As we’ve hit the halftime mark for the investment year 2022, we are faced with a daunting two-headed monster. One head is the first full year of unwinding what Charlie Munger called, “the biggest financial euphoria episode in his career, because of the totality of it.” The second head is what we call “wolverine inflation,” which is mean and leaves a stench. This combination is powerful and, in many ways, unprecedented. How do we navigate a stock market which is dealing with a two-headed monster?

John Kenneth Galbraith, in his book, A Short History of Financial Euphoria, explained today’s circumstances quite well:

“That the free enterprise economy is given to recurrent episodes of speculation will be agreed. These---great events and small, involving bank notes, securities, real estate, art and other assets and objects---are, over the years and centuries, part of history.”

Munger, who has seen 75 years of these episodes, is looking at the last five years realizing that what happened to tech stock valuations became a financial euphoria episode. As a result of five consecutive years of record performance among the largest of the large-cap stocks, a mania developed among research analysts, portfolio managers and individual investors, believing that these FAANG stocks were a ticket to countless wealth. Investors, both institutional and individual, were trained like Pavlov’s dog in a “just buy the dips” mentality.

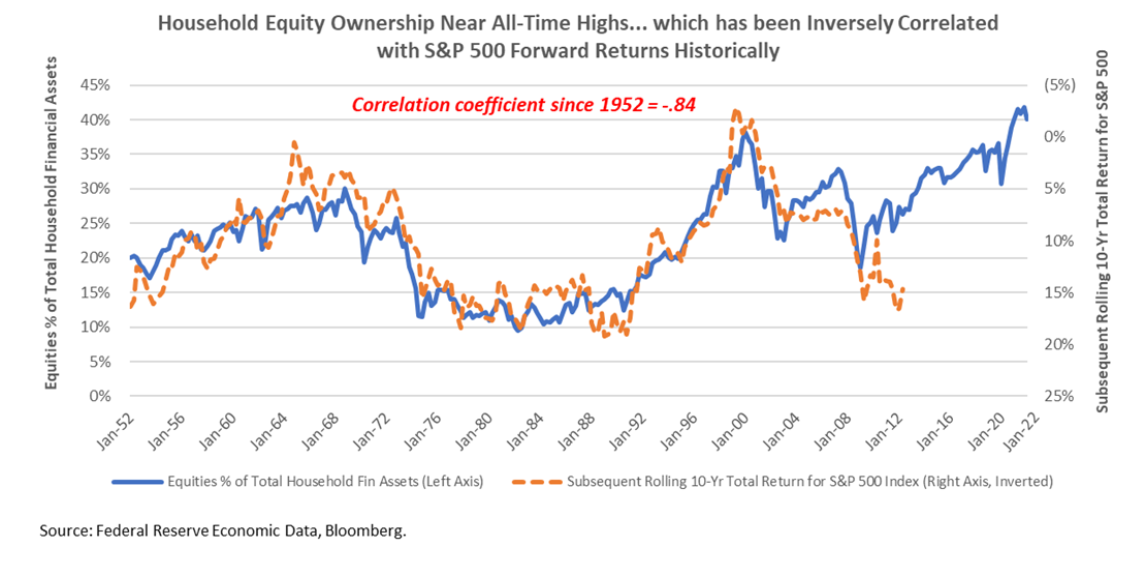

What has happened to second and third-tier tech stocks is a financial euphoria episode in and of itself. Munger recognizes that crypto became its own episode, as did clean energy investing, meme stocks, Robinhood trades, and IPOs and SPACs. This euphoria has manifested in participation/ownership of common stocks by households at levels only seen at the most major stock market tops of the last 100 years:

Simultaneously, the circumstances which could cause the Federal Reserve Board to lose control of inflation surfaced over a year ago. The Fed so hoped that the problem of inflation would go away that they dubbed it “transitory.” This explosion of price increases followed the pandemic just as the economic textbooks of my college years would have prescribed: Too many people with too much money chasing too few goods.

To deal with the pandemic war (COVID), the U.S. Government borrowed $6-7 trillion dollars and printed money. In tandem with this massive liquidity, 90 million millennial Americans started to form households and join adulthood for the first time. Then, as if we needed another inflation driver, our under-investment in energy was made glaringly obvious when Russia invaded Ukraine and caused the price of oil and gas to soar.

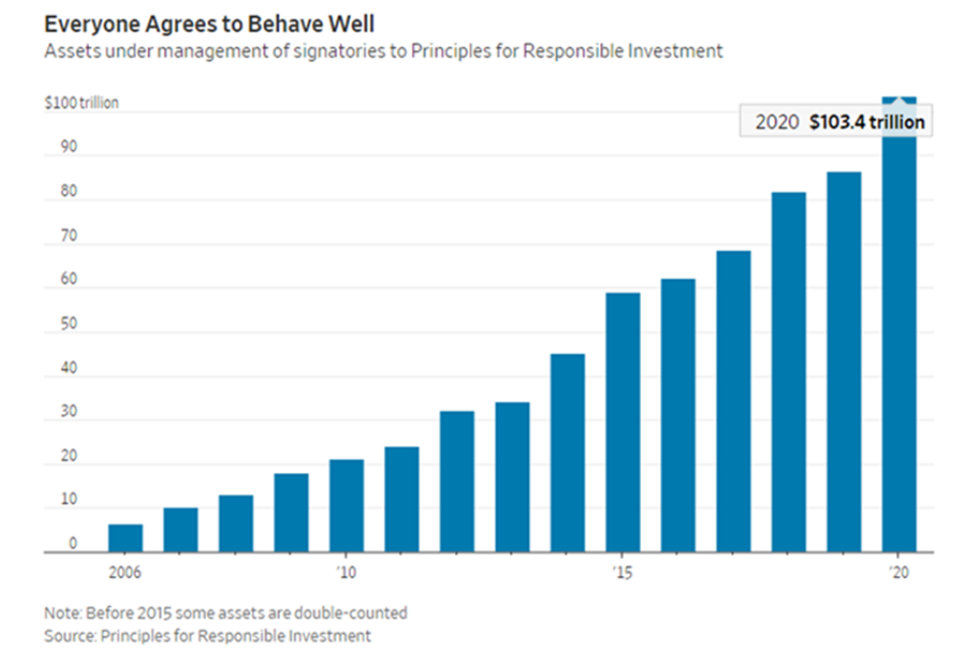

While ESG investing has soared in popularity:

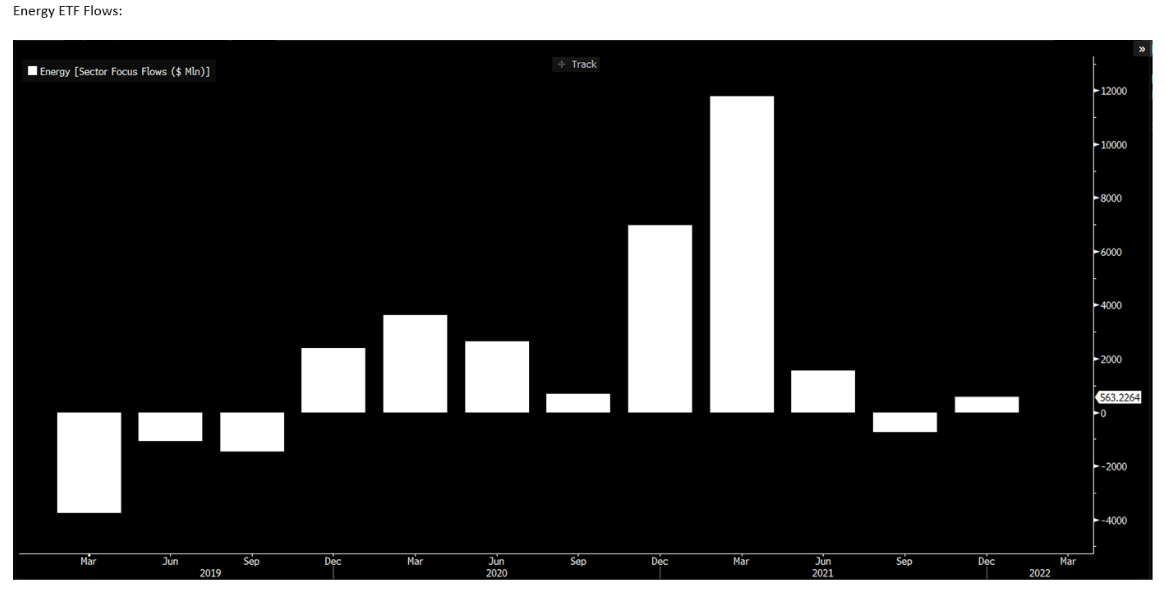

Investments in oil and gas disappeared:

Therefore, inflation has reached 8.6%, and the on-the-ground inflation rate in many cities is most likely even higher. In an effort to make up for their error of one year ago, the Fed is now raising the federal funds rate aggressively and pulling its buying of bonds in the open market. Unfortunately, the proverbial cat has been let out of the bag and this wolverine inflation animal is especially hard to get back into its high-elevation cave.

Action plan for the Two-Headed Monster

“Anyone taken as an individual is tolerably sensible and reasonable—as a member of a crowd, he at once becomes a blockhead.”

—Friedrich Von Schiller, As quoted by Bernard Baruch

Our plan for dealing with the unwinding of the financial euphoria episode is the same as the plan we had before it began to unwind. You avoid the areas which were part of the euphoria and don’t try to be a hero:

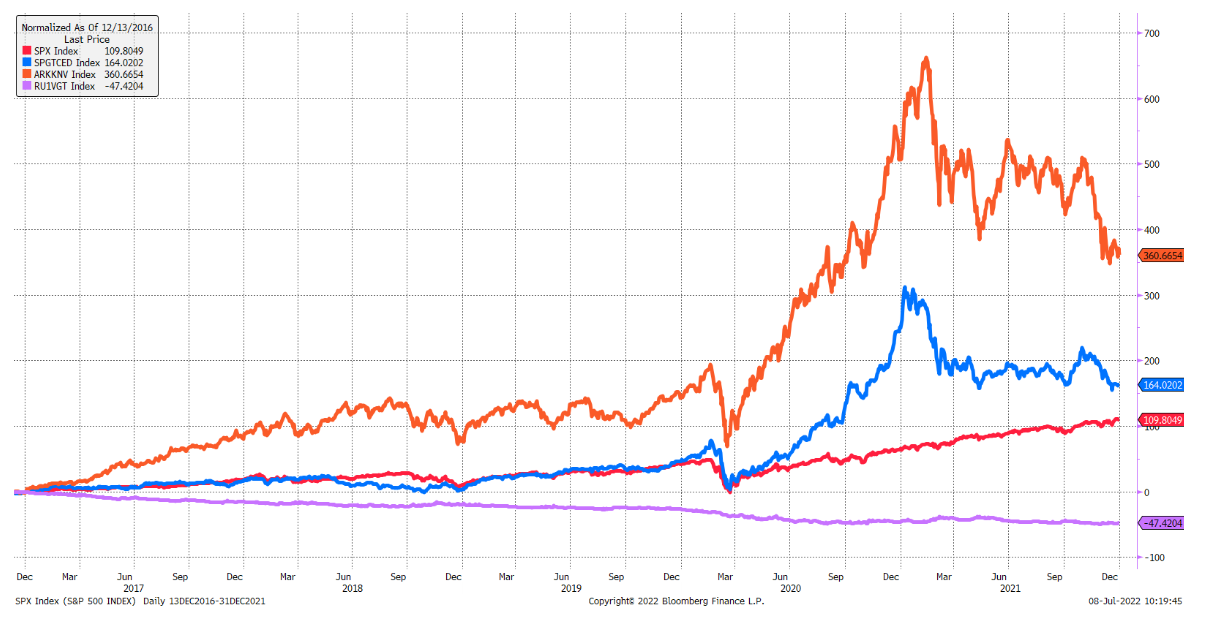

The five-year chart below compares the returns of the S&P 500 Index, the S&P Global Clean Energy Index, the ARK Innovation ETF NAV Index and the Russell 1000 Value/Growth Total Return Index:

We believe you need to avoid these formerly glamorous stock groups for many years. We loved to use eBay (EBAY) as a poster child back in 1999 for the dotcom bubble. We bought it eight years later and have done very well on it. We wouldn’t have done well if we bought it in the early years of that bear market, or even five years later. If you think this bear will be shorter and or less damaging than the dotcom bear market of 2000-2003, you could be showing your inexperience!

Where do we believe we can make money in the next two years?

We are very excited about the zeitgeist which will develop as wolverine inflation emerges as a more permanent problem. Investors will chase companies that benefit from 90 million millennials replacing 65 million Gen-X Americans in the key 27–45-year-old age group. The 1970s were all about household formation among baby boomers and the liquidity created by the Federal Government to fight the Vietnam War and to fight poverty, with President Johnson’s Great Society legislation in 1968.

Household formation among millennials should drive a big increase in necessity spending, at the expense of discretionary spending. The stocks which did well from 2010-2019 were all about single people spending money on non-necessity personal pleasures. Necessity spending among the 27–45-year-old group could encourage investment success in oil and gas, real estate and residential housing.

The biggest problem investors have is their willingness to invest in former darlings being crushed by the first six months of this bear market. This bear market won’t die until there is a capitulation in the money flows into darling tech stocks, crypto and other speculative investments covered by Friedrich Von Schiller.

As we wrestle with the “Two-Headed Investment Monster” and position ourselves to benefit from “Wolverine Inflation,” we ask for your patience, thank you for your confidence in our discipline and always suggest that investors fear stock market failure!

© Smead Capital Management

Read more commentaries by Smead Capital Management

We are very excited about the zeitgeist which will develop as wolverine inflation emerges as a more permanent problem. Investors will chase companies that benefit from 90 million millennials replacing 65 million Gen-X Americans in the key 27–45-year-old age group. The 1970s were all about household formation among baby boomers and the liquidity created by the Federal Government to fight the Vietnam War and to fight poverty, with President Johnson’s Great Society legislation in 1968.

We are very excited about the zeitgeist which will develop as wolverine inflation emerges as a more permanent problem. Investors will chase companies that benefit from 90 million millennials replacing 65 million Gen-X Americans in the key 27–45-year-old age group. The 1970s were all about household formation among baby boomers and the liquidity created by the Federal Government to fight the Vietnam War and to fight poverty, with President Johnson’s Great Society legislation in 1968.