Growth World-Wide: Three International Markets Where Wasatch is Finding Opportunities

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsGiven the breadth and diversity of international equity markets, there aren’t many universal rules of thumb one can apply to investing world-wide. Except for this: Cast a wide net and cast it often.

Depending on how one defines the investment universe, international equity markets encompass five continents, 46 countries, 27 languages, and a multitude of business norms and corporate cultures. International economies are also dynamic, which means the investment landscape within a country can shift dramatically over time.

At Wasatch Global Investors, we strive to leave no stone unturned in finding the best companies within this vast, ever-changing universe. Each year, in international developed markets, we screen every small-cap company to assess its quality and growth potential. We also spend roughly three months a year traveling to different countries to meet with management teams and get a feel for how businesses are operating on the ground.

This adaptive investment process can lead us to identify some of the best opportunities in countries that are worlds apart culturally, geographically and operationally. That’s the situation we find today. In the current landscape, we believe many attractive investments lie outside of continental Europe, a region many investors think of first when it comes to international investing. Instead, we’re currently finding the most compelling opportunities within three countries—Canada, the United Kingdom and Japan. This investment brief explores the changes and catalysts taking place within each of these countries that are leading us to find more company-specific opportunities.

Canada—A Small Country Punching Above Its Weight

One of the biggest changes to the Wasatch International Small Cap Growth strategy (representative account) in recent quarters is an increased weight in Canadian companies. In many client portfolios, that weight is now as large as our position in all of continental Europe. As bottom-up, fundamental investors, the increase is not based on a macroeconomic call. We’re simply finding more Canadian small-cap companies that are attractively valued and meet our stringent criteria for high-quality growth businesses.

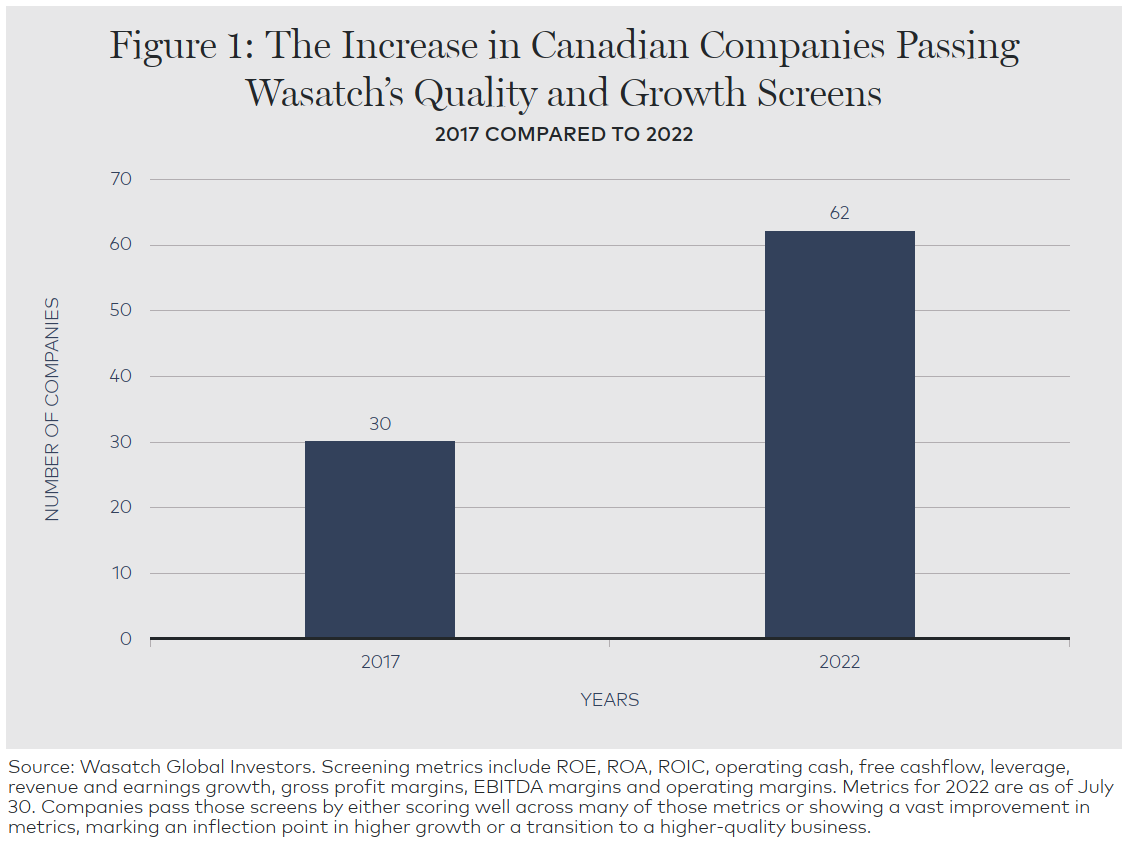

Figure 1 below puts the expanding opportunity set in perspective. We annually screen all the companies in Canada and other international markets on several metrics, including return on equity (ROE), return on assets (ROA), return on invested capital (ROIC), and revenue and earnings growth. The screens serve as an early filtering process to help us identify high-quality growth companies. Historically, there weren’t many Canadian firms that successfully met our initial investment criteria. But, as Figure 1 shows, the number of companies screening positively has doubled over the last five years.

Figure 1

We believe there are three reasons the opportunity set within Canada is expanding:

- First, Canada is at an optimal size and wealth status to nurture global businesses.

- Second, the country is developing vibrant information-technology (IT) and health-care sectors.

- Third, we believe the quality of management teams in Canada is improving.

Canada—An Estuary for Global Businesses of the Future

Canada’s business environment can be likened to an estuary—a partially enclosed coastal body of water where freshwater from streams mixes with salt water from the ocean. Estuarine habitats are often called the “nurseries of the sea” because their nutrient-rich waters provide an optimal feeding ground for young marine species to grow strong before heading to the vast ocean. At the same time, the estuary lacks many of the predators lurking in the ocean’s open waters.

Canada’s market and economy is not that different. Canada, as a nation of only 38 million people, is smaller population-wise than the state of California. This makes it a lower priority for global companies to enter the market and compete against Canada’s businesses. Yet there’s enough domestic wealth and demand to provide small domestic companies with ample headroom for growth. This makes Canada the ideal “estuary” in which a company can fine-tune its strategy and work through growing pains before branching out and replicating its success globally.

Further, capital tends to be scarcer in smaller countries. This forces management teams to be disciplined capital allocators, which lays the groundwork for companies to have a stronger balance sheet and ultimately a higher-quality business in the future.

As long-time international investors, we’ve seen this “estuary effect” play out in other small but wealthy countries. Over the years, for example, our International Small Cap Growth strategy (representative account) held many Australian and Swedish small-cap companies that grew into strong global franchises. We expect that many of our Canadian holdings will do the same.

Beyond Energy—Canada’s Burgeoning Technology and Health-Care Sectors

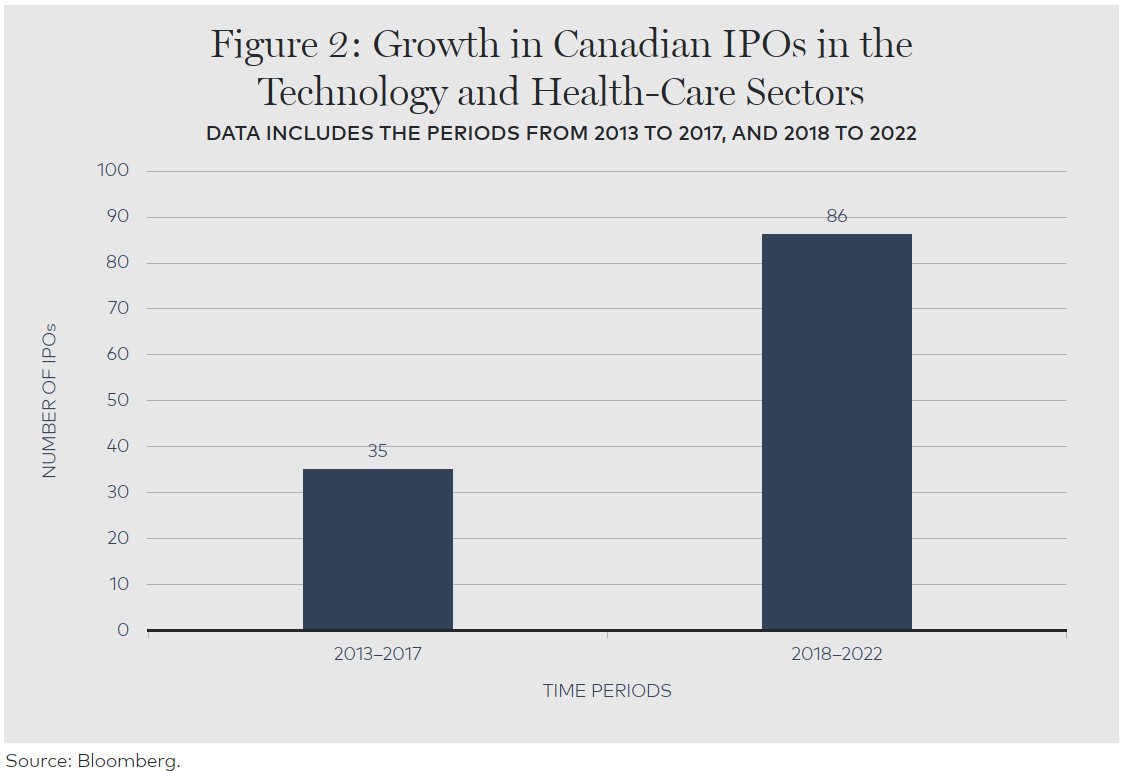

While energy and material production are still vital to the Canadian economy, other industries are growing. Notably, the IT and health-care sectors are blossoming. More capital is flowing into these areas, which has led to the formation of more of the high-quality, high-growth businesses that Wasatch typically favors. This can be seen through the growth of the initial public offering (IPO) market. (See Figure 2 below.) In the past five years, the number of IT and health-care companies that went public more than doubled the number from the prior five years.

Figure 2

Growth within the IT and health-care sectors is due in part to an influx of talent. Management teams report that younger professionals are more sensitive to and aware of climate change. Until the recent spike in oil prices, Canada’s energy sector had been in decline. As a result, management teams tell us that much of the talent that might previously have sought jobs within Canada’s energy sector are instead choosing to work within technology and health-care fields they find more stimulating and dynamic.

Management Quality Is Improving

The third reason we’re finding more attractive growth companies in Canada is that we believe the quality of management teams is improving. While this is purely a qualitative assessment, in recent visits to Canada we’ve discovered a growing number of savvy, world-class management teams that have impressed us. We believe the change is due in part to Canadians leaving U.S. companies or universities and desiring to work back home.

In summary, Canada’s favorable dynamics that nurture global businesses, the rise of its knowledge-based sectors and an improvement in management quality work together to make Canada a fertile hunting ground for finding attractive growth companies.

The U.K.—Macro Clouds Obscure Positive Company Fundamentals

For select U.K. companies, the past six years can be summed up by a familiar adage: “When the going gets tough, the tough get going.”

Since 2016, U.K. management teams have had to navigate a series of obstacles. First, Brexit disrupted trade relations with Europe and cast a host of uncertainties over businesses. Next, the Covid-19 pandemic hit the U.K. especially hard, and the government’s response was arguably lackluster compared to most other developed nations. More recently, political uncertainty hangs over the region after U.K. Prime Minister Boris Johnson announced his resignation amid scandal.

U.K. stock valuations, which are the lowest since 2009 by some metrics, reflect these negative factors. What the valuations don’t reflect is that many firms have forged ahead and grown despite the challenges.

In response to Brexit, many management teams found ways to run leaner, more efficient operations. Other companies made acquisitions to gain scale and improve profit margins or invested during a period of economic uncertainty—allowing them to take market share from competitors. Such responses have created competitive, highly profitable businesses that are thriving despite the political and macroeconomic headwinds buffeting the U.K.

Earnings Growth Demonstrates Companies’ Resiliency

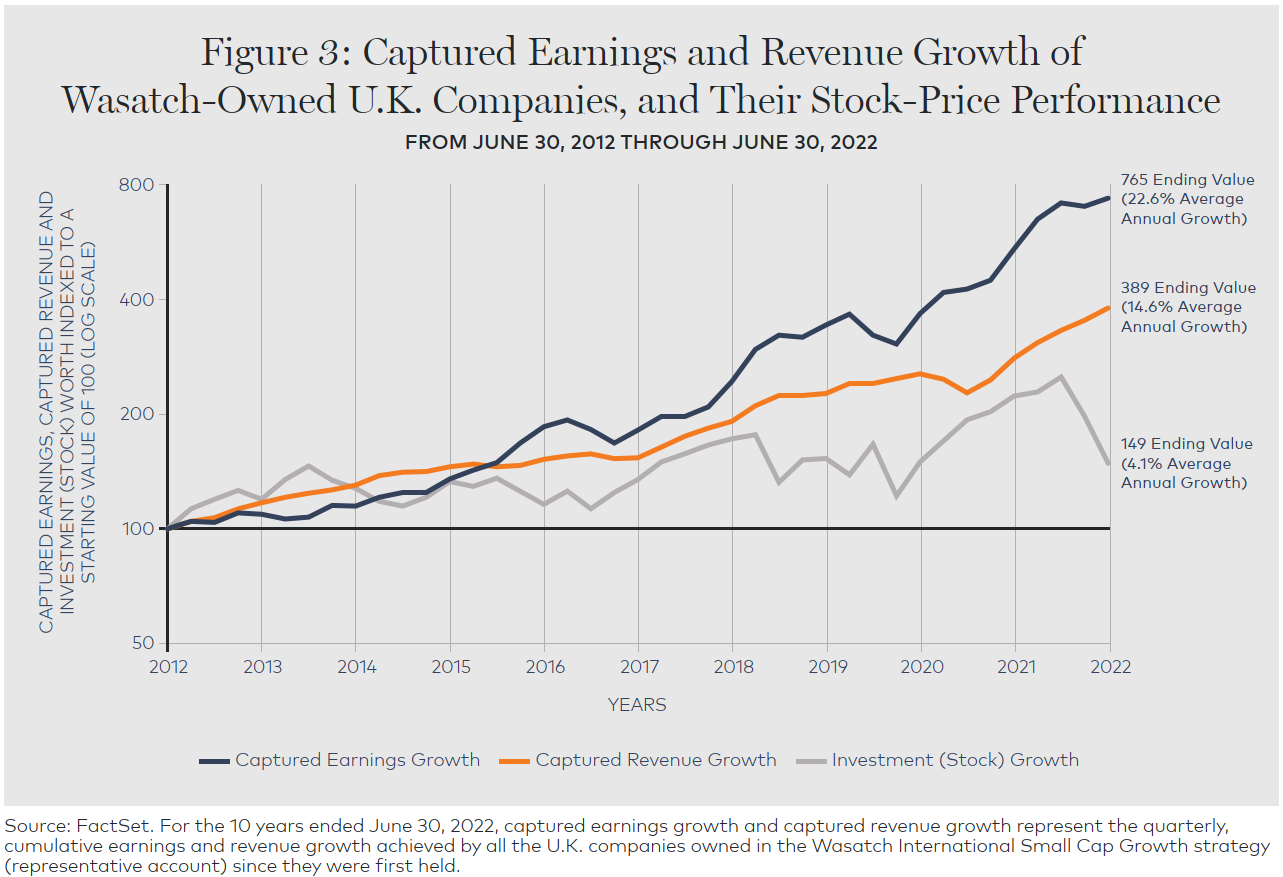

Figure 3 below offers one way to look at the dichotomy between U.K. stock performance and companies’ resiliency. In the graph, the blue line shows the “captured earnings growth” of Wasatch’s U.K. holdings over time, while the orange line shows “captured revenue growth.” We define this as the earnings growth and revenue growth a company achieves, or “captures,” after the Wasatch International Small Cap Growth strategy (representative account) invested in the stock. The gray line, meanwhile, shows the investment (stock) growth of those same holdings for the 10 years ended June 30, 2022.

Figure 3

The upward trajectory of the blue and orange lines shows relatively steady earnings and revenue growth since Brexit in 2016. We believe the fact that earnings have grown more than revenue speaks to the ability of our U.K. companies to tighten their belts, run leaner operations and generate more earnings from their revenue. We believe stock prices have lagged due to the string of political and macro issues clouding the U.K.

Over longer periods, we expect a company’s stock performance to closely track its earnings growth. With even a whiff of economic and political normalcy, we would anticipate that trend to resume within the U.K. market. In our view, today’s low valuations leave our U.K. holdings spring-loaded for better performance when these companies get credit for the earnings growth they’ve continually produced.

Japan—A Late Emergence from Covid-19 Restrictions

The markets in Japan and the U.K. share a similarity. In both countries, macro events have obscured positive, fundamental changes at the corporate level. But unlike the U.K., which has experienced a string of negative events, the single, predominant negative issue hanging over Japanese equities has been the Covid-19 pandemic.

The Japanese government’s initial response to Covid was more restrictive than that of many countries. The government also took a more cautious approach to vaccine distribution, waiting until March of 2021 to start vaccinating individuals. For comparison, by the end of June 2021, the U.S. had vaccinated 47% of its population, while Japan had vaccinated only 10%. The slow vaccine rollout delayed a return to normal activity in Japan. Then, when a new wave of the virus hit in late 2021 and early 2022, Japan again took a conservative approach to managing it, shutting down activity more than most other developed countries.

With its economy slow to emerge from Covid-related curbs on activity, Japanese equities have continued to underperform broader global equity indexes. As we see it, the underperformance belies important structural improvements taking place within Japanese businesses.

Structural Changes Have Been a Decade in the Making

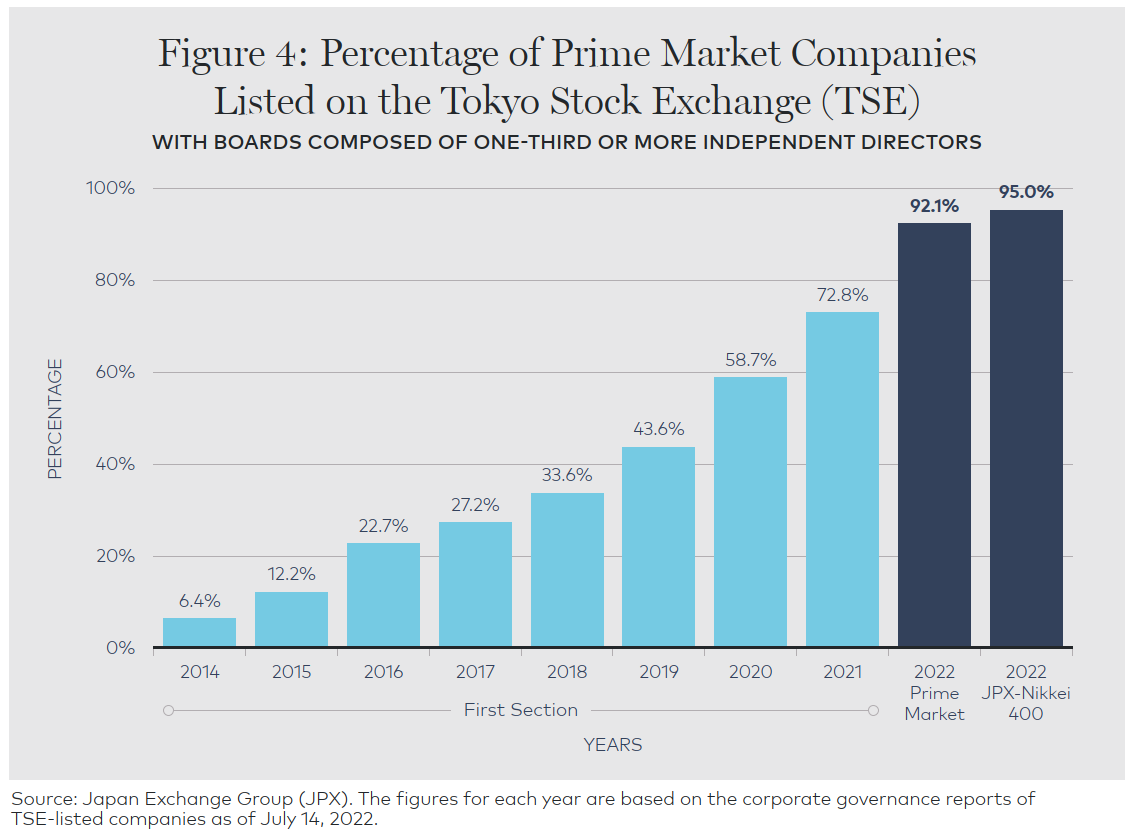

The groundwork for structural improvement was laid nearly a decade ago, when Shinzo Abe was elected prime minister. To revive the economy, he introduced an economic framework based on “three arrows”—economic policy, fiscal stimulus and structural reforms. The third arrow—structural reforms—included goals such as improving corporate governance, encouraging companies to have more independent directors and boosting business competitiveness.

Ten years later, we’re seeing real change. For example, in 2015 Japan’s financial regulators established a code requiring listed companies to appoint at least two independent directors to their board. In June 2021, the code was amended to require that at least one-third of board members be independent. This has led to a big change in board composition. (See Figure below.)

Figure 4

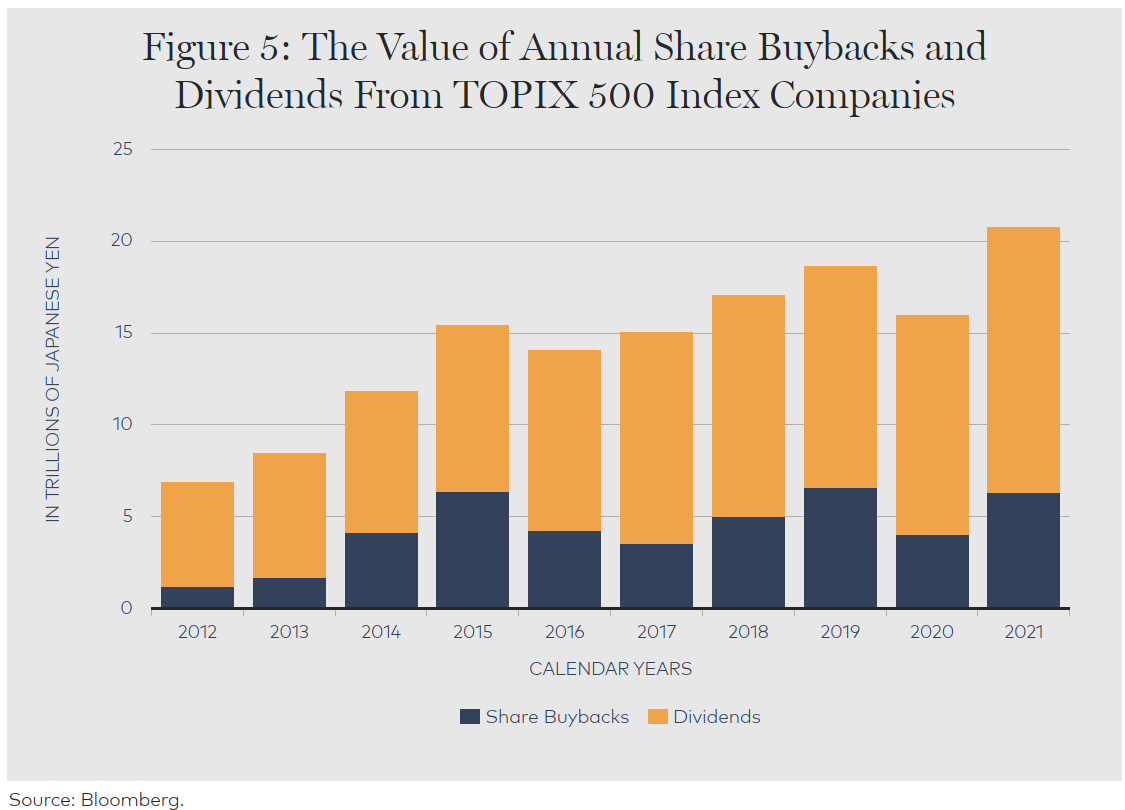

An important byproduct of the structural changes within corporate Japan is that directors and management teams have become more focused on creating value for shareholders. We see these teams putting cash to work in more productive ways, including paying dividends, buying back shares and making investments to grow their businesses.

Figure 5 below puts the magnitude of some of these actions in perspective. While management teams were understandably more cautious at the height of the pandemic in 2020, the amount of cash returned to shareholders via dividends and share buybacks has otherwise steadily increased since 2016 and has roughly tripled since 2012.

Figure 5

We’re seeing Japanese companies put cash to work in other productive ways too. For example, Japan’s pharmaceutical industry has increased research and development spending to new highs. We expect this could lead to innovative discoveries in the future.

After Covid-19

While the structural changes affecting Japanese companies are substantial, we don’t believe these positives are being reflected in stock prices, which have languished during the pandemic. However, normal activity is finally resuming in Japan. We’ve seen a pickup in restaurant activity, more positive consumer surveys and growth in a number of other indicators that show economic activity is normalizing. When the Covid-19 cloud hanging over Japan’s equity market lifts, we believe investors will start to appreciate many of the positive, fundamental changes taking place at Japanese companies.

Conclusion

At Wasatch, we rely on extensive bottom-up research to identify stocks for our strategies and funds. Our investment decisions are driven by company fundamentals, not macro factors. But larger forces can still tilt the playing field so that at times we find more company-specific opportunities within a given country.

This is what we find today in Canada, an estuary for global businesses with burgeoning IT and health-care sectors. It’s also what we find in the U.K., where Brexit and other headwinds have led to lower stock valuations but have forced companies’ management teams to run leaner operations and take other actions to improve their competitive positions. Finally, structural improvements have created a wider pool of high-quality growth companies to choose from within Japan. We expect Japanese companies to get credit for those improvements as the shadow of Covid-19 passes. Given the changes afoot, we believe these three countries present some of the best opportunities in international markets today.

RISKS AND DISCLOSURES

Investing in foreign securities, especially in frontier and emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

An investor should consider investment objectives, risks, charges and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit wasatchglobal.com or call 800.551.1700. Please read the prospectus carefully before investing.

Information in this document regarding market or economic trends, or the factors influencing historical or future performance, reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

Wasatch Advisors, Inc., trading as Wasatch Global Investors ARBN 605 031 909, is regulated by the U.S. Securities and Exchange Commission under U.S. laws which differ from Australian laws. Wasatch Global Investors is exempt from the requirement to hold an Australian financial services licence in accordance with class order 03/1100 in respect of the provision of financial services to wholesale clients in Australia.

The representative account for the Wasatch International Small Cap Growth strategy is the Wasatch International Growth Fund. The investment objective of the Wasatch International Growth Fund is long-term growth of capital.

Wasatch Advisors, Inc., doing business as Wasatch Global Investors, is the investment advisor to Wasatch Funds.

Wasatch Funds are distributed by ALPS Distributors, Inc. (ADI). ADI is not affiliated with Wasatch Global Investors.

DEFINITIONS

Brexit is an abbreviation for “British exit,” which refers to the June 23, 2016 referendum whereby British citizens voted to exit the European Union. The referendum roiled global markets, including currencies, causing the British pound to fall to its lowest level in decades.

Earnings growth is a measure of growth in a company’s net income over a specific period, often one year.

EBITDA is a company’s earnings before interest, taxes, depreciation and amortization.

An initial public offering (IPO) is a company’s first sale of stock to the public.

The JPX-Nikkei Index 400 is composed of common stocks whose main market is the Tokyo Stock Exchange Prime Market, Standard or Growth Market. The Index holds companies which meet requirements of global investment standards, such as efficient use of capital and investor-focused management perspectives. The JPX-Nikkei Index 400 was jointly developed by Nikkei, Japan Exchange Group and the Tokyo Stock Exchange.

Return on assets (ROA) measures a company’s profitability by showing how many dollars of earnings a company derives from each dollar of assets it controls.

Return on equity (ROE) measures a company’s efficiency at generating profits from shareholders’ equity.

Return on invested capital (ROIC) is a way to assess a company’s efficiency at allocating the capital under its control to profitable investments.

Sales growth is the increase in sales over a specified period of time, not necessarily one year.

The Tokyo Stock Exchange (TSE) is the largest stock exchange in Japan and lists the nation’s biggest companies. It is also one of the world’s largest stock exchanges.

The Tokyo Stock Price Index, commonly known as TOPIX, is a free float adjusted market capitalization-weighted index that is calculated based on all the domestic common stocks listed on the Tokyo Stock Exchange (TSE) First Section. It is calculated and published by the TSE.

The TOPIX 500 Index is a capitalization-weighted index designed to measure the performance of the 500 most liquid stocks with the largest market capitalization that are members of the TOPIX Index.

Valuation is the process of determining the current worth of an asset or company.

©2022 Wasatch Global Investors https://wasatchglobal.com/

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits