Federal Reserve Chair Jerome Powell’s hawkish comments dominated the markets on Friday, with the major indices all seeing a drop of over 3%. He acknowledged that higher rates “will bring some pain to households and businesses.” Powell also reinforced the Fed’s position on longer-term rates, pointing out that the current 2.25 – 2.5% range is within the Summary of Economic Projections’ longer-term range. Further comments indicated that the September meeting could see another 75 basis-point hike. Fed Funds futures data shows that the market is taking him at his word, with the probability of a 75 basis-point hike rising from 47% the prior week to 65%. Futures data has also indicated the likelihood of another 50 basis-point increase at the November meeting, with the probability of a rate over 3.5% being more likely than not.

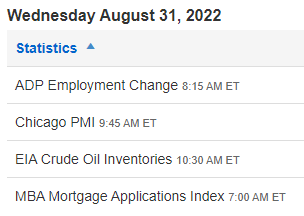

Given the Fed consensus that the current rate is the “new normal” and Powell’s hints at the board’s willingness to subject the economy to some short-term discomfort, the sell-off was a reasonable response. Monday morning saw a continuation of Friday’s moves, with the indices down another 0.7%+. As Q2 earnings season draws to a close, other data will take over as fundamental drivers of the equity markets. Today we are looking forward to the Conference Board Consumer Confidence Survey, which is forecasted to increase from 95.7 to 97.4, driven partly by a decline in energy costs, and the Job Opening and Labor Turnover Survey (JOLTS) which is forecasted to show 10.4 million job openings. It has remained over 10 million since last August, in a confirmation of the labor market tightness that Chairman Powell mentioned in his remarks at the Jackson Hole conference. Later in the week we will see more data from the Department of Labor on unemployment and non-farm payrolls.

Internationally, concerns about energy prices in Europe are drawing scrutiny, with both the UK and Eurozone both likely to see a recession as higher fuel costs are expected to eat into disposable income and thus consumer spending. Western European indices have mirrored those of the US, down 0.7%+, except for the UK which had their Summer Bank Holiday yesterday. While recession concerns can often be dampened by dovish central bank commentary and policy, inflation concerns will likely restrict their ability to provide accommodative conditions.