As Europe struggles with war, costly energy, record inflation and slowing growth, it’s no surprise that European corporate credit is out of favor. But in our view, bond prices already reflect a lot of bad news. Has the time to buy arrived?

In the face of geopolitical and economic storms, European investment-grade and high-yield credit have both slumped this year, leaving valuations cheaper than at any time since the global financial crisis (GFC) and yields higher than US equivalents. But with the European Central Bank (ECB) set to continue hiking rates, and with a tough winter in store, most investors remain wary. Even so, at current yield levels it’s important to see the issues in context.

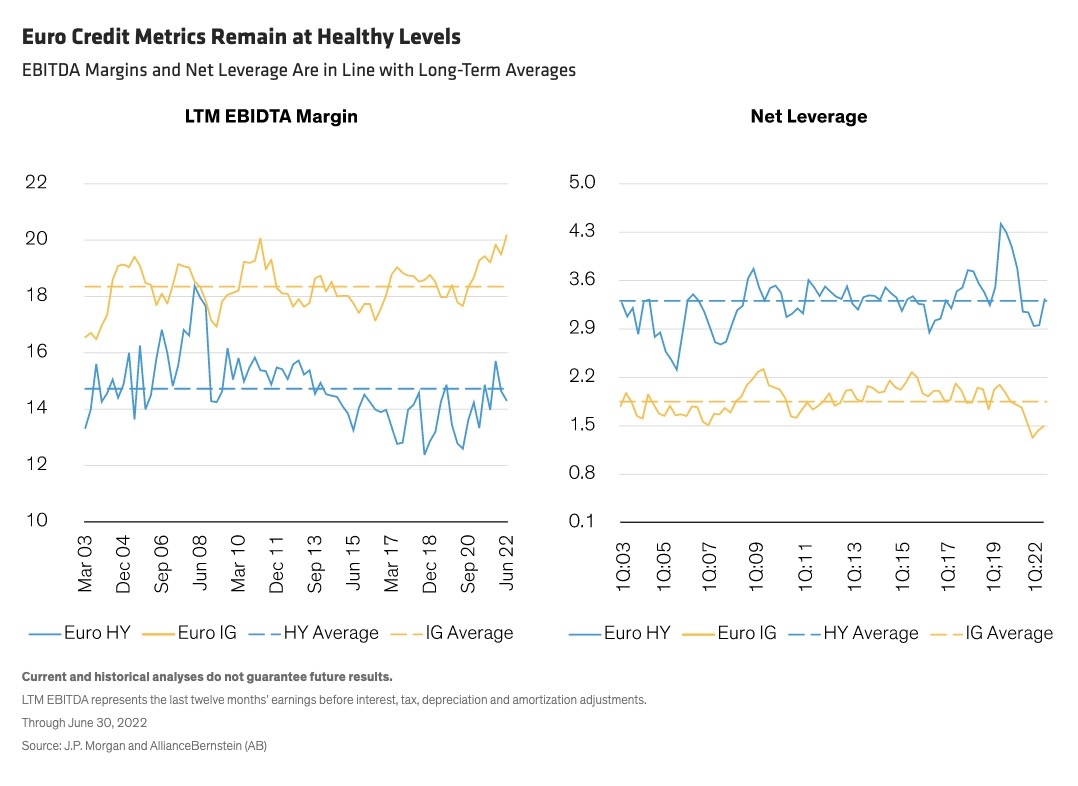

European Credit Has Solid Fundamentals

European corporates are fundamentally in good shape. They’ve bounced back from the COVID emergency period, reducing their leverage and restoring margins (Display, below). So at this point, both their balance sheets and pricing power seem resilient.

Cash-to-debt levels are high right now, a further indicator that European corporates are prepared to weather another challenging period. Of course, if European economies enter a recession, which seems likely, we expect those metrics to weaken, but the starting point is certainly strong.

Technical factors in the market are still modestly supportive. The ECB has ended its major bond-buying programs, but is still reinvesting the proceeds from its investment-grade holdings, providing some continuing support for this part of the market. Meanwhile, euro credit issuance has fallen away sharply, keeping supply balanced with demand.

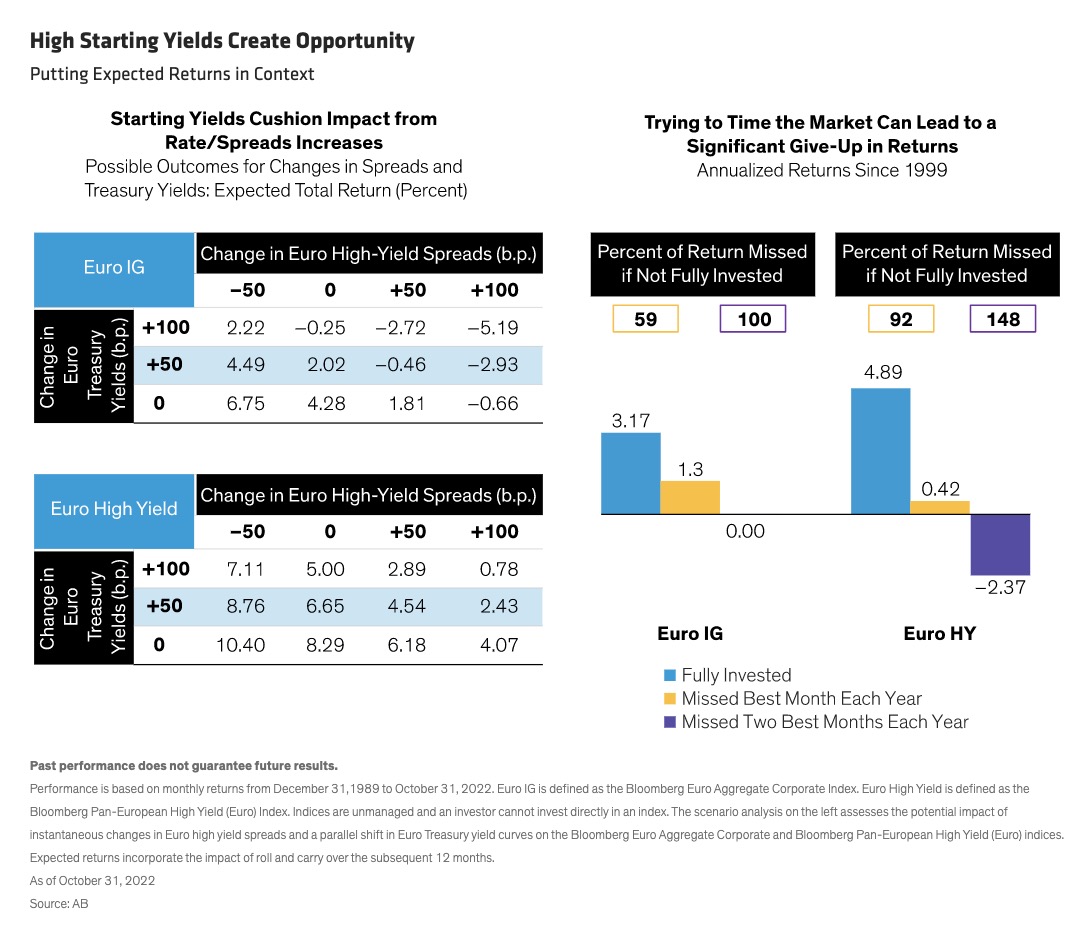

Euro Credit Valuations Are Compelling

Euro rates are set to increase, and credit spreads may widen further in 2023. But we don’t think Europe faces another GFC-style environment. Instead, we anticipate a shallow recession with rates plateauing towards the end of the year. While that scenario may be challenging for equity investors, we think it’s likely to be benign for bondholders, who focus on return of capital rather than earnings growth.

Markets are implying a terminal interest rate of around 3% for the ECB—in line with our own forecasts—which should be manageable for most European corporations. And we think the period of aggressive interest-rate hikes and related shocks for investors is likely over. Against that prospective backdrop of relatively stable rates, euro investment-grade and high-yield bonds offer not only attractive spreads but also absolute yields of over 3% and 7% respectively. We think that’s an environment where credit may perform well.

Potential Upside for Euro Investors

On a currency-hedged basis, those yields are significantly higher for euro investors than equivalent US credits. And while the exact turning point for credit performance is hard to predict, they offer a substantial cushion against possible rate increases and spread widening (Display, left). Historically, credit has rebounded quickly from crisis periods, and investors who bought into credit while yields were high reaped the benefits. In contrast, those who stayed on the sidelines and tried to time their entry point risked missing out on the best-performing periods (Display, right).

Starting Yield Has Been a Strong Indicator of Future Returns

Investors in euro credit face a potentially volatile 2023 and will likely not see lower rates or sustained tighter credit spreads before the end of next year. But these bonds already generate attractive income—and usually, such periods of elevated yield levels don’t last for very long.

In our view, higher yields today could translate into attractive risk-adjusted returns on both investment-grade and high-yield bonds over a five-year time horizon. That’s because historically, starting yields have been correlated with future returns over a three- to five-year window. Of course, market conditions might deteriorate, and yields could rise from here, offering a better entry point. But investors need to weigh the probability of that scenario unfolding against the risk of losing out on annualized returns similar to current yields.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. Views are subject to change over time.

© AllianceBernstein

Read more commentaries by AllianceBernstein