Goods versus Services

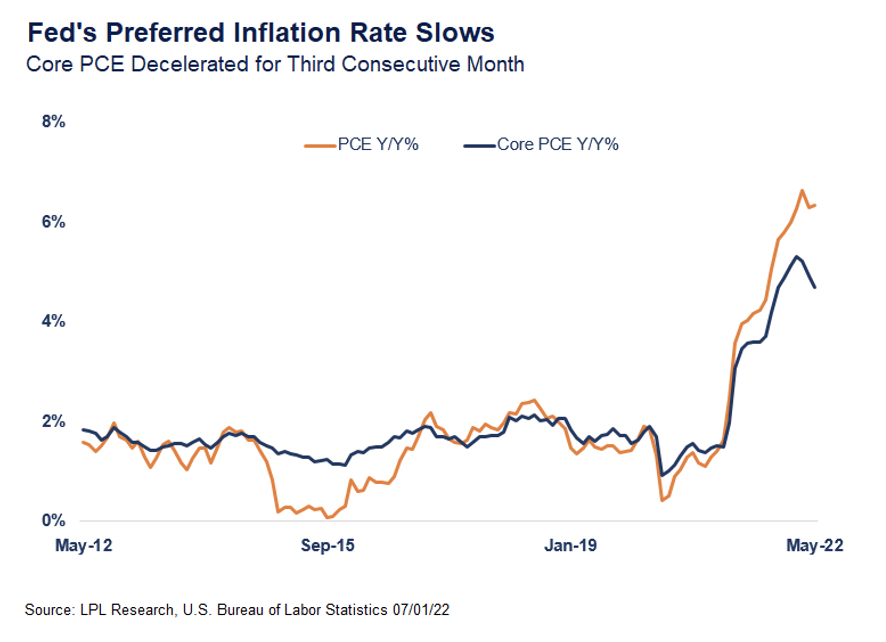

Before we think about the hypothetical new world order that global inflation may enter, let’s start with the good news within the United States. The Federal Reserve’s (Fed) preferred measure of inflation, the core PCE deflator, is slowing on a year-over-year basis. As shown in the LPL Chart of the Day, the May core PCE deflator rose 4.7% from a year ago. The annual growth rate slowed for the third consecutive month after reaching a high of 5.3% year-over-year in February. “Inflation is still stubbornly high and far above the Fed’s long run target of 2% but the deceleration in the core rate is encouraging,” explained Jeffrey Roach, Chief Economist at LPL Financial.

Price conditions in the U.S. are best understood by breaking out goods inflation from services inflation and the rate of inflation seems to be cooling for durable goods.

Auto prices continue to moderate as growth rates for motor vehicles and parts slowed for the fourth consecutive month. Used auto prices rose at the slowest pace since May 2020 and as supply bottlenecks improve, the car market should begin to revert to pre-COVID behavior.

Recreational goods and vehicle prices were flat from a year ago, as high gas prices are slowing demand for recreational vehicles.

However, a major concern for the Fed is the surge in travel-related demand is pushing services inflation up. Consumer prices for housing, restaurant, and accommodation services are reaching new highs as consumers release pent up demand for travel and housing costs react to the recent hot real estate market.

Overall, this is a positive report for investors as the core year-over-year growth rate has consistently fallen since February. This inflation report gives some salve to policy makers after what seemed to be unanchored inflation expectations in the previous week’s consumer confidence report. According to the Conference Board, inflation expectations 12 months hence rose to 8%, a record high but conflicting with the University of Michigan report as well as the inflation rate implied by Treasury Inflation-Protected Securities (TIPS).

Could Global Economies be Entering a Higher Long-run Inflation Regime?

With all the talk on inflation rates decelerating, in actuality, inflation may not reach the preferred target in the near term.

Consumers may have to live in a new world where inflation consistently runs hotter than the previous decade. At least, that’s what global central bankers warned at the ECB conference in Portugal.

Reshoring production, newer health protocols, and tight labor markets could keep inflation rates above the 2% long run average for the near term.

Policy makers must come to grips with a real possibility that inflation rates will not come down to their preferred targets any time soon. The latest inflation report is a juggernaut for the Federal Reserve as they use blunt instruments to slow aggregate demand during a time when inflation is also irritated by supply shocks. For more on the current environment, be sure to watch our latest Econ Market Minute, where Chief Economist Jeffrey Roach gives more economic insights. https://www.youtube.com/watch?v=7TxNgAps0Vo

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. For more information on the risks associated with the strategies and product types discussed please visit https://lplresearch.com/Risks

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

Securities and advisory services offered through LPL Financial, a registered investment advisor and broker-dealer. Member FINRA/SIPC.

LPL Financial Research discusses the latest PCE inflation report and the risks that inflation may not come down to the Fed’s preferred target for many years.

Read more commentaries by LPL Financial