Tourism was one of the first sectors to be deeply squeezed by the pandemic. Lockdowns and the closure of international borders led to a near-complete cessation of activity in an industry which had grown immensely over recent decades. With the worst of the pandemic behind us, there are signs that the industry is finally seeing some recovery.

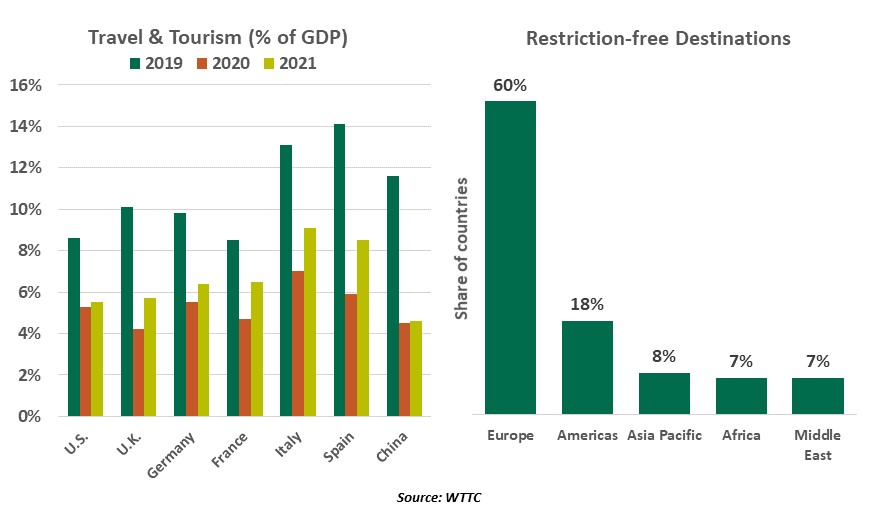

Tourism is a significant source of employment and livelihood for millions around the world, especially in Europe. As a result, COVID restrictions had an unprecedented impact on travel-related jobs and businesses. Prior to the pandemic, the travel & tourism sector accounted for one in four of all new jobs created globally. It also represented 10% of the world’s employment (333 million) and global gross domestic product (GDP). Over 20 national economies generated more than one-tenth of their national income from this sector.

In the first year of the pandemic, travel’s share of global GDP halved to 5%, even with a reduced denominator as all activity slowed. In the same year, 62 million jobs were lost in the travel & tourism sector. The global vaccine rollout was hoped to be the medicine that would set the stage for the revival of tourism in 2021, but that outcome didn’t materialize. New COVID-19 variants and public health measures continued to hinder domestic and foreign travel.

But as a growing number of destinations ease limitations on movement, international arrivals in various regions are ticking up again. Household savings accrued during the pandemic, led by generous government support and the inability of people to spend on travel and entertainment during 2020 and 2021, provided further impetus to the industry.

According to World Tourism Organization data, global tourism increased 182% in the first quarter of 2022 over the same time period last year. With two years of summer holidays lost, the momentum continued into the peak season. Global hotel occupancy in April and May exceeded pre-pandemic levels. The European and American continents are at the forefront of this recovery. Europe saw more than four times as many international arrivals in the first five months of 2022 when compared to last year’s traffic. In the Americas, arrivals more than doubled.

Spending on international tourism from countries like France, Germany, Italy and the U.S. is now at 70% to 85% of 2019 levels. The cost of travel, from airfares to hotel rates, has surged in recent months as demand soared while supply was constrained. Staff shortages at airports and across the hospitality sector are raising both prices and anxiety.

While increased traffic has induced confidence among observers about the recovery of international travel, there are also doubts that the momentum can be sustained. Households are reeling from rising costs of essentials, depleted savings and falling real incomes. Surging energy costs and the price of fuel have pushed airfares to record levels. If sustained, this will force consumers to cut back on leisure activities.

|

Tourism is back, but not all the way back.

|

And the recovery is far from complete. Tourist arrivals are still 54% below 2019 levels, with the sector’s contribution to GDP expected to climb back to its pre-pandemic level only in 2023. Restriction-free international travel remains a distant dream. Currently, only 72 countries have lifted all COVID-related travel restrictions.

China’s zero-tolerance approach to COVID will hold the key to global travel’s full recovery. Prior to the pandemic, the country was the world’s largest outbound tourism market. Chinese tourists spent over $250 billion on overseas travel in 2019, almost one-fifth of the global total. Today, China continues to restrict international departures and arrivals.

The tourism industry has recouped some of its losses, but its recovery is still vulnerable to new variants of COVID-19, threats of geopolitical tensions and a challenging global economic environment. Just as travel is taking off, it could get grounded once again.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

© Northern Trust

Read more commentaries by Northern Trust