Let’s begin by reviewing how the markets are presently positioned. The equity market remains in a strong downtrend with many of our long held technical support levels being breached. Meanwhile, Capital Weighted Capital flows, Capital Weighted Volume and market breadth continue their bearish declines. In September, staunch S&P 500 support @ 3900 was violated. 3900 was the minimum target objective of the former Head and Shoulder’s pattern (measured by the top of the head to the neckline).

Additionally, this support level was tested several times and held, making the break of support that much more significant. Rarely do these chart patterns playout in such textbook fashion.

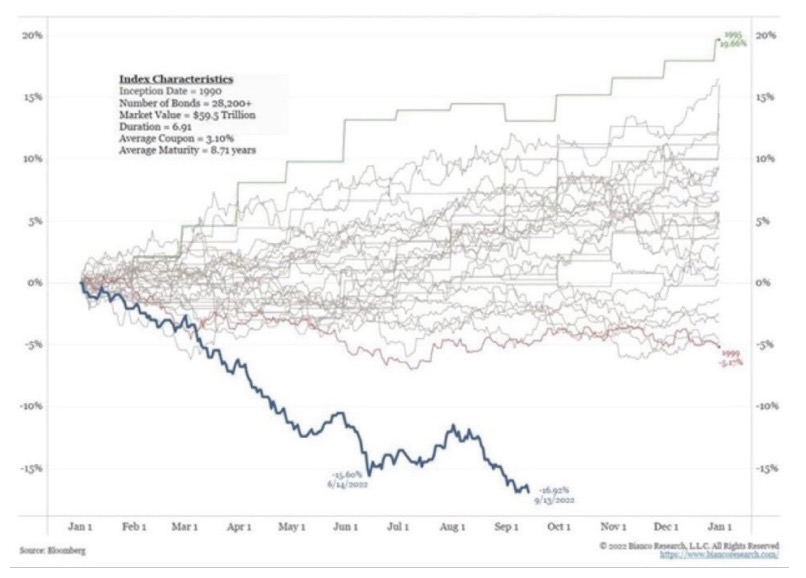

ILLUSTRATION 1: YTD TOTAL RETURN FOR THE BLOOMBERG GLOBAL AGGREGATE INDEX

Source: Bloomberg

ILLUSTRATION 2: S&P 500 HEAD & SHOULDERS PATTERN WITH VOLUME

Source: www.optuma.com/volumeanalysis

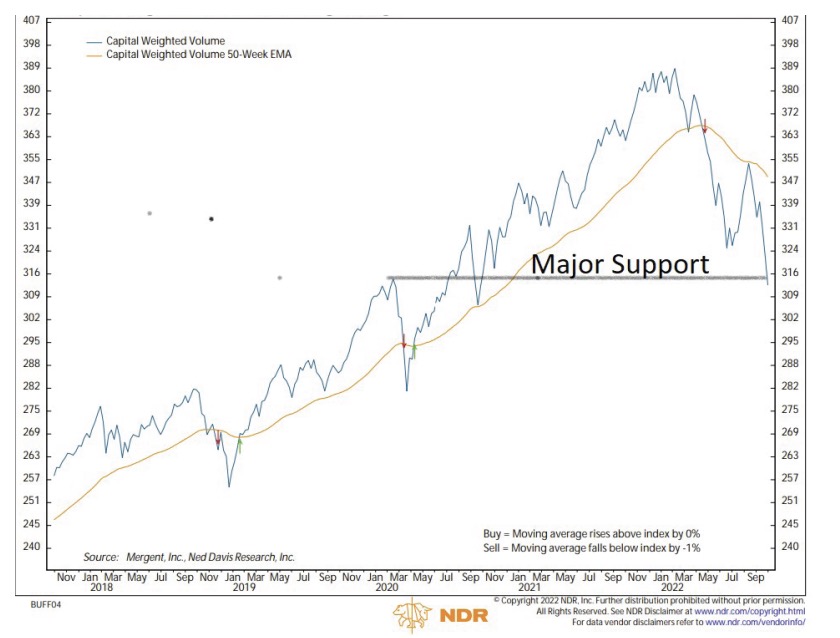

The all-time peak on the S&P 500 is just above 4800 while the trough support of the June lows was near 3600. That placed the midpoint between the peak and trough at 4200, our former critical resistance level. In midAugust, the S&P 500 surpassed 4300, breaking above the midpoint. Historically, during a bear market, the S&P 500 had never broken the prior lows after breaking through the midpoint. However, by September 16th, price and volume support both broke beneath additional levels of SPX support, closing just under 3900. Simultaneously, major SPX 500 Capital Weighted Volume cut through support at 331 like a hot knife through butter to make a new yearly low. This suggested SPX 3600 support was in serious jeopardy.

In our view, 3600 was very firm and staunch SPX 500 support. As, I mentioned earlier, never has the S&P 500 exceeded its midpoint (4200) to break through its prior lows (3667) during a bear market. Although it has never happened before, it did not mean it was impossible. Technically, earlier in the last week of third quarter, the market broke through the June lows on an intraday basis. And then on September 30th, the S&P 500 failed to close above the 3600 critical support.

Presently, our leading indicators of Capital Weighted Volume and the NYSE Advance-Decline line are both making new yearly lows. Capital Weighted Volume is presently flirting with breaking another major support level @ 315. This Capital Weighted Volume support corresponds to SPX 3510 support. Whether volume support breaks or bounces may be predictive of price’s direction. Should the market garner strength at these depressed levels, look for resistance @ 3830 and strong resistance @ 3900. Now that the 3600 support level has failed, the next S&P 500 support is 3550 & 3510, followed by major steadfast support @ 3410.

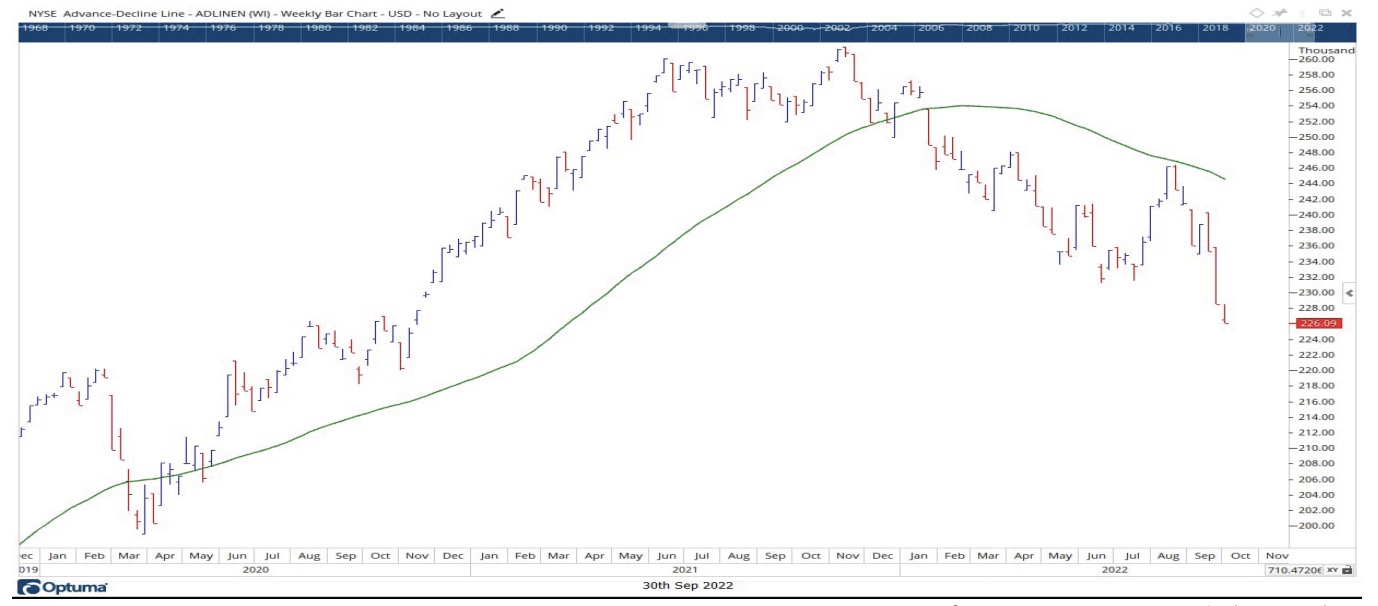

Concurrently, the NYSE Advance-Decline line also broke its April lows to make its own low of the year. Thus, our leading indicators, Capital Weighted Volume and market breadth are both leading the way down.

Now, that we have established the market trend is down and our leading indicators are confirming the decline, let us move on to the next topic.

• Has the bear market shown any signs of knuckling under?

We will begin this investigation by examining our indicators suggesting neutrality.

ILLUSTRATION 3: CAPITAL-WEIGHTED VOLUME VS MOVING AVERAGE

Source: NDR Ned Davis Research

ILLUSTRATION 4: NYSE ADVANCE – DECLINE LINE

Source: Optuma Software www.optuma.com/volumeanalysis

The Volatility Index (VIX), AKA “the fear index”, closed September just over 31. That compares to the Aprils VIX highs exceeding 33. Historically, final washout levels have exceeded 45. Thus, volatility could be suggesting investors may have yet to fully capitulate.

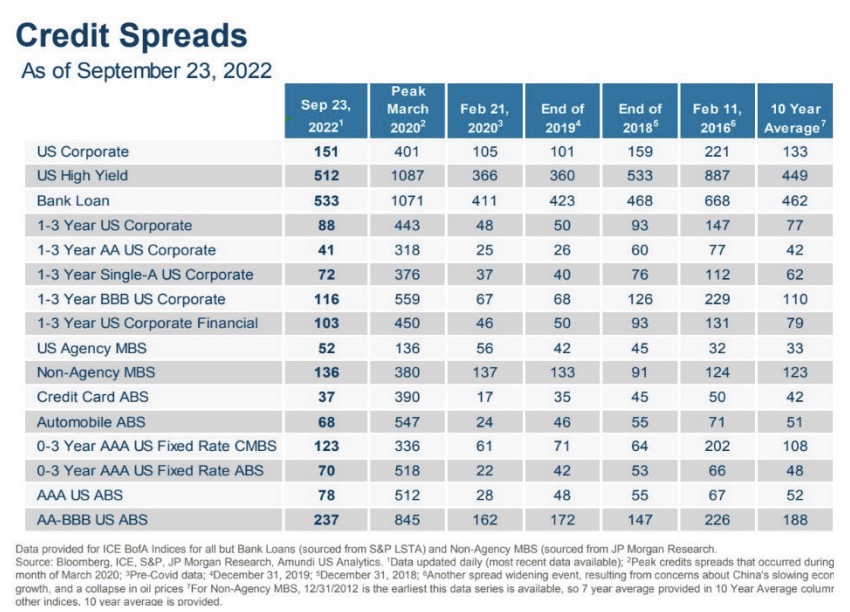

Another dataset that has not yet reached wipeout levels in our estimation is credit spreads. When market participants fear failure, they typically demand more yield from debt vehicles. Wider spreads between low grade credit and the highest credit (US Treasuries) display greater concerns of default. Wide credit spread extremes may correlate with market tops and bottoms.

Presently, both corporate debt and high yield debt are only slight above their 10-year averages. A lack of a high credit risk premium may suggest that immense fear has yet to be interjected into the debt markets.

ILLUSTRATION 5: VIX – VOLATILITY INDEX

Source: IBD, Investors Business Daily.

ILLUSTRATION 6: CREDIT SPREADS

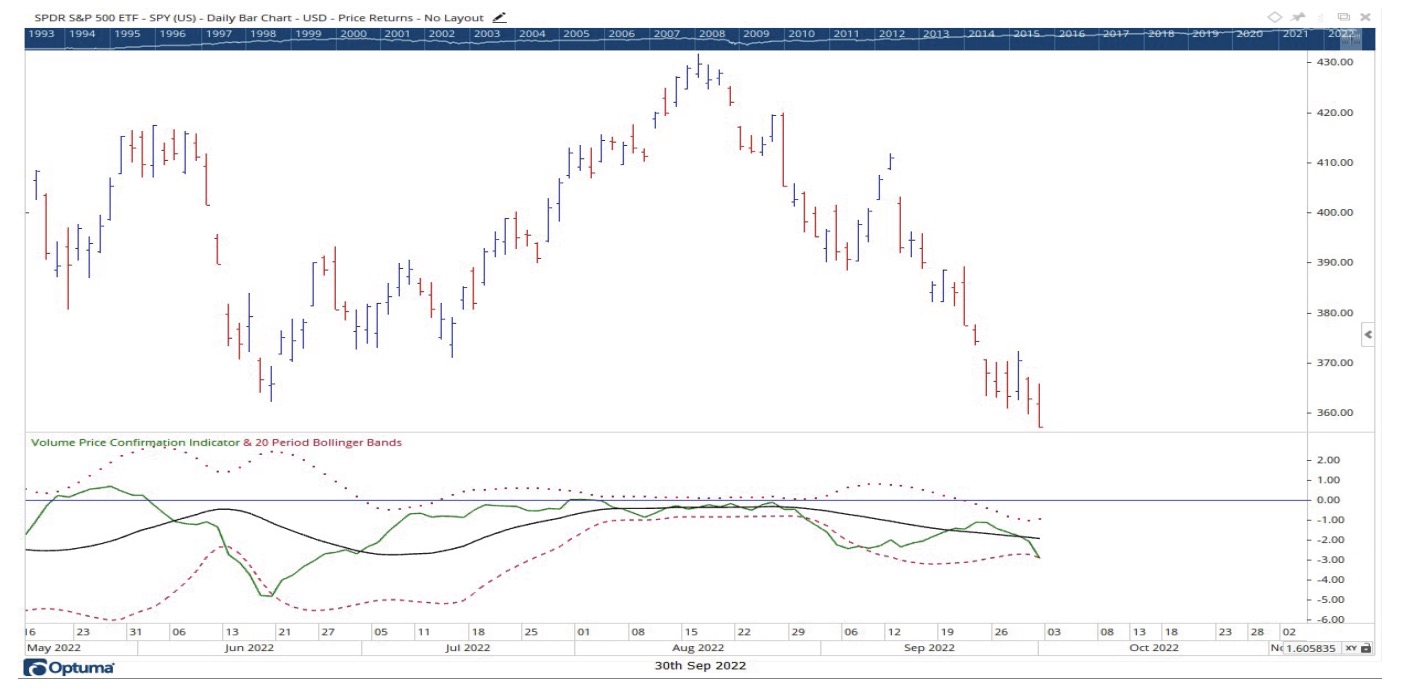

Finally, although the VPCI is trending down, it is still above levels associated with capitulation. In order to set up to washout levels, our proprietary VPCI V bottom needs to both fall below negative 4 as well as drop below two standard deviations from its 20-day mean.

On Friday, September 30th, the VPCI finally met its lower standard deviation band but has not yet reached the -4 oversold level. The setup appears to be coming together but keep in mind not all market bottoms are formed off this supply side imbalance setup.

Source: Amundi Pioneer Asset Management

ILLUSTRATION 7: VPCI – VOLUME PRICE CONFIRMATION INDICATOR

Although the short-term technical outlook still does not show the ideal setup for an immediate low being in play yet, on a sentiment basis, the intermediate and long-term outlook appears to be positive.

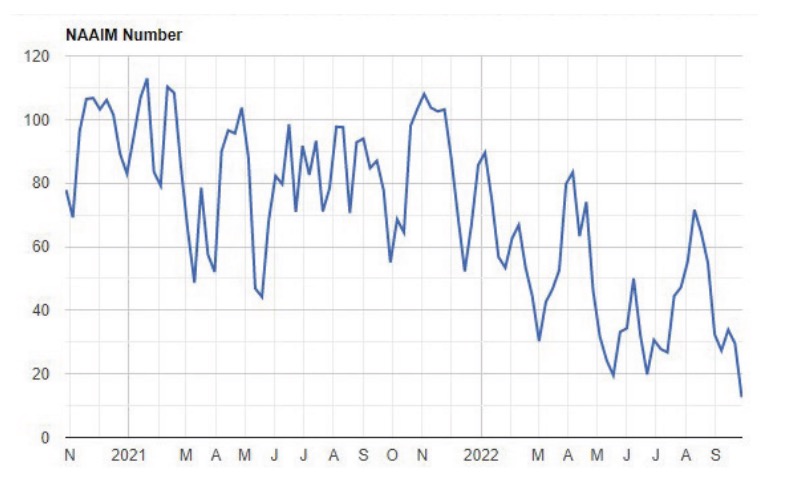

When sentiment is overly bearish, it can mean that most shortsighted investors have already sold. That leaves just the strong long-term investors who are reluctant to sell remaining. This potential bullish outlook is evidenced by the NAAIM sentiment survey showing less than 12% of active managers being bullish on the S&P 500. This is only the 9th time that bullish sentiment has fallen below 12% since 1998.

ILLUSTRATION 8: NAAIM BULLISH PERCENT SENTIMENT

Source: https://www.naaim.org/programs/naaim-exposure-index/

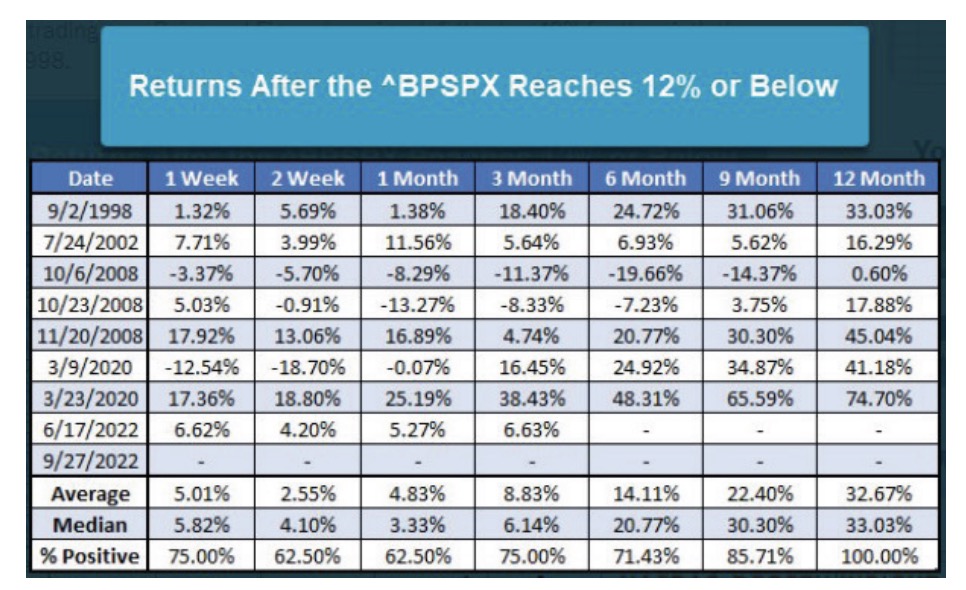

For the patient long-term investor, forward returns have historically been strong during this time of extreme pessimism. Although positive after a year, note there was a double dip in 2020 and triple dip in 2008. Those outliers of extreme outcomes could also be in play as well many other possibilities.

ILLUSTRATION 9: PAST S&P 500 RETURNS WHEN NAAIM BULLISH PERCENT IS BELOW 12

Source: Dorsey Wright Money Management, September 28, 2022.

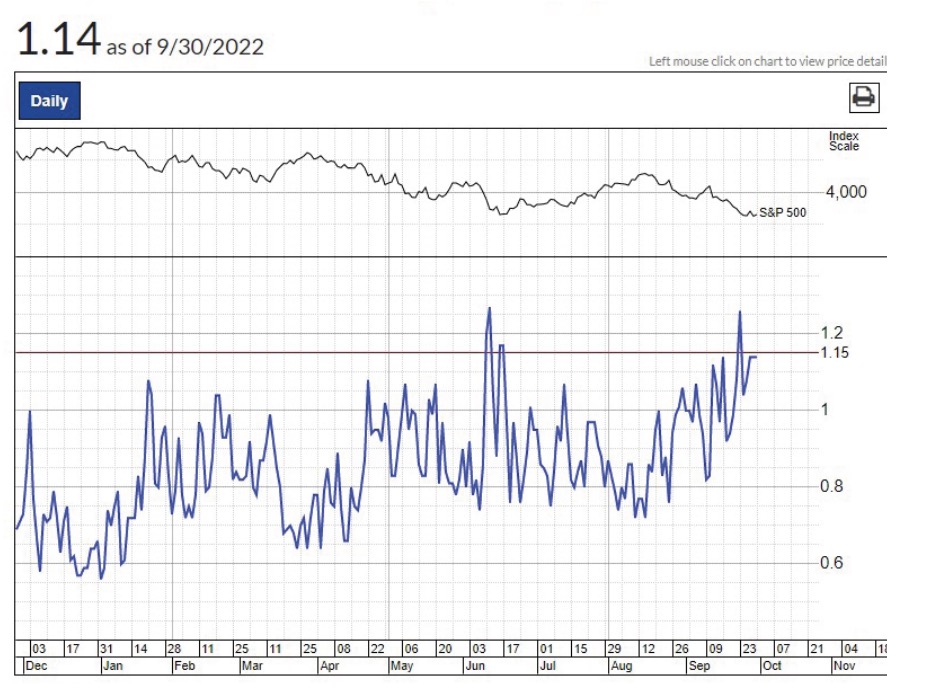

The gloom may also be overdone in the Put Call Ratio, another sentiment index measuring the actions of option traders who buy calls when optimistic and purchase puts when pessimistic.

Historically, the average ratio between bullish calls and bearish puts is around 0.7. Levels above 1 are considered overly bearish whereas levels above 1.15 have historically occurred in heavily oversold conditions. The end of the third quarter reading was 1.14.

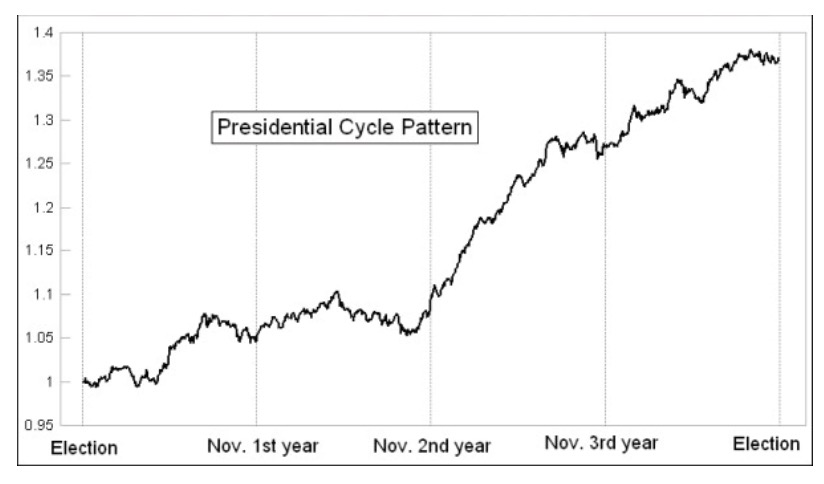

From a technical perspective, the most bullish scenario comes from cycle analysis. The presidential cycle may be the most prominent and perhaps strongest cycle in market cycle analysis. Within the presidential cycle, the strongest market cycle tends to be the third year of a first term President.

This is where the sitting President pulls out all the stops to help capture reelection. The average market return of a third-year president is 16.3%, compared to under 7% for the first and last years, while the second year has the lowest historical return just under 6%

ILLUSTRATION 10: PUT CALL RATIO

Source: IBD, Investors Business Daily.

The low of the presidential cycle is the second year before the midterms, historically bottoming out at the end of the third quarter. Elections can cause investors anxiety. However, once the outcome is believed to be known, investors have shown the ability to withstand the eventual result. It’s the unknown that causes investors fear and indecision. We are closing in on that phase now. This is typically the time when the outlook becomes clearer.

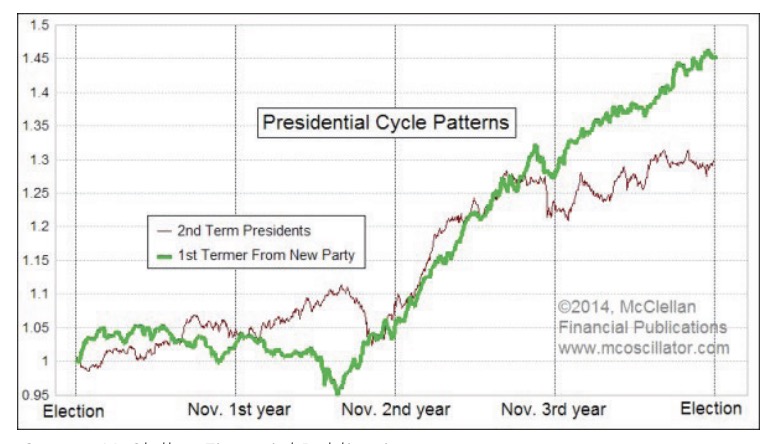

ILLUSTRATION 11: FOUR YEAR PRESIDENTIAL CYCLE

Source: McClellan Financial Publications

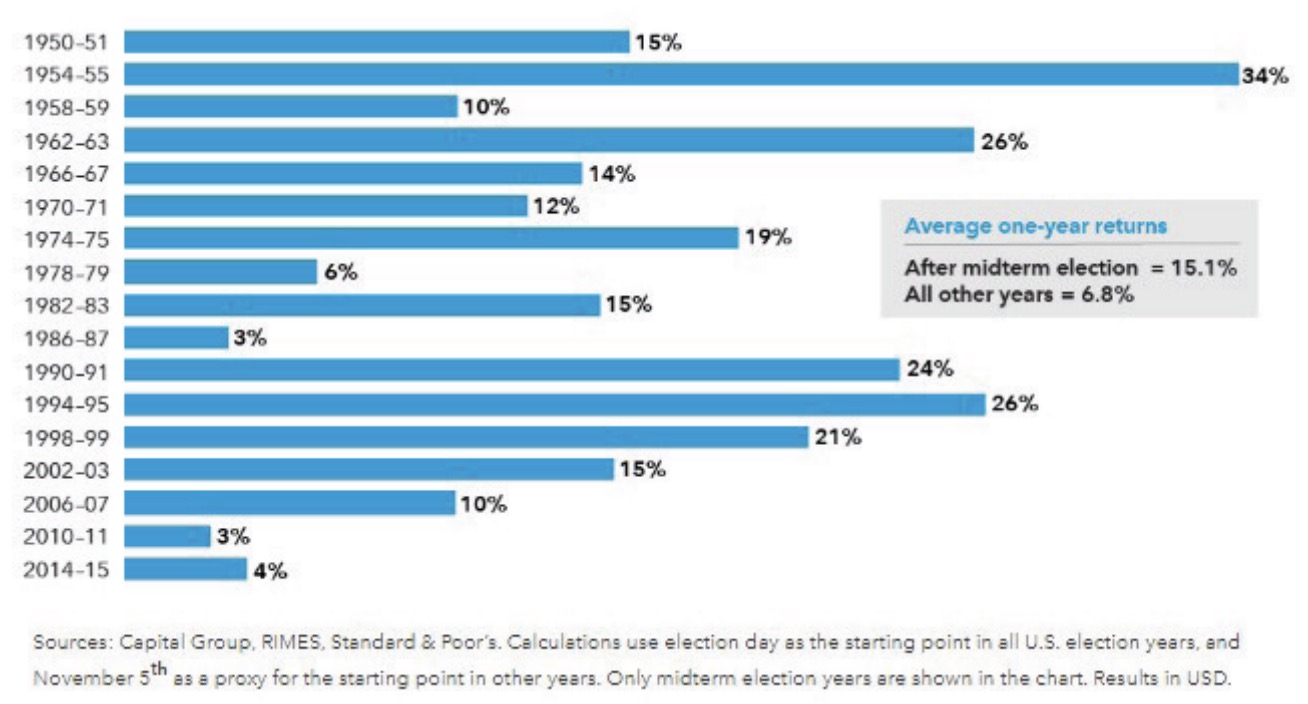

ILLUSTRATION 12: S&P INDEX PRICE RETURN ONE YEAR AFTER A U.S. MIDTERM ELECTION

Source: The Capital Group

Through consensus in the polling data, investors may start to feel more confident ahead of the actual election. Historically, according to the cycle, after the September presidential lows, October flattens out leading to a new bull market in November. This results in an average historical S&P 500 return of 15.1% in the year following the mid-terms since 1950. So, signs of hope may be just around the corner from a cyclical timing standpoint.

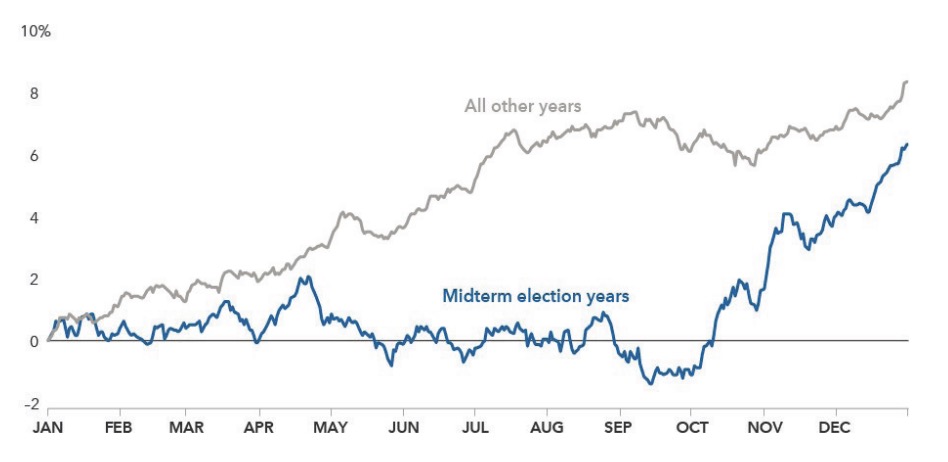

ILLUSTRATION 13: MARKET RETURNS BY MONTH MID TERM ELECTIONS -VS- ALL OTHER YEARS

Source: The Capital Group

The chart on the left shows the historical cycle of a midterm presidential cycle bottom beginning late September, followed by a strong rally. Although the cycle appears to be normal, there are many factors that could negate the future of the cycle.

Similarly, the third year of a President’s first term also shows the greatest bounce off of the low. By contrast, the President’s second term third year has historically produced a milder bounce lacking continuation into the fourth year as show in the graph below. Keep in mind that the underlying factors that create these cycles may not always present themselves in ensuing election years.

ILLUSTRATION 14: 3RD YEAR PRESIDENTIAL CYCLE 1ST TERM -VS- 2ND TERM PRESIDENT

Source: McClellan Financial Publications

Hang in there my friends. The market may not be completely done retreating yet but there appears to be good reasons for optimism for the patient investor. And always remember, risk management is often the path less taken but the steady course leading towards successful long-term financial outcomes.

Grace and peace my friends — Buff

DISCLOSURES

Kingsview Wealth Management (“KWM”) is an investment adviser registered with the Securities and Exchange Commission (“SEC”). Registration does not constitute an endorsement of the firm by the SEC nor does it indicate that KWM has attained a particular level of skill or ability. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Kingsview Investment Management (“KIM”) is the internal portfolio management group of KWM. KIM asset management services are offered to KWM clients through KWM IARs. KIM asset management services are also offered to non KWM clients and unaffiliated advisors through model leases, solicitor agreements and model trading agreements. KWM clients utilizing asset management services provided by KIM will incur charges in addition to the KWM advisory fee. Historical references do not assume that any prior market behavior will be duplicated. Past performance does not indicate future results. This material has been prepared by Kingsview Wealth Management, LLC. It is not, and should not, be regarded as investment advice or as a recommendation regarding any particular security or course of action. Opinions expressed herein are current opinions as of the date appearing in this material only. All investments entail risks. There is no guarantee that investment strategies will achieve the desired results under all market conditions and each investor should evaluate their ability to invest for the long term. This information does not address individual situations and should not be construed or viewed as any typed of individual or group recommendation. Be sure to first consult with a qualified financial adviser, tax professional, and/or legal counsel before implementing any securities, investments, or investment strategies discussed.

© Kingsview

Read more commentaries by Kingsview