The uncertainty of a looming recession and high market volatility makes almost all investment options look doubtful as investors search for safe and reliable investment tools. Given the current market situation, is there any viable and practical solution to secure investors' funds and generate a positive return available for investors? Investment Director of Sigma Global Management herein shares his perspective on the situation.

- Is the downturn in a global economy really critical and the recession is inevitable?

Central banks across the world have been raising key interest rates in an attempt to halt the inflation that is running at 40-year highs. The Fed raised interest rates three-quarters of a percentage point for the third time in a row this year, bumping the federal funds rate to a target range of 3.25 to 3.50 percent. BoE raised its key interest rate by 0.5% to 2.25%, which is the highest level in 14 years. The Central bank of Switzerland joined the flurry of rate hikes by announcing an interest-rate rise that would bring its benchmark lending rate above 0% for the first time in eight years. Swedish Central bank increased its key interest rate by 1 percentage point to 1.75%, marking the biggest hike in almost three decades. For the first time in 24 years, the Bank of Japan intervened in the foreign exchange market to prop up the abrupt plunge of the yen, as rising import costs have been disrupting the country's broader economy.

In September, the British pound touched its lowest point in 37 years against the dollar. The Dollar gained 1 percent against a basket of currencies of major U.S. trading partners. The euro keeps lingering at its lowest levels against the dollar, not seen since 2002. A surging greenback can stifle the profits of U.S. multinationals and take a toll on global trade, with so much of it transacted in dollars.

The US GDP has seen another decline of 0.6% in the second quarter. The spread between 10-year and 2-year Treasuries is (-)0,37%. It has been inverted since early July with the shorter-term yield exceeding the longer-term yield.

S&P 500 index YTD is (-)24,71%, Dow Jones index YTD is (-)19,44%, Nasdaq YTD is (-)32,62%.

All the signs are in place pointing to an upcoming recession.

- Thank you. It appears that the stock market is not doing so well. What can you say about typical 60/40 portfolio and other long only strategies, - can any of them offer an adequate return on investment in such volatile time?

Some investors are convinced that maintaining long-only positions on the diversified stock will eventually yield the desired return. Diversifying a portfolio of stock across multiple sectors of the economy appears as a sensible approach.

For instance, C3.ai - is a software developing company that creates artificial intelligence and has a capitalization of 2 billion. They went public in 2020 at $42 per share. The company runs businesses all over the globe: in the USA, Europe, the Middle East, Africa, and Asia. The software they develop is applicable for industrial and commercial scaling in different industries. Their product is quite diversified and has a vast scope of application across multiple industries: oil and gas sector, utilities, banking, military industry, healthcare, retail, government structures, and transport. The company recently received contracts from Raytheon Technologies - RTX. RTX chose C3 ai (AI) and their platform to implement artificial intelligence and machine learning for US Army tactical intelligence. The company also received $90,000,000 worth of contracts from the US Department of Health and Human Services.

Holding long positions in the stock of this promising company along with holding position in other companies’ growth stocks may seem as a promising investment, but Nasdaq Index of hi-tech growth companies has seen a sizeable slump of (-)33%, and C3.ai stock has now hit a drawdown (-)62% YTD.

To illustrate the situation better, let us examine the charts 1-3 below with data generated from a portfolio visualizer analysis, where the performance of three sets of portfolio assets is compared with each other and with the SPDR S&P 500 ETF Trust. The tracking period runs from August 2021 up until now, - October 2022.

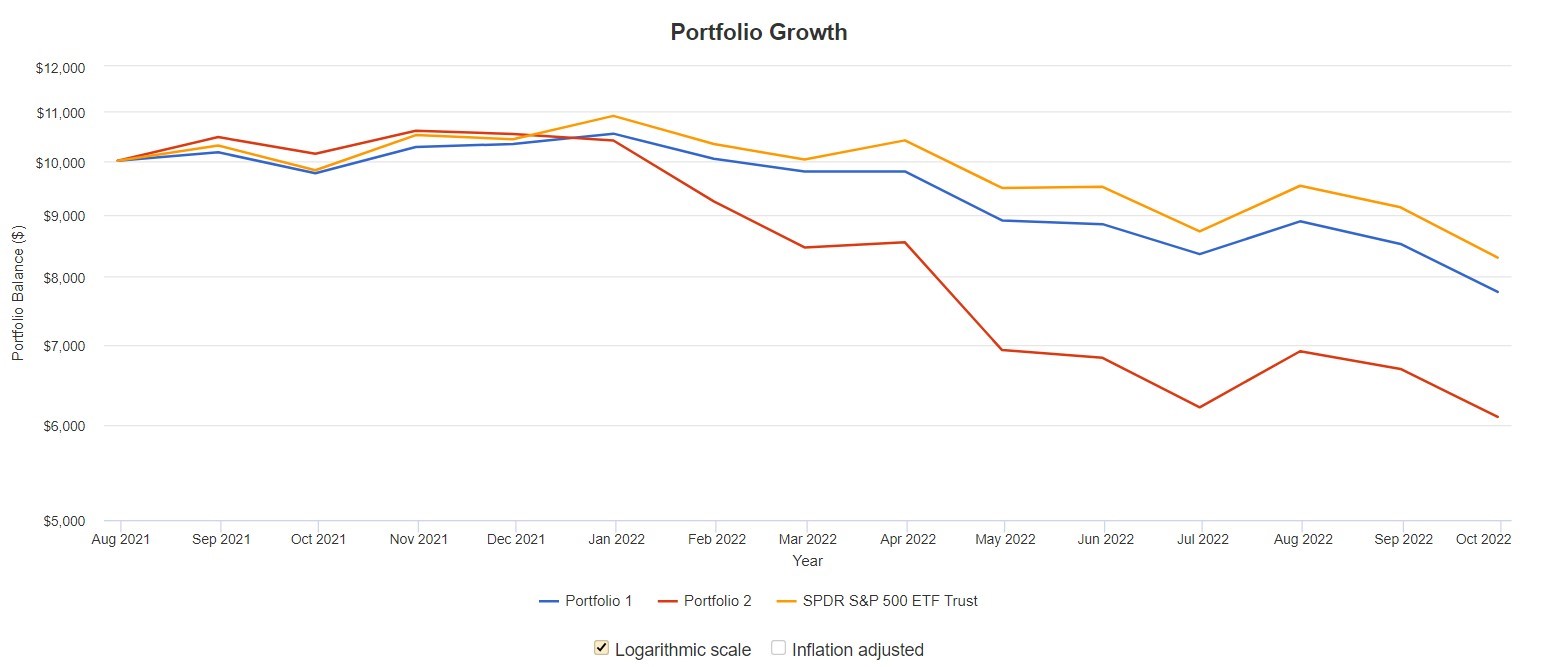

Chart 1: Portfolio Growth

Chart 2: Trailing Returns

Chart 3: Portfolio Returns

The chart above designates that the (YTD) performance and performance over 14 tracked months of a Typical 60%/40% portfolio (Portfolio 1) that consists of 60% allocated to SPY stocks and 40% invested in 20+ Year Treasury Bonds (TLT) has had substantial YTD (-26.32%) and CAGR (-19.51%) drawdowns, which are typical of the current bear market situation. The performance of FAANG portfolio (five major US high-tech companies - Facebook, Amazon, Apple, Netflix, and Google, (Portfolio 2)) indicates sizeable YTD (-41.33%) and CAGR (-34.53%) negative returns. The performance of the SPDR S&P 500 ETF Trust benchmark also does not look comforting, - (-23.93%) YTD and (-14.80%) CAGR, although it is the best performing out of the three long allocations.

We have to admit: the results above cannot inspire investors to allocate their funds into any of the portfolios above.

- Is there any type of a portfolio allocation strategy that can help mitigate investors’ risks more and generate positive return given the turmoil of the given situation?

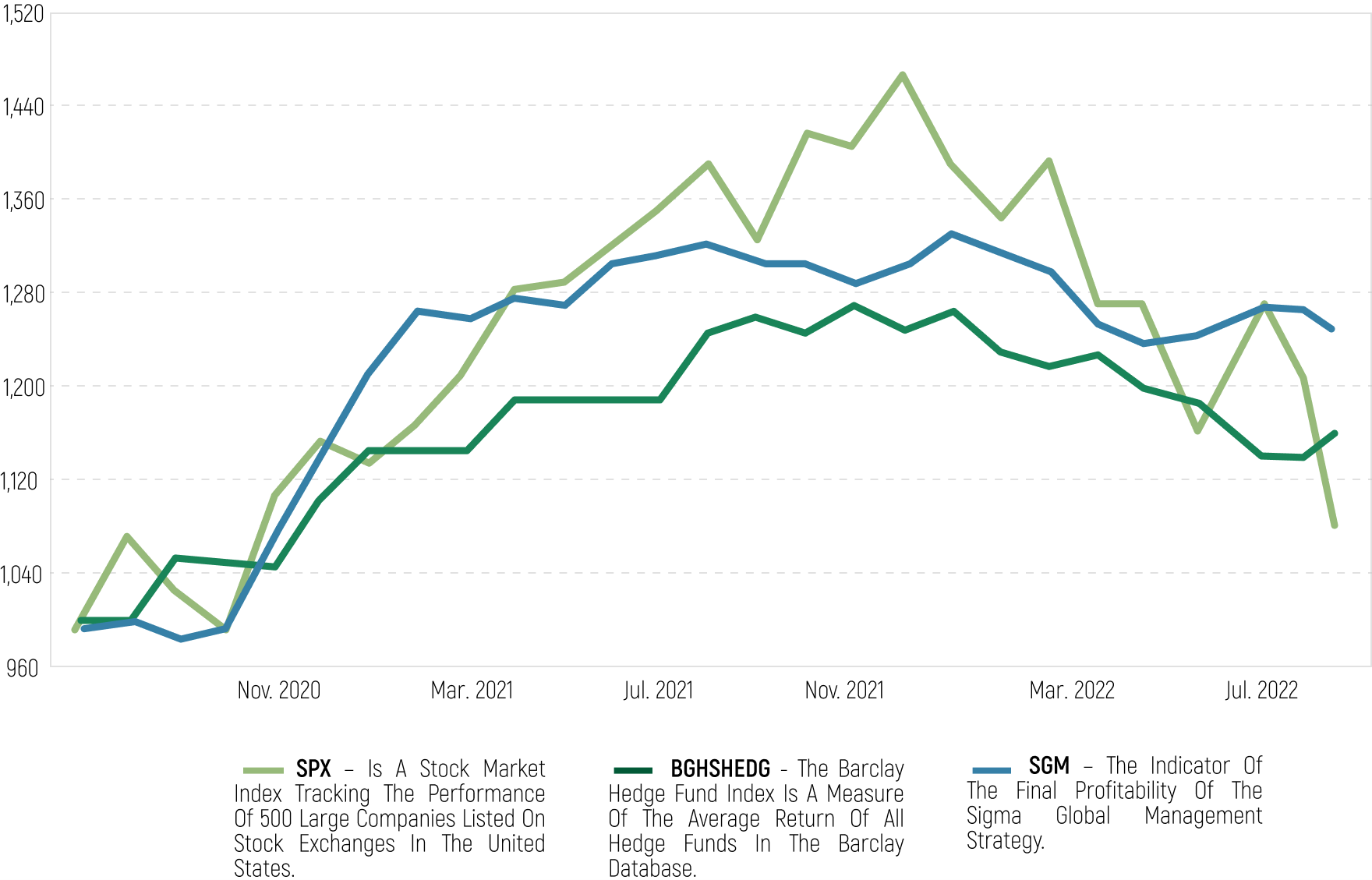

Let us compare several examples. Examining charts 4 and 5 below that compares the performance of the Barclay Hedge Fund Index, which utilizes long and short positions, arbitrage, and a long-short strategy utilized by an asset management company Sigma Global Management against the SPY index, we can gather that both the Barclay Hedge Fund Index and Sigma long-short strategy show better returns (CAGR): 16% for Barclay Hedge Fund and 24% for Sigma long short strategy vs 9,6% for SPY. In fact, Sigma’s long-short strategy has outperformed the SPY by 2,5 times.

Chart 4: Compared CAGR on BGHSHEDG and SGM strategies vs. SPX.

Chart 5: Compared Risk Metrics of BGHSHEDG and SGM strategies vs. SPX

The results of both risk-adjusted evaluations of return on investment provided by Barlclay’s Hedge Fund, Sharpe ratio and Sortino ratio, exceed the similar SPY values by 3 and 4 times, respectively.

The results of both risk-adjusted evaluations of return on investment provided by Sigma’s long-short strategy, Sharpe ratio and Sortino ratio, exceed the similar SPY values by 4,35 and 7,74 times, respectively. The maximum drawdown of Barlclay’s Hedge Fund over the tracking period has been (-)9,80%, and the maximum drawdown of Sigma’s long-short strategy over the same tracking period has been only (-)6,71% vs (-) 24,77% by SPY. The results of Barclay Hedge Fund and Sigma demonstrate far better returns and risk assessment ratios than long only SPY, 60/40, FAANG and the SPDR S&P 500 ETF portfolio allocations.

- So, what does the trick of minimizing risks and losses to such a significant level?

It is a portfolio management strategy where the manager attempts to minimize market risk by taking both long and short positions. In a long-short portfolio strategy the risks of losses are minimized by buying undervalued stocks and selling overvalued stocks. The idea is that if the market declines and the long positions take losses, the short positions will provide gains and minimize overall losses and keep the portfolio profitable.

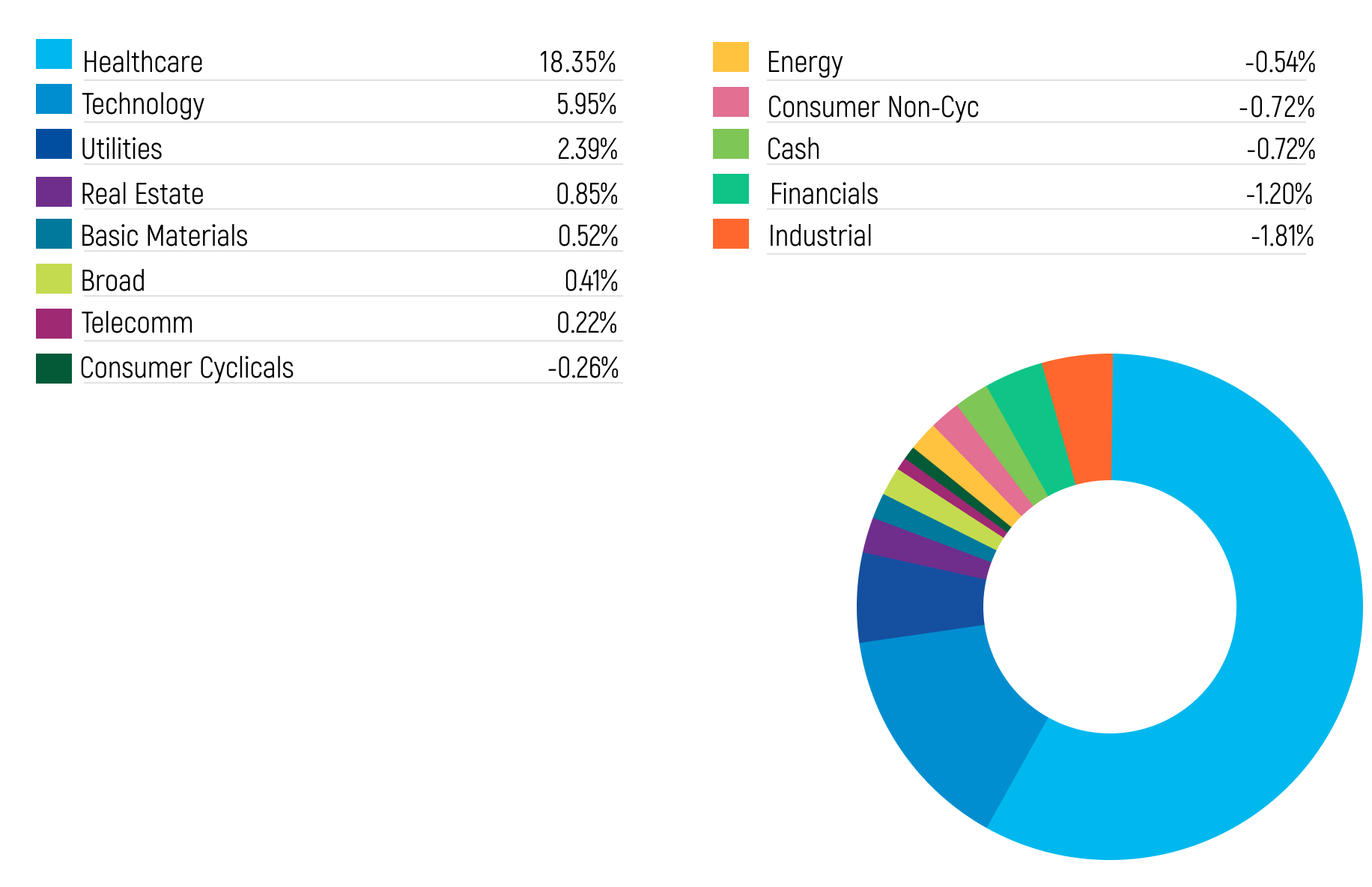

For example, Chart 6 below demonstrates how 28,69% of portfolio allocation in undervalued stocks of long exposure is balanced with 5,25% of portfolio allocation in overvalued stocks of short exposure.

Chart 6: Allocation of stock in long-short sector exposures

5. Ok, we can see the results of your strategy, but could you tell us a bit about what type of methodology you use to determine which stock is overvalued or undervalued?

Strictly speaking, our strategy does not employ only the mathematical volatility method. First, we allocate some funds in long positions by investing money in attractive, promising stocks and sectors, meanwhile keeping sufficient funds in long-short exposures intended to hedge these long exposures. Therefore, absent exposure of funds to net long positions, the net results of the applied methodology for determining long-short pairs would be different from the presented above and show a lower correlation with S&P 500, improved risk-assessment metrics, and lower return.

However, we keep allocations to the net long exposures to preserve an opportunity to achieve a performance of 20%, 30%, or higher than a similar stock market growth rate after the market has rebounded from a crisis-driven decline.

The core of our strategy centers on matching long-short pairs of stock, and this process undergoes several stages. We assess historical and current stock volatility levels and the propensity of stock to regression - a return of stock values to its average growth and decline rates.

The statistical and volatility analysis enables us to determine:

- whether the stock deemed undervalued is at its critical undervalued level relative to its average values or not;

-whether it is worthwhile to buy a stock perceived as undervalued, and whether this stock’s undervalued level has reached a critical point with regards to its average values or not;

-whether it is worthwhile to sell a stock deemed overvalued, or its upward movement is still within the normal volatility range, and the stock’s overvalued level is less obvious to signal a selloff.

In the first phase of implementing our long-short investment strategy through matching stock pairs, we conduct a systematic search of stocks that substantially deviate from their average values and average growth rates. In addition, we search for stocks that form an adequate, stable regression model, indicating the stock’s propensity to return to their historical average rates over a designated tracking period.

Among other things, we also use cyclical phase analysis on every stock, testing the stock’s performance, resistance to regression, and other volatility metrics in conditions consistent with the current cyclical phase of the market. As we have observed from the cyclical shift of the prevailing through 2021 bull market to the bear market we face now, and the shifts to bear markets of 2008, 1999, etc., stocks' volatility and propensity to regression can change depending on the market conditions. Therefore, we test each and every stock in order to find the most stable pairs that would be capable to demonstrate a reduced spread in all cyclical phases of the market movements, or in other words, return to their mathematically proved values.

The main point of this approach is to match up stock pairs that are completely neutral with respect to monetary beta exposure or correlation with the market, essentially ruling out the influence of any market dynamics factor on the long-short strategy core.

That said, however, we do track the list of promising companies that have the lead in innovation, cyber-technology, and biotechnology industries throughout all market phases, - be it the phase of such high descending volatility as we see now, or an ascending one. We allocate these companies’ stocks to excess long exposures that do not surpass 15-20% of the portfolio. By doing this not only do we strive to diversify our positions to manage risks better and detach from the market dynamics, but we also keep up with the pace of the market during a growth phase and maintain the strategy performance in line with the average returns of market indexes such as, for example, S&P 500.

Thank you for your attention, and we hope this explanation of the long-short strategy will help investors make up their minds about what approach to use to protect their assets better in these uncertain and volatile times. This was Vladislav Petlenko, Investment Director of Sigma Global Management.

© Sigma Global Management

Read more commentaries by Sigma Global Management