: Exploring the Investment Opportunities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsIn emerging markets, we’re finding companies with particularly attractive valuations and enormous headroom for growth—which is a powerful combination. In this white paper, we focus on India and the Greater China region (China, Hong Kong and Taiwan)—which account for a large portion of our emerging-market investments at Wasatch.

Key Takeaways

- Over long periods of time, we believe there will be compelling opportunities to generate attractive returns in emerging markets—including India and the Greater China region (China, Hong Kong and Taiwan)—and in small-cap and mid-cap stocks.

- There’s enormous scope for India, Greater China and other emerging markets to increase their GDP per capita relative to the U.S. and relative to other developed nations.

- Because the opportunity set is so large and the headroom for growth is so enormous, we think Indian stocks—and small- and mid-caps in particular—could be treated as a separate asset class with a dedicated investment allocation.

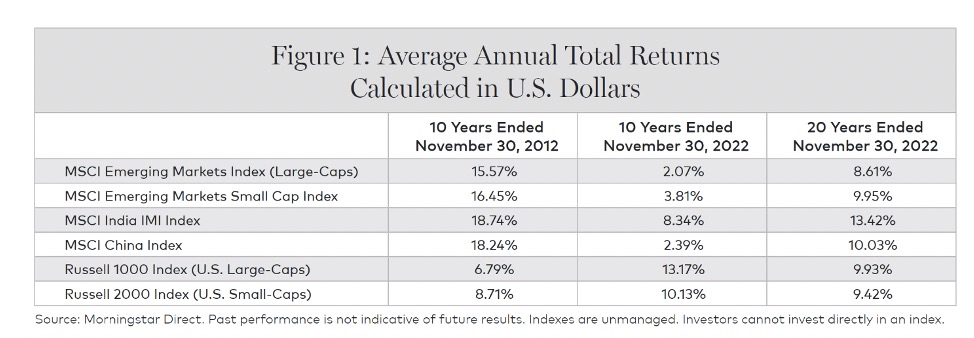

Because investing conditions can change dramatically, and stock prices can move in cycles, the recent past may not be a good roadmap for the future. Today, we believe this could be especially true among emerging markets. For a better understanding of how emerging-market conditions have changed over the past two decades, refer to Figure 1 below.

Figure 1

As you can see, the 10-year period ended November 30, 2012 was generally a strong decade for emerging markets—including large- and small-caps, and Indian and Chinese stocks. But, India notwithstanding, the 10-year period ended November 30, 2022 was mostly a lackluster decade for emerging markets. Nevertheless, the emerging-market universe produced significant returns for the full 20-year period ended November 30, 2022. U.S. stock performance, measured by the Russell 1000® Index of large-caps and the Russell 2000® Index of small-caps, is presented for comparison.

We think there were four main reasons for the generally lackluster emerging-market performance in the most recent decade ended November 30, 2022:

- There can be cyclicality in the performance of equities, and the previous decade ended November 30, 2012 was quite strong—particularly as emerging-market stocks bounced higher after the 2008–09 global financial crisis.

- In the most recent decade, developed countries including the U.S. looked more attractive due to compelling growth, government spending and monetary stimulus—and due to Covid-19 being especially tough on emerging markets. Moreover, emerging markets lurched from crisis to crisis—especially related to events in Greece, Venezuela, Brazil, Turkey, Argentina, China, Pakistan, Russia and Ukraine.

- Also during the most recent decade, the U.S. dollar was in a rising cycle—which hurt dollar-denominated investors in emerging markets.

- Late in the most recent decade, rising interest rates in developed countries created further obstacles for emerging markets.

LONG-TERM EXPECTATIONS AND CYCLICAL IMPROVEMENTS

Having described the broad performance of stocks over the past two decades, we have some thoughts about what may lie ahead. Over long periods of time, we believe there will be compelling opportunities to generate attractive returns in emerging-markets—including India and Greater China—and in small- and mid-caps.

Among emerging-market companies in general—and small- and mid-caps in particular—we believe investment success comes more from properly assessing business models, management teams and competitive landscapes than from simply buying their stocks at low prices. For our part, business models, management teams and competitive landscapes—among other fundamental factors—are where we concentrate the bulk of our research efforts.

Still, we understand that cyclical factors also impact market prices. For instance, the most recent decade has been out of sync with what we’d expect over the longer term. In other words, we believe emerging-market stocks will see cyclical improvements over the next decade. The reasons for such improvements include comparatively attractive prices, headroom for growth and technological advances that may transform the investment landscape.

GDP PER CAPITA: U.S. VERSUS INDIA AND CHINA

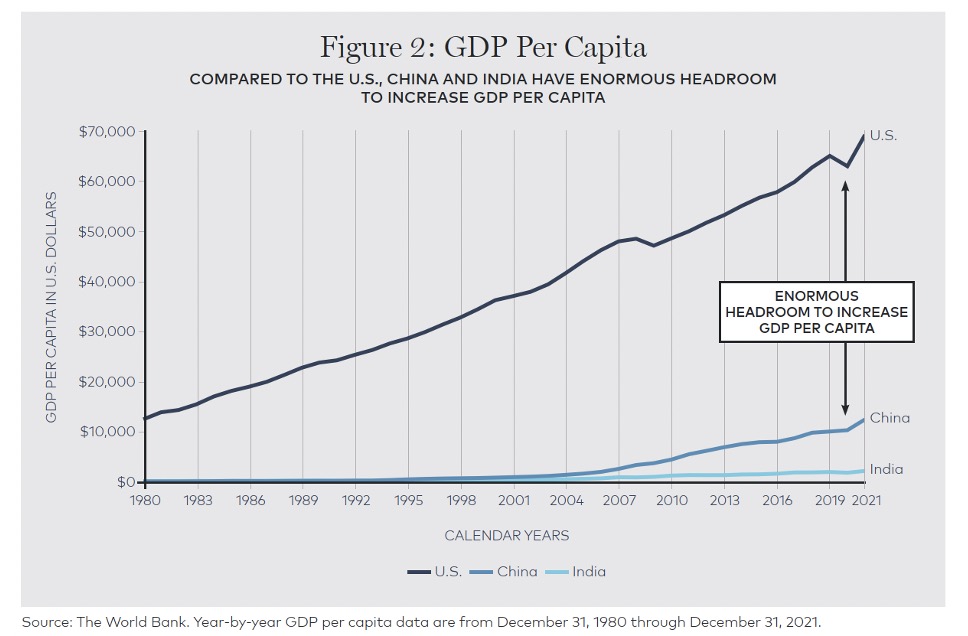

Another way to consider the investment opportunity set in emerging markets is to look at gross domestic product (GDP) per capita. For example, as you can see in Figure 2 below, GDP per capita is about US$69,300 in the United States, US$2,300 in India and US$12,600 in China.

Figure 2

Of course, there are large portions of the economy that GDP statistics don’t capture in India and China. But there’s still enormous scope for these countries and other emerging markets to increase their GDP per capita relative to the U.S. and relative to other developed nations. Moreover, this growth potential is even greater when population size is considered. India and China, for instance, each have over four times the population of the United States.

Key Takeaways—India

- In India, we believe the megatrends of digitalization, financialization, formalization and industrialization should be particularly beneficial for our holdings.

- India is home to almost 1.4 billion citizens—over a sixth of all the people world-wide—and is the fastest-growing major economy on the planet.

- India’s rapid advancement is based on a confluence of positive developments including public initiatives such as the massive Goods and Services Tax reform and private ventures such as Reliance Jio, which has created India’s low-cost, high-tech infrastructure for mobile phones.

- Like the U.S. in the 1980s, India is currently experiencing the long-term effects of changing government priorities—which have accelerated under Prime Minister Narendra Modi.

- Wasatch is among the relatively few U.S.-based advisors that run actively managed strategies exclusively invested in Indian stocks.

IN INDIA, WE THINK THE WIND IS AT OUR BACKS— AND THE COUNTRY COULD BE VIEWED AS A SEPARATE ASSET CLASS

At Wasatch, we scour the entire emerging-market universe. And we’re excited to invest in attractive, niche companies wherever we find them—even in countries with difficult macro conditions. Put another way, as emerging-market investors, we often make money in a country despite the country itself.

But what’s preferable, when possible, is to invest where the wind is at our backs. And more than in any other emerging market, we believe the wind is at our backs in India—especially among smaller companies.

Because the opportunity set is so large and the headroom for growth is so enormous, we think Indian stocks—and small- and mid-caps in particular—could be treated as a separate asset class with a dedicated investment allocation. Some might assert the same view about Chinese stocks, and we wouldn’t necessarily argue with such a position.

Having said that, China’s weighting in the MSCI Emerging Markets Index was approximately 30% as of November 30, 2022. And this weighting influences many emerging-market portfolio managers. As a result, their clients probably have sizable exposure to China already.

Not so for India. The weighting for Indian positions in the MSCI Emerging Markets Index was about 15% as of November 30, 2022. For our part, we believe it should be much higher.

DIGITALIZATION, FINANCIALIZATION, FORMALIZATION AND INDUSTRIALIZATION DRIVE INDIA’S VIRTUOUS CIRCLE OF PROGRESS

At Wasatch, we’ve traveled to India for about 20 years. And we meet on-site with as many as 100 Indian company management teams annually. Based on this bottom-up, on-the-ground research, our investment premise for the country as a whole centers largely on four megatrends: digitalization, financialization, formalization and industrialization.

For perspective, we note that extraordinary growth is what can totally transform an economy in relatively short order—whether during the Industrial Revolution that began in the late 1700s, the Computer Revolution that began in the 1950s or India’s four megatrends that we’re seeing today. Moreover, we believe digitalization, financialization, formalization and industrialization should benefit our Indian holdings in particular.

One reason for this is that we focus on high-quality small- and mid-caps. While extraordinary growth in segments of an economy can be a decent tailwind for large companies, it can be a gale of sustained advancement for small- and mid-caps that have even more scope for expansion.

Digitalization involves the electronic storage, retrieval and distribution of information—and the ability to communicate, collaborate and be productive with the help of electronic devices. Digitalization means that India is making great strides in the identification of its citizens (with data integrity and security) and in the expansion of the internet and mobile-phone services, often more progressively than developed-market counterparts.

Financialization entails the creation and distribution of banking, investment, credit, payment and insurance services. Financialization is at the foundation of any well-functioning modern economy. Additionally, digitalization is a critical element in India’s rapid financialization—and the interaction of the two is part of India’s virtuous circle.

Formalization refers to the greater transparency of economic activities and a better regulatory framework. One element of formalization is a simpler and fairer tax system that reduces layers of “petty corruption” and gets tax money to where it’s intended—to building infrastructure, for example. Another element of formalization is making personal and business transactions with electronic devices, rather than with tangible currency notes. This way, transactions are conducted more honestly and equitably—and with fewer inefficiencies that can clog economic systems.

Industrialization is driven mainly by manufacturing of goods for export. While India has a longstanding segment of highly trained workers, manufacturing provides jobs for the many lower-skilled workers who are less well-educated. Additionally, these jobs should enable the average Indian to afford some of the basic products and services that consumers in the West take for granted. What’s more, increased industrialization isn’t just a goal for the future. In fact, we’re seeing it take place on the ground today.

HOW INDIA COMPARES ON THE WORLD STAGE

As mentioned, there’s no doubt that China is a major economic force and is correspondingly well-represented in many emerging-market and global portfolios. India, by comparison, has a population of similar size, has even better investment prospects in our view and has less exposure to trade-war risks. But Indian equities are surprisingly underrepresented in many portfolios.

Consider that India is home to almost 1.4 billion citizens—over a sixth of all people world-wide—and is the fastest-growing major economy on the planet. India also benefits from a relatively young population’s willingness to embrace technology, transparency and the rule of law. Extremely rapid progress has ensued from there.

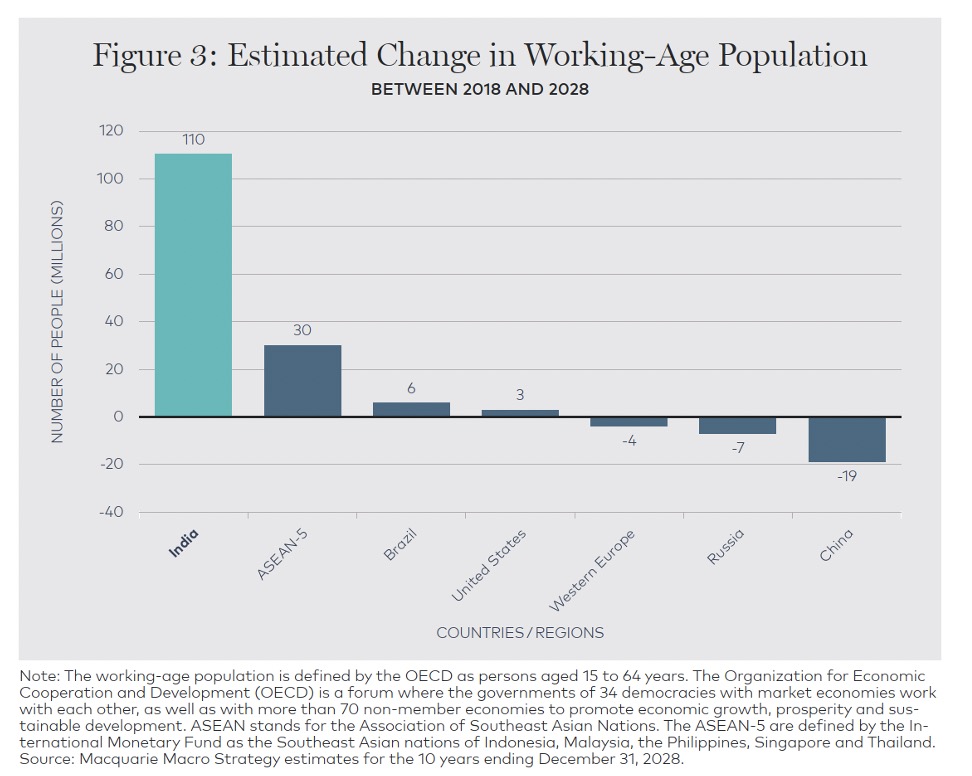

A young population is important because rapid change is more likely to be accepted by people who haven’t lived long lives controlled by an outmoded system. In fact, with over 65% of its total population under age 35, India has the largest group of young people on earth. In the next decade, as shown in Figure 3 below, the estimated change in India’s working-age population (ages 15 to 64) will be 110 million—making India’s workforce the world’s biggest at over one billion people, many of whom will be quite tech-savvy.

Figure 3

Additionally, among all countries, India has the most English speakers after the United States. This is important because English is frequently the language used for education, training and business interactions around the globe.

Technology has allowed India to leapfrog outmoded stages of development in the ways people communicate, the ways they live and the ways they work. Just imagine going from having no indoor plumbing or electricity to having a mobile phone and a bank account almost overnight.

Transparency—protected, of course, by world-class security—has allowed technology to function properly. Without transparency, technology would be limited in its ability to improve peoples’ lives. For instance, the Indian government wouldn’t be able to help the poor as effectively if people weren’t willing and able to disclose their identity, their circumstances and their needs.

Moreover, transparency is a vital aspect of the rule of law, which is a basic element of a thriving economy. People need to know that corruption will be exposed and that what they earn and save won’t be stolen through malicious schemes. The rule of law also encourages people to engage in productive work and pay their taxes.

WHAT MAKES INDIA SO COMPELLING NOW?

In India, the Hindi term “jugaad” is used to describe an improvised fix, or a clever solution born of adversity. In other words, jugaad characterizes a way of life—an attitude of doing more with less. In the past, jugaad had meant that India always found a way to move ahead incrementally and to make do.

But what’s happening in India today is much more than simply making do. Preparation has met opportunity, and India is currently taking a giant leap forward. This rapid advancement is happening now because there’s been a confluence of positive developments.

These developments include public initiatives such as the massive Goods and Services Tax (GST) reform and Aadhaar, which uses biometric data to electronically identify almost all of India’s adult population—and private ventures such as Reliance Jio, which has created India’s low-cost, high-tech infrastructure for mobile phones.

From a political standpoint, Prime Minister Narendra Modi has less than two years remaining in his second five-year term—and he will likely run again in 2024. Modi’s popularity should enhance the prospects for continued government reforms, economic-growth initiatives, and corporate competitiveness as India strives to lure manufacturers looking for relief from tariffs and other disruptions tied to the trade dispute between the U.S. and China.

In this regard, the Make in India initiative is intended to improve infrastructure, develop skills, foster innovation and secure intellectual property rights. Under the initiative, government incentives spur companies to develop, manufacture and assemble products in India.

TODAY’S INDIA IS SIMILAR TO THE U.S. IN THE EARLY 1980s

Later in this white paper, we describe how Chinese capitalism differs from Western capitalism. By contrast, Indian capitalism resembles what’s practiced in the West. In fact, even though India is located in the East, the country’s economic development and customs have much in common with those of the United States. But India has significantly larger headroom for business expansion.

When we consider why the United States has had better economic growth than most other developed countries in recent decades, we believe the reasons include U.S. deregulation and other free-market reforms that began in the early 1980s under President Ronald Reagan. Like the U.S. back then, India is currently experiencing the long-term effects of changing government priorities—which have accelerated under Prime Minister Modi. India’s forward-thinking measures have helped make the country the fastest-growing major economy in the world and one of the most fertile emerging markets for finding attractive investments.

Even India’s do-it-yourself investor culture and the proliferation of self-funded retirement plans are similar to those of the United States. In the U.S., there are individual retirement accounts (IRAs), 401(k) plans and other savings vehicles. In India, there are systematic investment plans (SIPs). The goal in each country is the same: getting people who are still relatively young to take charge of financial and retirement planning—and benefit from the powerful force of long-term compounding. At the same time, investing by Indians themselves should improve market efficiency, provide funding to companies at a reasonable cost of capital, enhance economic development and lessen the country’s dependence on foreign investors.

WASATCH GLOBAL INVESTORS: EXTENSIVE EXPERIENCE IN INDIA, ESPECIALLY RESEARCHING SMALLER COMPANIES

As mentioned, we’ve researched companies in India for about 20 years. And our firm is among the relatively few U.S.-based advisors that run actively managed strategies exclusively invested in Indian stocks. Additionally, compared to their benchmarks, many of our international, global and emerging markets strategies are overweighted in India.

With our India-only strategy—the Wasatch Emerging India strategy—we typically hold 20 to 60 positions. Although we can invest in companies of any size, we focus on small- and mid-caps that tend to have especially significant scope for growth. We think our deep, fundamental research of smaller companies is very different from many emerging-market managers and indexes that generally concentrate on bigger names.

Key Takeaways—China

- China has a rapidly growing economy that’s less dependent on exports than many casual observers assume.

- Outside of semiconductor production, which is still in a nascent stage, China already has a large and deep range of investable companies across market capitalizations.

- Investors must recognize that Chinese capitalism isn’t the same as the capitalism practiced in the West.

- In evaluating a Chinese company for purchase, the impacts of the firm’s products and services on the broader social good must be carefully considered.

- To the extent that recent events in China foreshadow a more activist role for the government in determining how businesses are run, returns on capital—compared to those in India, for example—may remain compressed.

MAINLAND CHINA: ECONOMIC DEVELOPMENT SHOWS SIMILARITIES TO THE U.S. IN THE 1960s

Turning back to China, we think the mainland’s state of development today is analogous to where the U.S. was in the 1960s. After World War II, the U.S. was one of relatively few nations that were in a strong economic position. In the late 1940s and throughout the 1950s, the U.S. was a major exporter of high-quality manufactured goods to foreign countries.

As the 1960s progressed, however, the U.S. was primarily interested in serving the domestic needs of a rising middle class. For example, the Big Three automobile companies—General Motors, Ford and Chrysler—were predominantly focused during that period on selling cars to American consumers. This is the type of transition we see mainland China making today.

For decades, mainland China has been an exporting powerhouse as it has ramped up its economy by improving its industrial and technological capabilities. Now, with over 1.4 billion people, mainland China is becoming increasingly focused on its own needs for modern living standards.

This means existing Chinese companies and startups should have enormous opportunities for growth just within the country’s own borders. To put these opportunities in context, we note again that the mainland Chinese population is more than four times the size of the U.S. population.

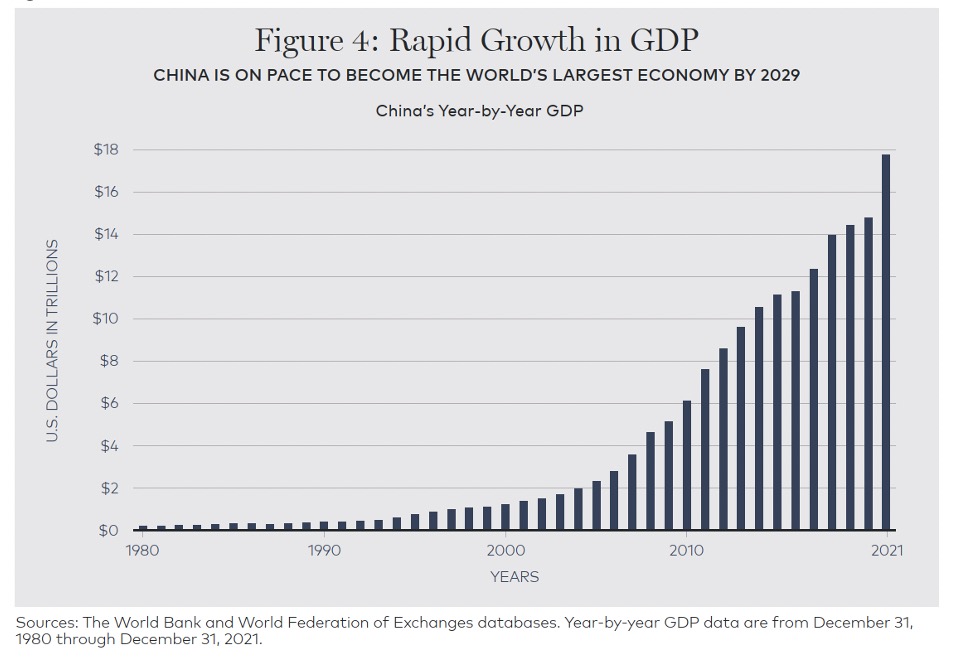

As shown in Figure 4 below, China has a rapidly growing economy with annual GDP in 2021 of nearly US$18 trillion—which already dwarfs the country’s exports at approximately US$3.4 trillion. So it’s clear that even now, China is less dependent on exports than many casual observers assume. Moreover, regardless of politics and trade issues, we think China is mostly a well-run economy and is too important to ignore from an investment standpoint.

Figure 4

INVESTMENT OPPORTUNITIES IN CHINA, TAIWAN AND THE SEMICONDUCTOR INDUSTRY

As we describe in other communications, we think mainland China may start making major strides to decouple its semiconductor industry from that of the rest of the world. To better understand this issue, we also need to evaluate what’s going on in Taiwan, which we consider to be part of the Greater China region. According to a recent report from Taiwan’s statistics bureau, exports have driven much of the island’s economic growth. A substantial share has come from Taiwan Semiconductor Manufacturing Co., the country’s largest firm.

While China bristles at Taiwan’s affinity with the West, there’s some optimism that U.S.-China relations are in a holding pattern. The thinking seems to be that even if relations don’t improve under the Biden administration, they’re unlikely to deteriorate much further. This thesis is reasonable in our view.

Considering Taiwan’s strong business ties with the U.S. and Europe, we believe China’s long-term strategy is to invest heavily in building a Chinese-centric infrastructure for semiconductor design and fabrication. However, start-to-finish semiconductor production is a complex process that requires considerable time and effort to develop the necessary expertise. Meanwhile, countries such as Taiwan may find themselves caught in the middle between China’s hunger to expand its global economic influence and the desire of the U.S. to contain Chinese expansion.

Having said that, trade tensions and other forms of geopolitics have always been inherent risks in emerging markets. And despite these risks, we think there may be good investment opportunities if China develops a semiconductor infrastructure to serve its own needs. These opportunities could go beyond design and fabrication—as semiconductor production also requires many different types of machines, tools and other supplies.

Outside of semiconductor production, which is still in a nascent stage, China already has a large and deep range of investable companies across market capitalizations. Moreover, many of these companies cater to domestic Chinese demand—which is an economic segment we find particularly attractive.

As for our investments in Taiwan, we hold some semiconductor-related companies. But unlike most of our Chinese companies, which tend to serve domestic Chinese needs, our Taiwanese companies tend to have global customers.

CHINESE CAPITALISM VERSUS WESTERN CAPITALISM

Clampdowns by Chinese regulators in areas such as technology and private education have caused some investors to rethink their China allocations. These government actions came in the wake of a broader push aimed at curbing monopolistic behavior in the so-called platform economy.

Investors began to ponder the implications in November 2020 when Chinese regulators suspended the initial public offering (IPO) of Ant Group, a financial-technology firm whose chairman and majority shareholder is renowned tech titan Jack Ma. Thereafter, a flurry of additional restrictions rattled financial markets. Pundits in the press and elsewhere have even begun to question the Chinese government’s commitment to capitalism.

In assessing these concerns, it must first be recognized that Chinese capitalism isn’t the same as the capitalism practiced in the West. Western capitalism in its modern form rests largely on the free-market principles laid out by eighteenth-century philosopher and economist Adam Smith.

In The Theory of Moral Sentiments, Smith introduced the concept of the “Invisible Hand” to describe the unintended social good brought about by individuals acting in their own self-interest. With an almost religious zeal, Smith viewed the workings of the free market as manifestations of something akin to divine providence.

The Chinese reject Smith’s formulation. They believe capital allocation driven by self-interest and greed inevitably leads to inequality, exploitation and the dangerous accumulation of power by large corporations.

Because all of these things undermine the Chinese Communist Party’s (CCP’s) objectives of common prosperity, capitalism in the Chinese model must be kept on a tight leash. In what might be characterized as “guided capitalism” or “directed capitalism,” Adam Smith’s Invisible Hand is replaced by the not-so-invisible and sometimes-heavy hand of the Chinese government.

THE NEED FOR A COMMON-SENSE APPROACH TO INVESTING IN CHINA

Because social cohesion is especially important in China, we think the government’s willingness to use strict regulations in pursuit of policy goals makes it more important than ever to take a pragmatic approach when investing there. In evaluating a Chinese company for purchase, the impacts of the firm’s products and services on the broader social good must be carefully considered.

Certain consumer-facing businesses may be especially at risk of finding themselves at odds with the government. Among these are companies such as payment and social-media platforms that collect large amounts of proprietary data on Chinese citizens and companies that may be perceived as failing to promote socially responsible behavior. Also at risk are firms that the government deems important to the country’s competitiveness and may therefore be less able to operate freely.

Because China’s economy has matured to the point of becoming self-sustaining, exports and capital from overseas are no longer as vital to its survival. As a result, companies are encouraged to emulate the CCP’s vision of what their business models should look like.

The government, in turn, now has additional scope to regulate industries without having to fear the consequences of alienating international investors. China’s nascent semiconductor industry is a notable exception—and for that reason has become the subject of intense government efforts to promote its development.

Despite challenges, including the onerous zero-Covid policy that’s still snarling production and supply chains, we think China’s self-sustaining economy and relatively stable currency provide advantages found in few other emerging markets. For example, the rate of capital formation measured by the number of IPOs in the Greater China region—China, Hong Kong and Taiwan—is the highest in the world.

Regarding the recently well-publicized tensions between China and Taiwan, we don’t expect an escalation. China depends on the smooth operation of Taiwan’s businesses, notably Taiwan Semiconductor, in order to ensure the progression of Chinese artificial intelligence and high-tech manufacturing. Additionally, while Taiwan is an island geographically, it isn’t an island unto itself in terms of semiconductor manufacturing. Taiwan relies on equipment and supplies from many other countries. If China were to escalate tensions with Taiwan, the equipment and supplies would likely be cut off—slowing the pace of Chinese economic growth. And we don’t think China is willing to make such a sacrifice.

IMPLICATIONS FOR CHINESE RETURNS ON CAPITAL: A COMPARISON TO INDIA

Primarily as a result of heightened competition, returns on capital have generally been less sustainable in China than in some Western-style economies. In India, for example, competitive advantages such as proprietary technologies, barriers to entry and economies of scale have tended to be more enduring.

Additionally, the coalition led by Prime Minister Narendra Modi has enacted a series of business-friendly reforms in India that have allowed long-running investment themes to play out more fully and with less regulatory interference than might otherwise have been the case. For these reasons, our emerging markets strategies and funds at Wasatch have typically been structurally overweight in India and underweight in China compared to their respective benchmarks.

To the extent that recent events in China foreshadow a more activist role for the government in determining how businesses are run, returns on capital may become compressed somewhat further—perhaps both in amplitude as well as duration. However, we believe companies will still be permitted reasonable levels of profitability.

Capitalism has enabled China to bring hundreds of millions of its citizens out of abject poverty. With much work still remaining, the government clearly understands the profit motive’s essential role in spurring the innovation necessary for China’s continued growth and development.

______

ADDITIONAL INFORMATION

For both India and China, we believe our legacy in small- and mid-cap investing gives Wasatch a competitive edge—as smaller companies may be better-positioned to grow for longer periods. Moreover, members of our investment team speak Mandarin Chinese and the Indian languages Hindi, Malayalam and Gujarati.

For clients who are registered to accept securities traded on foreign stock exchanges, our investment strategies can be structured as separately managed portfolios. Otherwise, we offer the convenience of mutual funds—the Wasatch Emerging India Fund and the Wasatch Greater China Fund.

RISKS AND DISCLOSURES

Mutual-fund investing involves risks, and the loss of principal is possible. Investing in small-cap funds will be more volatile, and the loss of principal could be greater, than investing in large-cap or more diversified funds. Investing in foreign securities, especially in emerging markets, entails special risks, such as unstable currencies, highly volatile securities markets, and political and social instability, which are described in more detail in the prospectus.

The Wasatch Greater China Fund is subject to risks associated with investments in China and countries in the greater China region that could affect the value of your investment in the Fund, including government control over currencies, economic conditions, industries and specific issuers, as well as continued strained international relations, uncertainty regarding taxes, and limits on credible corporate governance and accounting standards. Because of its exposure to greater China, including mainland China and China’s special administrative regions, such as Hong Kong, the Fund is subject to greater risk of loss as a result of volatile securities markets, adverse exchange rates and social, political, military, regulatory, economic or environmental developments, or natural disasters that may occur in the China region. The imposition of tariffs or other trade barriers by the U.S. or foreign governments on exports from China may also have an adverse impact on Chinese issuers. The Fund may invest in the securities of Chinese issuers through the China Stock Connect program. Trading through the Stock Connect Programs is currently subject to a daily quota, which limits the maximum net purchases by all purchasers using the Stock Connect Programs each day. While the daily quotas are relatively large, there is the possibility that the quotas could be reduced or exceeded, meaning buy orders for China A-shares would be rejected, affecting the Fund’s ability to efficiently execute on its investment strategy. Being non-diversified, the Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit wasatchglobal.com or call 800.551.1700. Please read the prospectus carefully before investing.

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflect the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

Wasatch Advisors, Inc., trading as Wasatch Global Investors ARBN 605 031 909, is regulated by the U.S. Securities and Exchange Commission under U.S. laws which differ from Australian laws. Wasatch Global Investors is exempt from the requirement to hold an Australian financial services licence in accordance with class order 03/1100 in respect of the provision of financial services to wholesale clients in Australia.

The primary investment objective of the Wasatch Emerging India and Wasatch Greater China funds is long-term growth of capital.

As of September 30, 2022, the Wasatch Emerging India and Wasatch Greater China funds were not invested in Taiwan Semiconductor Manufacturing Co. Ltd. Reliance Jio and Ant Group are privately held companies.

Wasatch Advisors, Inc., doing business as Wasatch Global Investors, is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Global Investors.

CFA® is a trademark owned by the CFA Institute.

DEFINITIONS

The global financial crisis, also known as the 2008–2009 financial crisis, is considered by many economists to have been the worst financial crisis since the Great Depression of the 1930s.

Gross domestic product (GDP) is a basic measure of a country’s economic performance and is the market value of all final goods and services made within the borders of a country in a year.

GDP per capita is a measure of the total output of a country that takes the GDP and divides it by the number of people in the country.

An initial public offering (IPO) is a company’s first sale of stock to the public.

Return on capital is a measure of how effectively a company uses the money, owned or borrowed, that has been invested in its operations.

Valuation is the process of determining the current worth of an asset or company.

The MSCI China Index captures large- and mid-cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g., ADRs). The index covers about 85% of this China equity universe. Currently, the index includes large-cap A shares and mid-cap A shares represented at 20% of their free float adjusted market capitalization.

The MSCI India Investable Market Index (IMI) covers all investable large-, mid- and small-cap securities across India, targeting approximately 99% of the Indian market’s free float adjusted market capitalization.

The MSCI Emerging Markets Index is a free float adjusted market capitalization index designed to measure the equity market performance of emerging markets.

The MSCI Emerging Markets Small Cap Index is a free float adjusted market capitalization index designed to measure the equity market performance of small company stocks in emerging markets.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non- infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

The Russell 1000 Index is an unmanaged total return index of the largest 1,000 companies in the Russell 3000 Index. The Russell 1000 typically comprises about 92% of the total market capitalization of all listed stocks in the U.S. equity market. It is considered a bellwether index for the performance of large company stocks.

The Russell 2000 Index is an unmanaged total return index of the smallest 2,000 companies in the Russell 3000 Index. The Russell 2000 is widely used in the industry to measure the performance of small company stocks.

The Wasatch strategies and funds have been developed solely by Wasatch Global Investors. The Wasatch strategies and funds are not in any way connected to or sponsored, endorsed, sold or promoted by the London Stock Exchange Group PLC and its group undertakings (collectively, the “LSE Group”). FTSE Russell is a trading name of certain of the LSE Group companies.

All rights in the Russell indexes vest in the relevant LSE Group company, which owns these indexes. Russell® is a trademark of the relevant LSE Group company and is used by any other LSE Group company under license.

These indexes are calculated by or on behalf of FTSE International Limited or its affiliate, agent or partner. The LSE Group does not accept any liability whatsoever to any person arising out of (a) the use of, reliance on or any error in these indexes or (b) investment in or operation of the Wasatch strategies and funds or the suitability of these indexes for the purpose to which they are being put by Wasatch Global Investors.

Indexes are unmanaged. Investors cannot invest in these or any indexes.

©2022 Wasatch Global Investors

Wasatch Funds are distributed by ALPS Distributors, Inc. Separately managed accounts and related investment advisory services are provided by Wasatch Global Investors, a federally registered investment advisor. ALPS Distributors, Inc., is not affiliated with Wasatch Global Investors.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits