Portfolio allocators rarely rely on one single factor when making investment decisions. Just because something is cheap, for example, doesn’t mean you should buy it. Investment results tend to be more favorable when multi-factor variables align themselves toward a specific investment outcome. This logic is particularly important in volatile and uncertain environments. Today, we believe there are five factors affecting emerging markets which point toward an attractive risk/reward for investors.

1. The Macro cycle

Since 1995, there have been five Federal Reserve interest rate-hiking cycles and they have all had several things in common. In the months leading up to the initial hike, market uncertainty tends to prevail and risk assets suffer as investors worry over inflationary pressures and potential central bank policy response. There’s speculation over the possible trajectory and cadence of future rate hikes and their potential effect on risk asset classes. In addition, the U.S. dollar tends to outperform both developed and emerging market currencies, and cyclical, value-oriented stocks tend to outperform growth-skewed companies.

In this cycle the Fed has so far hiked rates six times. We would argue that the cycle is advanced and the uncertainty surrounding the cadence and trajectory of future hikes is fading. U.S. rates may rise further but at a slower more predictable pace. At this point in the cycle, as Fed policy becomes less uncertain, risk assets tend to find their feet. At the same time, the U.S. dollar tends to stop appreciating against developed and emerging currencies and the growth-oriented stocks rebound against value stocks.

2. China

Experienced investors generally accept that emerging markets are often less predictable and more volatile than some other equity asset classes, such as European and North American stocks. Over the past 30 years, there have been many instances when emerging markets equities have fallen more than 15%. But it’s less common for emerging markets to fall over 30% in 18 months and even more infrequent for a major market, like China, to fall over 50% in that period. That’s exactly what has happened since May 2021.

China has been battered by several well-publicized headwinds, including the government’s regulatory targeting of Chinese monopolies (especially within the tech and e-commerce space), the default of several Chinese property developers and the massive negative economic impact of China’s zero-COVID policies. These headwinds have all led to a downgrade in earnings forecasts for Chinese companies.

Our job is to attempt to discount which of these headwinds has been priced into markets and consider whether risk factors could improve. We believe all these challenges may have peaked in terms of their negative effects on risk premium of Chinese equities, particularly the two largest headwinds— government regulation and China’s COVID policy.

"The broader investable universe gives active managers a toolbox to create portfolios with positions in industries which can thrive within inflationary environments and offset the headwind of a temporary slowing of global growth."David Dali, Head of Portfolio Strategy

3. Not just China

Market conditions today–with rising inflation being driven in part by higher commodities prices–have added support to many emerging markets, and not just in Asia, some of which have smaller benchmark or no benchmark representation.

This dispersion of emerging country returns has been dramatic. Active managers who have looked across geographies and created ballast within their portfolios by diversifying their sector and factor holdings have had success. For example, Turkey’s equity market is made up of 34% industrials whereas in China it is 5.6%. Brazil has 28% in financials, 20% in materials and 17% in energy. Indonesia and Saudi Arabia have about 50% of their public companies in the financials sector, which has been able to outperform in an interest rate-rising environment. India, on the other hand, with its young, educated population and information technology servicing prowess, is slowly capturing manufacturing business from China.

The bottom line is that emerging market constituents are diverse. The broader investable universe gives active managers a toolbox to create portfolios with overweight positions in industries and companies which can thrive within inflationary, commodity driven environments and offset the headwind of a temporary slowing of global growth.

4. Valuations

At Matthews, we are fundamental, bottom-up stock pickers. Our analysts and portfolio managers screen for characteristics, conduct deep dive analysis on business and management quality, and toward the end of the stock selection process we look at valuations. If valuations look appropriate a stock could enter the portfolio but if a great business is expensive it may go onto a watch-list. The same rationale holds when analyzing the attractiveness of an asset class like emerging markets.

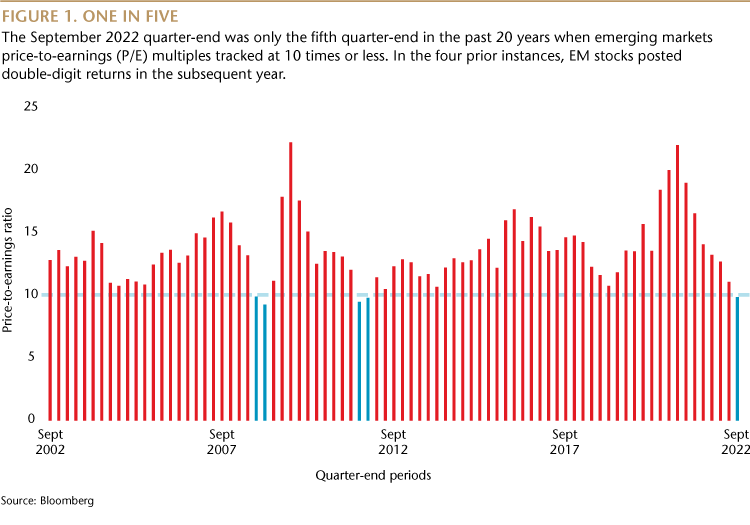

Looking back 20 years (or 80 quarters), there have only been five end-of-quarter instances when the MSCI Emerging Markets Equity Index has registered a price-to-earnings (P/E) multiple of 10 times or less. The September quarter-end was one of them, with a P/E of 9.96 times. Of the prior four instances, the median index total return for the subsequent one year was 19.03% and for the subsequent two years it was 31.47%. And in all the prior cases, the five-year total returns were positive. We believe this pattern bodes well for the point in the cycle we are at today.

5. Tangible Innovation

While innovative sectors like IT and health care have been primary drivers of emerging market returns over many years, we believe the theme is just getting started. In simplistic terms, we view Asia and China innovation today as roughly equating to the U.S. innovation period of the late 1980s and ’90s, when Microsoft, Genentech, Apple and Nike, and Google, Amazon and Facebook respectively were laying down their foundations. Asia and China’s current stage of development, buying power and consumer preferences, point to a similar path of demand for innovation. We believe innovation should be a core growth theme within an emerging markets allocation and the Matthews Asia Innovators Active ETF (ticker: MINV) puts this theme into practice.

Innovation, particularly in Asia and China, is also trading at Black Friday prices. Within the MSCI China Index, for example, innovative sectors like IT are trading at a P/E ratio of 14 times, which is a 67% discount from its five-year high. Health care is at a 64% discount to its five-year high and communication services is at an 86% discount.

A word about benchmarks

Portfolio allocators need to rationalize when to use a passive strategy and when to select an active one. Some asset classes, like emerging markets, are more suitable for active management in our view because their benchmarks fail to represent the investable opportunities that exist. Emerging market benchmarks also cannot vet quality and corporate governance and they don’t include world class companies doing business within emerging market economies if they are domiciled outside those economies. Perhaps most topically, active managers in emerging markets, unlike benchmark-tracking strategies, can be cognizant of geo-politics and government policy and take steps to mitigate the impact of both.

David Dali

Head of Portfolio Strategy

Matthews Asia

Definitions:

Price-to-earnings (P/E) ratio: a ratio for valuing a company that measures its current share price relative to its earnings per share (EPS).

MSCI Emerging Markets Index: captures large and mid-cap representation across 25 emerging markets. The index covers approximately 85% of the free float-adjusted market capitalization in each country.

MSCI China Index: measures large and mid-cap representation across China securities listed on the Shanghai and Shenzhen exchanges.

It is not possible to invest directly in an index.

As of October 30, 2022, accounts managed by Matthews Asia did not hold positions in Microsoft, Roche (Genentech), Apple, Nike, Alphabet (Google), Amazon and Meta (Facebook).

© Matthews Asia

Read more commentaries by Matthews Asia